|

Related Topics

|

|

Category: Stock Market and American Express (AXP)

Date: 26 October 2020 Stock Price of American Express: $100.98 We take a look at the 3rd quarter earnings report of their 2020 fiscal year of American Express, a leading global payments company that provides personal and business credit and travel cards. The group reported that they are making provisions to write off $879 million in credit losses for the quarter. They reported revenues of $8.06 billion and net income of $1.073 billion.

|

|

- Since the lows of mid-April, we have seen a steady recovery in our overall spending volumes. In fact, we had positive year-over-year growth in non-T&E spending, which has long accounted for the large majority of our overall volumes. While credit remains strong, with delinquencies and net write-offs at the lowest levels we have seen in a few years, we remain cautious about the direction of the pandemic and its impacts on the economy, which is reflected in our reserve levels. - Stephen J. Squeri, Chairman and Chief Executive Officer"

About American Express

American Express is a globally integrated payments company, providing customers with access to products, insights and experiences that enrich lives and build business success.

Overview of American Express' 3rd quarter 2020 earnings report

Data below refers to the latest quarters data unless specified otherwise:

- Total revenues: $8.086 billion (down from $10.110 billion for the same period of the previous year)

- Revenues decreased by -20% over the last 12 months

- Expenses: $6.722 billion (down from $7.844 billion for the same period of the previous year)

- Expenses decreased by -14% over the last 12 months

- Net earnings: $1.073 billion (down from $1.755 billion for the same period of the previous year)

- Diluted earnings per share: $1.30 (down from $2.08 for the same period of the previous year)

- PE ratio of American Express: 35.7

- Dividend declared: $0.43 (up from $0.39 for the same period of the previous year)

- Dividend yield: 1.7%

- Diluted weighted-average shares outstanding: 805 million (down from 827 million for the same period of the previous year)

- Cash and cash equivalents: $33 billion

- Cash and cash equivalents per share: $40.99

- Cash and cash equivalents makes up 40.5% of American Express' market capital

- Cash and cash equivalents makes up 17.6% of American Express' total assets

- Card member loans: $64 billion

- Card member loans makes up 34.2% of American Express' total assets

- Stockholders equity in American Express: $22 billion

- Stockholders equity per share: $27.32

- So American Express is trading a 3.69 times its stockholders equity which is outside the expected range of between 2 and 4 which most firms ten to trade at.

American Express' management commentary on their 3rd quarter 2020 earnings report

NEW YORK--(BUSINESS WIRE)-- American Express Company (NYSE: AXP) today reported third-quarter net income of $1.1 billion, or $1.30 per share, compared with net income of $1.8 billion, or $2.08 per share, a year ago.

“While our business continues to be significantly affected by the impacts of the pandemic, our third quarter results have increased our confidence that our strategy for managing through the current environment is the right one,” said Stephen J. Squeri, Chairman and Chief Executive Officer.

“Since the lows of mid-April, we have seen a steady recovery in our overall spending volumes. In fact, we had positive year-over-year growth in non-T&E spending, which has long accounted for the large majority of our overall volumes. While credit remains strong, with delinquencies and net write-offs at the lowest levels we have seen in a few years, we remain cautious about the direction of the pandemic and its impacts on the economy, which is reflected in our reserve levels.

“The investments we have made to enhance our value propositions have yielded strong results, driving spending and loyalty, and our voluntary attrition rates on our proprietary products remain lower than last year. We’re also expanding our largest ever Shop Small campaign to support small merchants in 18 countries and territories. In addition, we have begun to selectively increase our customer acquisition activities while continuing to invest for the long term, such as expanding our commercial offerings through our recent acquisition of financial technology company Kabbage, as well as officially launching our network in mainland China. Additionally, we have maintained a robust liquidity position and capital ratios well above targets. “We recognize that the road ahead continues to be uncertain, but we are confident that the steps we are taking will enable us to exit this crisis in a strong position and maximize value for our stakeholders over the long term.”

“While our business continues to be significantly affected by the impacts of the pandemic, our third quarter results have increased our confidence that our strategy for managing through the current environment is the right one,” said Stephen J. Squeri, Chairman and Chief Executive Officer.

“Since the lows of mid-April, we have seen a steady recovery in our overall spending volumes. In fact, we had positive year-over-year growth in non-T&E spending, which has long accounted for the large majority of our overall volumes. While credit remains strong, with delinquencies and net write-offs at the lowest levels we have seen in a few years, we remain cautious about the direction of the pandemic and its impacts on the economy, which is reflected in our reserve levels.

“The investments we have made to enhance our value propositions have yielded strong results, driving spending and loyalty, and our voluntary attrition rates on our proprietary products remain lower than last year. We’re also expanding our largest ever Shop Small campaign to support small merchants in 18 countries and territories. In addition, we have begun to selectively increase our customer acquisition activities while continuing to invest for the long term, such as expanding our commercial offerings through our recent acquisition of financial technology company Kabbage, as well as officially launching our network in mainland China. Additionally, we have maintained a robust liquidity position and capital ratios well above targets. “We recognize that the road ahead continues to be uncertain, but we are confident that the steps we are taking will enable us to exit this crisis in a strong position and maximize value for our stakeholders over the long term.”

Global Consumer Services Group reported third-quarter net income of $855 million, compared with $991 million a year ago. Total revenues net of interest expense were $5.2 billion, down 16 percent from $6.2 billion a year ago. The decrease primarily reflected declines in Card Member spending and loan volumes compared to the prior year.

Provisions for credit losses totaled $412 million, down 37 percent from $653 million a year ago. The decrease primarily reflected a modest reserve release and lower net write-offs.

Total expenses were $3.7 billion, down 14 percent from $4.3 billion a year ago. The decrease primarily reflected significantly lower customer engagement costs due to a decline in Card Member spending and lower usage of travel-related Card Member benefits, partially offset by investments in the previously mentioned value proposition enhancements and expenses related to the Shop Small campaign.

Global Commercial Services reported third-quarter net income of $220 million, compared with net income of $568 million a year ago. Total revenues net of interest expense were $2.5 billion, down 23 percent from $3.3 billion a year ago, primarily reflecting a decline in Card Member spending.

Provisions for credit losses totaled $250 million, up 13 percent from $222 million a year ago, driven by a slight reserve build.

Total expenses were $2.0 billion, down 14 percent from $2.4 billion a year ago. The decrease primarily reflected lower client incentives and other customer engagement costs due to a decline in Card Member spending.

Global Merchant and Network Services reported third-quarter net income of $263 million, compared with $523 million a year ago. Total revenues net of interest expense were $1.1 billion, down 27 percent from $1.6 billion a year ago. The decrease primarily reflected declines in Card Member spending and the average discount rate compared to the prior year.

Total expenses were $780 million, down 8 percent from $845 million a year ago, driven by lower network partner payments due to a decline in Card Member spending.

Corporate and Other reported a third-quarter net loss of ($265) million, compared with a net loss of ($327) million a year ago.

Provisions for credit losses totaled $412 million, down 37 percent from $653 million a year ago. The decrease primarily reflected a modest reserve release and lower net write-offs.

Total expenses were $3.7 billion, down 14 percent from $4.3 billion a year ago. The decrease primarily reflected significantly lower customer engagement costs due to a decline in Card Member spending and lower usage of travel-related Card Member benefits, partially offset by investments in the previously mentioned value proposition enhancements and expenses related to the Shop Small campaign.

Global Commercial Services reported third-quarter net income of $220 million, compared with net income of $568 million a year ago. Total revenues net of interest expense were $2.5 billion, down 23 percent from $3.3 billion a year ago, primarily reflecting a decline in Card Member spending.

Provisions for credit losses totaled $250 million, up 13 percent from $222 million a year ago, driven by a slight reserve build.

Total expenses were $2.0 billion, down 14 percent from $2.4 billion a year ago. The decrease primarily reflected lower client incentives and other customer engagement costs due to a decline in Card Member spending.

Global Merchant and Network Services reported third-quarter net income of $263 million, compared with $523 million a year ago. Total revenues net of interest expense were $1.1 billion, down 27 percent from $1.6 billion a year ago. The decrease primarily reflected declines in Card Member spending and the average discount rate compared to the prior year.

Total expenses were $780 million, down 8 percent from $845 million a year ago, driven by lower network partner payments due to a decline in Card Member spending.

Corporate and Other reported a third-quarter net loss of ($265) million, compared with a net loss of ($327) million a year ago.

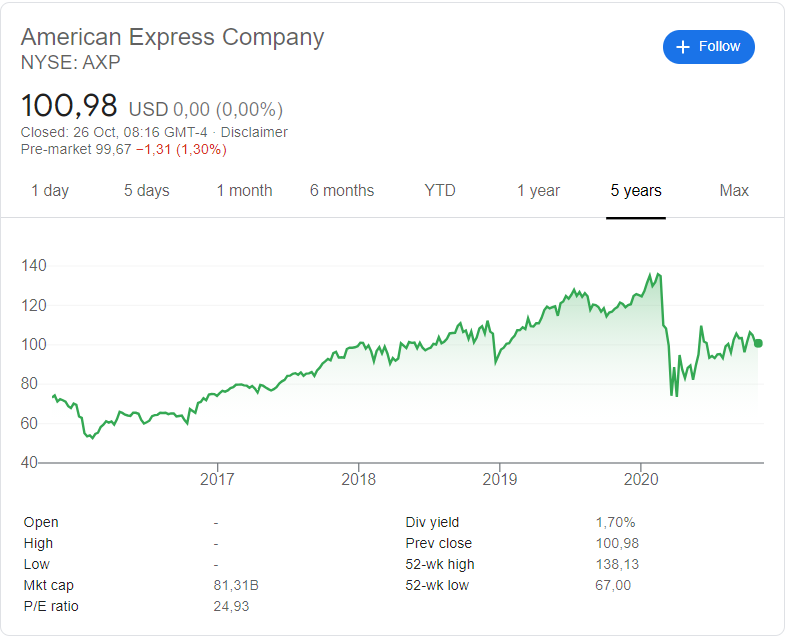

American Express (NYSE: AXP) stock price history

The image below, obtained from Google, shows the stock price history of American Express over the last 5 years. And it's been a pretty good time for American Express stockholders. 5 years ago the stock was trading at around $77.70 a stock and its currently trading at $83.17 a stock. That's a decent return of 7% provided to American Express stockholders over the last 5 years.

The stock of American Express is trading at close to the midpoint between its 52 week low and its 52 week high which to us is a clear indication that the short term sentiment and momentum of American Express is neutral at this point in time.

The stock of American Express is trading at close to the midpoint between its 52 week low and its 52 week high which to us is a clear indication that the short term sentiment and momentum of American Express is neutral at this point in time.

American Express (NYSE: AXP) stock price history over the last 5 years

Recent coverage of American Express

The extract below discusses some of the latest news regarding American Express as obtained from Fool.com

Warren Buffett's favorite credit card company American Express (NYSE:AXP) held its third quarter earnings call last Friday, and results were somewhat surprising. Revenue was down 20.4% year-over-year, but that actually beat analyst expectations. However, American Express' earnings per share of $1.30 missed expectations of $1.35, and the stock sold off after the announcement.

The results run somewhat counter to what we've seen from a lot of companies in the second and third quarters, during which revenue decreases were offset by better profitability as many companies saved on travel and marketing expenses. However, American Express management has actually decided to zig while others are zagging, ramping up marketing spending on new initiatives even amid the downturn. Here's why.

Upping marketing by 23%

In contrast to just about every other business I've followed during the pandemic, American Express increased its marketing spend in the third quarter, not just relative to the second quarter, when many businesses were shut down, but actually on a year-over-year basis. "I don't know how many people had that, either in their calculus or sort of in their models, but during times like this, probably the go-to move is to reduce marketing. But we don't believe that that's true," said CEO Steve Squeri.

Of note, American Express invested in its largest-ever small business initiative during the quarter, which offered cardholders incentives to buy from local businesses. Also on the small and medium business front, Amex acquired the Kabbage data platform, which management believes will accelerate its efforts to build a digital banking platform for small businesses by 18-24 months. In addition, Amex also stepped up growth initiatives toward the end of the quarter, including new card acquisition as it got a handle on consumer behaviors, as well as officially launching its card network in China.

Read the full article here

Warren Buffett's favorite credit card company American Express (NYSE:AXP) held its third quarter earnings call last Friday, and results were somewhat surprising. Revenue was down 20.4% year-over-year, but that actually beat analyst expectations. However, American Express' earnings per share of $1.30 missed expectations of $1.35, and the stock sold off after the announcement.

The results run somewhat counter to what we've seen from a lot of companies in the second and third quarters, during which revenue decreases were offset by better profitability as many companies saved on travel and marketing expenses. However, American Express management has actually decided to zig while others are zagging, ramping up marketing spending on new initiatives even amid the downturn. Here's why.

Upping marketing by 23%

In contrast to just about every other business I've followed during the pandemic, American Express increased its marketing spend in the third quarter, not just relative to the second quarter, when many businesses were shut down, but actually on a year-over-year basis. "I don't know how many people had that, either in their calculus or sort of in their models, but during times like this, probably the go-to move is to reduce marketing. But we don't believe that that's true," said CEO Steve Squeri.

Of note, American Express invested in its largest-ever small business initiative during the quarter, which offered cardholders incentives to buy from local businesses. Also on the small and medium business front, Amex acquired the Kabbage data platform, which management believes will accelerate its efforts to build a digital banking platform for small businesses by 18-24 months. In addition, Amex also stepped up growth initiatives toward the end of the quarter, including new card acquisition as it got a handle on consumer behaviors, as well as officially launching its card network in China.

Read the full article here

American Express (NYSE: AXP) latest stock valuation

So what is American Express stock worth based on the release of their latest earnings report? Based on American Express' latest earnings report our valuation models provide a target price (full value) price of American Express stock at $127.70 a stock. Therefore we believe the stock of American Express is undervalued at its current price of $100.98

We usually recommend that long term fundamental or value investors look to enter the stock at 10% below our target price (full value price) which in this case is $127.80, so a good entry point into American Express' stock would be at $115 or below.

We expect the stock of American Express to tick up in coming weeks and months to levels closer to our target price (full value price). Since the stock of American Express is trading at well below our suggested entry price we rate the stock of American Express a buy

We usually recommend that long term fundamental or value investors look to enter the stock at 10% below our target price (full value price) which in this case is $127.80, so a good entry point into American Express' stock would be at $115 or below.

We expect the stock of American Express to tick up in coming weeks and months to levels closer to our target price (full value price). Since the stock of American Express is trading at well below our suggested entry price we rate the stock of American Express a buy

Next earnings release date for American Express

It is expected that American Express will release their 4th quarter 2020 earnings report will be released in late January 2021