|

Related Topics

|

|

Category: Stock Market and Boise Cascade

Date: 12 November 2019 Stock Price: $38.17 We take a look at the 3rd quarter earnings report of their 2019 fiscal year of Boise Cascade, one of the largest producers of engineered wood products and plywood in North America.

|

|

About Boise Cascade

Boise Cascade Company is one of the largest producers of engineered wood products and plywood in North America and a leading U.S. wholesale distributor of building products

A Boise Cascade semi-truck delivering goods

Overview of Boise Cascade's 3rd quarter 2019 earnings report

- Net sales: $1.269 billion (down from $1.338 billion for the same quarter of the previous year

- Net sales decreased by -5.1% over the last 12 months

- Costs and expenses: $1.224 billion (down from $1.308 billion for the same quarter of the previous year)

- Costs and expenses decreased by -6.4% over the last 12 months

- Net income: $27.171 million (up from $13.848 million for the same quarter of the previous year)

- Diluted earnings per share: $0.69 (down from $0.35 for the same quarter of the previous year)

- PE ratio of Boise Cascade:

- Dividend declared: $1.10

- Dividend yield of Boise Cascade: 2.89%

- Diluted weighted-average shares outstanding: 39.292 million (down from 39.461 million for the same quarter of the previous year)

- Cash and cash equivalents: $306.443 million

- Cash and cash equivalents per share: $7.79

- Cash and cash equivalents makes up 20.4% of Boise Cascade's market capital

- Cash and cash equivalents makes up 17.15% of Boise Cascade's total assets

- Accounts receivable: $295.585 million

- Accounts receivable makes up 16.6% of Boise Cascade's total assets

- Inventories: $492.588 million

- Inventories makes up 27.6% of Boise Cascade's total assets

- Stockholders equity of Boise Cascade: $731.566 million

- Stockholders equity per share: $18.62

- Boise Cascade is trading at 2.04 times its stockholders equity which is within the expected range of between 2 and 4 times that most firms tend to trade at

- Cash generated from operations (for 9 months): $194.750 million

- Cash generated from operations per share (for 9 months): $4.96

Boise Cascade's management commentary on their 3rd quarter earnings results and guidance

BOISE, Idaho - Boise Cascade Company ("Boise Cascade," the "Company," "we," or "our") (NYSE: BCC) today reported net income of $27.2 million, or $0.69 per share, on sales of $1.3 billion for the third quarter ended September 30, 2019, compared with net income of $13.8 million, or $0.35 per share, on sales of $1.3 billion for the third quarter ended September 30, 2018.

“Despite the lack of growth in residential construction and ongoing weakness in commodity wood products pricing that has persisted this year, both of our businesses continue to execute well. BMD delivered outstanding financial results during the third quarter, with solid growth in general line product sales and gross margins. With the operating footprint changes made during the last year, our favorable performance in EWP is more evident in Wood Products' results. The stability of EWP, together with input cost improvements, mitigated the overall earnings impact of the significant year-over-year decline in plywood pricing,” commented Tom Corrick, CEO. “Our operating results have positioned us to comfortably fund our bolt-on acquisitions and internal growth initiatives while strengthening our balance sheet. As part of our capital allocation process, I am pleased our board approved an 11% increase in our regular quarterly dividend to $0.10 per share, as well as a supplemental dividend of $1.00 per share, both payable in December. This is consistent with our objective of generating favorable returns on our shareholders’ invested capital. We remain well positioned to fund anticipated working capital needs in early 2020, as well as having flexibility to take advantage of internal growth initiatives and acquisition opportunities which may occur in the next six to nine months.”

Dividends

On October 30, 2019, our board of directors declared a quarterly dividend of $0.10 per share, as well as a supplemental dividend of $1.00 per share, on our common stock payable on December 16, 2019, to stockholders of record on December 2, 2019.

“Despite the lack of growth in residential construction and ongoing weakness in commodity wood products pricing that has persisted this year, both of our businesses continue to execute well. BMD delivered outstanding financial results during the third quarter, with solid growth in general line product sales and gross margins. With the operating footprint changes made during the last year, our favorable performance in EWP is more evident in Wood Products' results. The stability of EWP, together with input cost improvements, mitigated the overall earnings impact of the significant year-over-year decline in plywood pricing,” commented Tom Corrick, CEO. “Our operating results have positioned us to comfortably fund our bolt-on acquisitions and internal growth initiatives while strengthening our balance sheet. As part of our capital allocation process, I am pleased our board approved an 11% increase in our regular quarterly dividend to $0.10 per share, as well as a supplemental dividend of $1.00 per share, both payable in December. This is consistent with our objective of generating favorable returns on our shareholders’ invested capital. We remain well positioned to fund anticipated working capital needs in early 2020, as well as having flexibility to take advantage of internal growth initiatives and acquisition opportunities which may occur in the next six to nine months.”

Dividends

On October 30, 2019, our board of directors declared a quarterly dividend of $0.10 per share, as well as a supplemental dividend of $1.00 per share, on our common stock payable on December 16, 2019, to stockholders of record on December 2, 2019.

Outlook

We expect to experience seasonally slower demand growth for the products we manufacture and distribute in fourth quarter 2019. The October 2019 Blue Chip consensus forecast for 2019 and 2020 reflects 1.25 million and 1.27 million total U.S. housing starts, respectively, compared with actual housing starts of 1.25 million in 2018. Although we believe U.S. demographics are supportive of higher levels of housing starts, we expect near-term residential construction growth to be flat to slightly down due to constraints faced by builders, such as availability of labor and building lots, as well as affordability constraints faced by prospective buyers. The pace of household formation rates and residential repair-and-remodeling activity will be affected by employment growth, wage growth, prospective home buyers' access to and cost of financing, housing affordability, and consumer confidence, as well as other factors. Household formation rates in turn will be a key factor behind the demand for new construction. In addition, the size of new single-family residences as well as the mix of single and multi-family starts will influence product consumption. We will continue to manage our production levels to our sales demand. As in past years, we plan to take scheduled capital and maintenance-related downtime at certain plywood facilities during the fourth quarter.

Weak commodity products pricing experienced in the first half of 2019 continued throughout third quarter 2019 as weaker year-to-date residential construction activity and additional industry capacity brought on in 2018 have led to supply and demand imbalances. Commodity product pricing during the remainder of 2019 and into 2020 will be a key driver of our financial results and will be dependent on industry operating rates, net import and export activity, transportation constraints or disruptions, inventory levels in various distribution channels, and seasonal demand patterns. We anticipate that commodity products pricing in the fourth quarter of 2019 will remain at low absolute, although more stable, levels compared to fourth quarter 2018.

We expect our capital spending, excluding acquisitions, to be $85-$95 million in 2019, including spending to improve the efficiency of our veneer production at our Chester, South Carolina, and Florien, Louisiana, facilities. In addition, we expect our capital spending, excluding acquisitions, to also be $85-$95 million in 2020.

We expect fourth quarter 2019 financial results to be improved compared with fourth quarter 2018. Included in Wood Products fourth quarter 2018 results were certain items that negatively affected reported earnings. These items include $24.0 million of pre-tax impairment and sale related losses related to the sale of our hardwood plywood facility in Moncure, North Carolina, and $55.0 million and $2.8 million, respectively, of pre-tax accelerated depreciation and other curtailment related costs due to the permanent curtailment of LVL production at our Roxboro, North Carolina, facility.

We expect to experience seasonally slower demand growth for the products we manufacture and distribute in fourth quarter 2019. The October 2019 Blue Chip consensus forecast for 2019 and 2020 reflects 1.25 million and 1.27 million total U.S. housing starts, respectively, compared with actual housing starts of 1.25 million in 2018. Although we believe U.S. demographics are supportive of higher levels of housing starts, we expect near-term residential construction growth to be flat to slightly down due to constraints faced by builders, such as availability of labor and building lots, as well as affordability constraints faced by prospective buyers. The pace of household formation rates and residential repair-and-remodeling activity will be affected by employment growth, wage growth, prospective home buyers' access to and cost of financing, housing affordability, and consumer confidence, as well as other factors. Household formation rates in turn will be a key factor behind the demand for new construction. In addition, the size of new single-family residences as well as the mix of single and multi-family starts will influence product consumption. We will continue to manage our production levels to our sales demand. As in past years, we plan to take scheduled capital and maintenance-related downtime at certain plywood facilities during the fourth quarter.

Weak commodity products pricing experienced in the first half of 2019 continued throughout third quarter 2019 as weaker year-to-date residential construction activity and additional industry capacity brought on in 2018 have led to supply and demand imbalances. Commodity product pricing during the remainder of 2019 and into 2020 will be a key driver of our financial results and will be dependent on industry operating rates, net import and export activity, transportation constraints or disruptions, inventory levels in various distribution channels, and seasonal demand patterns. We anticipate that commodity products pricing in the fourth quarter of 2019 will remain at low absolute, although more stable, levels compared to fourth quarter 2018.

We expect our capital spending, excluding acquisitions, to be $85-$95 million in 2019, including spending to improve the efficiency of our veneer production at our Chester, South Carolina, and Florien, Louisiana, facilities. In addition, we expect our capital spending, excluding acquisitions, to also be $85-$95 million in 2020.

We expect fourth quarter 2019 financial results to be improved compared with fourth quarter 2018. Included in Wood Products fourth quarter 2018 results were certain items that negatively affected reported earnings. These items include $24.0 million of pre-tax impairment and sale related losses related to the sale of our hardwood plywood facility in Moncure, North Carolina, and $55.0 million and $2.8 million, respectively, of pre-tax accelerated depreciation and other curtailment related costs due to the permanent curtailment of LVL production at our Roxboro, North Carolina, facility.

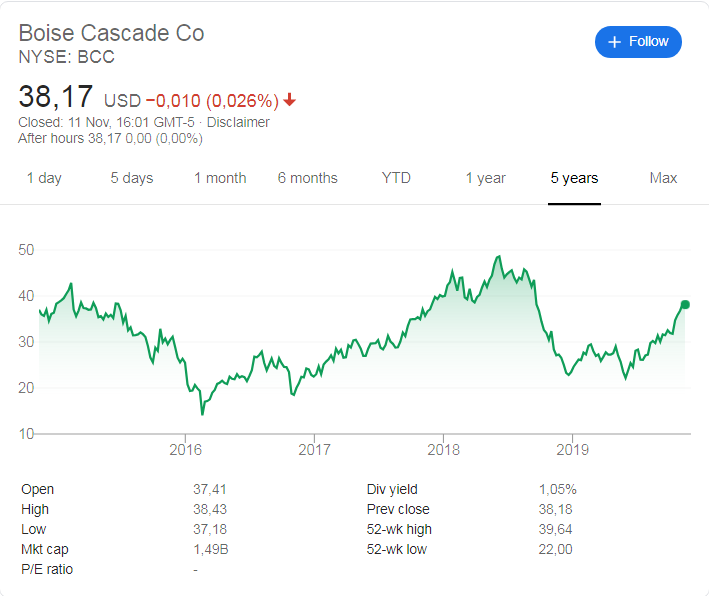

Boise Cascade (NYSE: BCC) stock price history

The image below shows the stock price history of Boise Cascade (NYSE: BCC) over the last 5 years. And it's not been a very average time for Boise Cascade stockholders. 5 years ago the stock was trading at around $37. and it is currently trading at $38.17 a stock. So over a 5 year period the stock of Boise Cascade increased by 3.2% . The stock of Boise Cascade is trading at a lot closer to its 52 week high of $39.64 than it is to its 52 low of $22 which to us is a clear indication that the short term sentiment and momentum of Boise Cascade's stock is positive.

Boise Cascade (NYSE: BCC) stock price history over the last 5 years

Recent coverage of Boise Cascade

The extract below covers the latest on Boise Cascade as obtained from TheStreet,com

Boise, Idaho, Oct. 30, 2019 (GLOBE NEWSWIRE) -- Boise Cascade Company's (Boise Cascade or the Company) (NYSE: BCC) Board of Directors has declared a quarterly dividend of $0.10 per share, an increase of $0.01 per share or 11%, as well as a supplemental dividend of $1.00 per share, to holders of its common stock. The dividends will be paid on December 16, 2019 to stockholders of record on December 2, 2019. Future dividend declarations, including amount per share, record date and payment date, will be made by the Board of Directors and will depend upon, among other things, legal capital requirements and surplus, the Company's future operations and earnings, general financial condition, contractual restrictions and other factors as the Board of Directors may deem relevant

Boise, Idaho, Oct. 30, 2019 (GLOBE NEWSWIRE) -- Boise Cascade Company's (Boise Cascade or the Company) (NYSE: BCC) Board of Directors has declared a quarterly dividend of $0.10 per share, an increase of $0.01 per share or 11%, as well as a supplemental dividend of $1.00 per share, to holders of its common stock. The dividends will be paid on December 16, 2019 to stockholders of record on December 2, 2019. Future dividend declarations, including amount per share, record date and payment date, will be made by the Board of Directors and will depend upon, among other things, legal capital requirements and surplus, the Company's future operations and earnings, general financial condition, contractual restrictions and other factors as the Board of Directors may deem relevant

Engineered Wood Products from Boise Cascade

Boise Cascade (NYSE: BCC) latest stock valuation

So what is Boise Cascade (NYSE: BCC) stock worth based on the release of their latest earnings report and their outlook provided? Based on their earnings report and the fiscal guidance provided our valuation models provide a target (full value) price for Boise Cascade at $36.00 a stock

We therefore believe that the stock of Boise Cascade is close to being fully valued as the stock is trading at close to our target (full value) price.

We usually suggest long term investors look to enter a stock at least 10% below our target (full value) price which in this case is $36.00. A good entry point into Boise Cascade stock would be at $32.40 or below. We expect the stock of Boise Cascade to trade in a narrow range around our target (full value) price in coming weeks and months until there is a new catalyst to provide direction for the company's stock price

We therefore believe that the stock of Boise Cascade is close to being fully valued as the stock is trading at close to our target (full value) price.

We usually suggest long term investors look to enter a stock at least 10% below our target (full value) price which in this case is $36.00. A good entry point into Boise Cascade stock would be at $32.40 or below. We expect the stock of Boise Cascade to trade in a narrow range around our target (full value) price in coming weeks and months until there is a new catalyst to provide direction for the company's stock price

Next earnings release for Boise Cascade

It is expected that Boise Cascade's 4th quarter and full fiscal 2019 earnings will be released towards the middle of February 2020