Delta Airlines (DAL) earnings release for the 2nd quarter of their 2021 fiscal year

|

Category: Delta Airlines (DAL)

Date: 15 July 2021 Stock Price of Delta (DAL): $40.68 Market Capital of Delta (DAL): $26 billion We take a look at the 2nd quarter earnings report of their 2021 fiscal year of Delta Airlines, a U.S global airline company that used to have over 5000 departing flights on a daily basis across the world. For the quarter the group reported GAAP revenues of $7.12 billion and reported net income of $652 million.

|

|

Ed Bastian, Delta's chief executive officer - Looking forward, we are harnessing the power of our differentiated brand and resilient competitive advantages to drive towards sustainable profitability in the second half of 2021 and enable long-term value creation"

About Delta Airlines (DAL)

Delta Air Lines (NYSE: DAL) is the U.S. global airline leader in products, services, innovation, reliability and customer experience. Powered by its 80,000 people around the world, Delta continues to invest in its people, improving the air travel experience and generating industry-leading shareholder returns.

Headquartered in Atlanta, Delta offers more than 5,000 daily departures and as many as 15,000 affiliated departures including the premier SkyTeam alliance, of which Delta is a founding member. Delta serves nearly 200 million people every year, taking customers across its industry-leading global network to more than 300 destinations in over 50 countries.

Headquartered in Atlanta, Delta offers more than 5,000 daily departures and as many as 15,000 affiliated departures including the premier SkyTeam alliance, of which Delta is a founding member. Delta serves nearly 200 million people every year, taking customers across its industry-leading global network to more than 300 destinations in over 50 countries.

Overview of Delta Airlines' 2nd quarter 2021 earnings report

June Quarter Financial Results

- Adjusted non GAAP pre-tax loss of $881 million excludes $1.5 billion of benefit related to the first and second payroll support program extensions (PSP2 and PSP3, respectively) and mark-to-market adjustments on our investments

- Adjusted operating revenue of $6.3 billion, which excludes refinery sales, declined 49 percent on 39 percent lower sellable capacity (see Note A) versus June quarter 2019

- Total operating expense, which includes $1.5 billion of benefit related to PSP2 and PSP3, decreased $4.1 billion relative to the June quarter 2019. Adjusted for the benefit related to the PSP programs and third-party refinery sales, total operating expense decreased $3.3 billion or 32 percent in the June quarter 2021 versus the comparable 2019 period

- Generated $1.9 billion of operating cash flow, $1.5 billion of free cash flow and $195 million of free cash flow, adjusted in the June quarter

- At the end of the June quarter, the company had $17.8 billion in liquidity, including cash and cash equivalents, short-term investments and undrawn revolving credit facilities. The company had total debt and finance lease obligations of $29.1 billion with adjusted net debt of $18.3 billion

Delta Airlines' management commentary on their 4th quarter 2020 earnings report

ATLANTA, July 14, 2021 /PRNewswire/ -- Delta Air Lines (NYSE:DAL) today reported financial results for the June quarter 2021 and provided its outlook for the September quarter 2021. Highlights of the June quarter 2021 results, including both GAAP and adjusted metrics, are on page six and are incorporated here.

"With the best employees and operation in the industry and an accelerating demand environment, we achieved significant milestones in the quarter including a solid pre-tax profit in the month of June, positive free cash flow for the June quarter, and our people and our brand being recognized with the top spot in the J.D. Power 2021 Airline Study," said Ed Bastian, Delta's chief executive officer. "Looking forward, we are harnessing the power of our differentiated brand and resilient competitive advantages to drive towards sustainable profitability in the second half of 2021 and enable long-term value creation."

"Domestic leisure travel is fully recovered to 2019 levels and there are encouraging signs of improvement in business and international travel. With the recovery picking up steam, we are making investments to support our industry-leading operation. We are also opportunistically acquiring aircraft and creating upside flexibility to accelerate our capacity restoration in 2022 and beyond in a capital-disciplined manner," he said.

"With the best employees and operation in the industry and an accelerating demand environment, we achieved significant milestones in the quarter including a solid pre-tax profit in the month of June, positive free cash flow for the June quarter, and our people and our brand being recognized with the top spot in the J.D. Power 2021 Airline Study," said Ed Bastian, Delta's chief executive officer. "Looking forward, we are harnessing the power of our differentiated brand and resilient competitive advantages to drive towards sustainable profitability in the second half of 2021 and enable long-term value creation."

"Domestic leisure travel is fully recovered to 2019 levels and there are encouraging signs of improvement in business and international travel. With the recovery picking up steam, we are making investments to support our industry-leading operation. We are also opportunistically acquiring aircraft and creating upside flexibility to accelerate our capacity restoration in 2022 and beyond in a capital-disciplined manner," he said.

Revenue Environment

"With accelerating demand for air travel and growing affinity for Delta's best-in-class products, June quarter adjusted operating revenue improved 76 percent from the March quarter. Increasing customer engagement is evident with spend on the American Express co-brand credit card already exceeding 2019 levels and a record number of new customers signing up for SkyMiles accounts during the June month," said Glen Hauenstein, Delta's president. "I am excited to see this momentum continuing in the September quarter as business travel rebounds and international markets continue to reopen."

"We have the industry's best domestic and global network, an increasingly efficient and simplified fleet, a de-commoditized product, a highly valued brand, and the industry's best employees," Hauenstein continued. "Combined with our more efficient cost structure, we are on a path to improve on pre-pandemic margins and generate sustainable free cash flow."

Adjusted operating revenue of $6.3 billion for the June quarter improved 76 percent from March quarter 2021. Compared to the same period in 2019, adjusted operating revenue declined 49 percent, an improvement from the company's guidance update in June of down 50 to 52 percent. Passenger revenue declined 53 percent in the June quarter 2021 compared to June quarter 2019 on 32 percent lower scheduled capacity and 39 percent lower sellable capacity, which included the blocking of the middle seat through the month of April 2021.

Total unit revenue, adjusted was 45.4 percent higher than the March quarter 2021 as adjusted operating revenue grew 76 percent on a 21 percent increase in scheduled capacity over the same period. Compared to the March quarter 2021, system yields improved 4.8 percent and load factors improved 24 points.

Revenue-related Highlights:

Cost Performance

"The cost performance in the first half of the year was strong as we continue to restore the business efficiently. September quarter non-fuel CASM is expected to be between 11 percent and 14 percent above the same period in 2019 as the significantly improving demand environment is driving some welcome cost pressures with an increase in rebuild and selling-related costs," said Gary Chase, Delta's interim co-chief financial officer. "As we continue to leverage our network restoration, we remain on a path to achieve non-fuel CASM below 2019 levels by the fourth quarter," he said.

Total adjusted operating expense for the June quarter decreased $3.3 billion excluding $1.5 billion in benefits from PSP2 and PSP3. Expense performance was driven by an $811 million, or 36 percent reduction in fuel expense, adjusted versus the June quarter 2019, a 34 percent reduction in maintenance expense, and lower volume- and revenue-related expenses. Salaries and related costs and profit sharing of $2.3 billion were down 31 percent compared to the June quarter 2019.

Fuel efficiency (see Note A) improved 7.1 percent in the June quarter versus the same period in 2019, with nearly five points of the improvement a result of our fleet renewal efforts, with the remaining improvement temporary in nature due to reduced airport congestion and lower load factors. Adjusted fuel price of $2.12 per gallon was up 11.1 percent compared to the March qarter 2021 and higher than initial guidance in April on increased market prices and losses at the refinery equivalent to 23¢ per gallon.

CASM, adjusted was up 0.5 percent compared to June quarter 2019. CASM-Ex was 9.0 percent higher than the June quarter 2019 on 32 percent less capacity. The company saw four points of CASM-Ex pressure related to rebuild expense, including accelerated maintenance, training and hiring to prepare for summer 2022 flying. Additionally, the company made the decision to reward our employees for winning the J.D. Power Award for #1 North American Airline with travel passes, which drove 1.3 points of non-cash CASM-Ex expense in the quarter. CASM-Ex declined 12.3 percent sequentially from operating leverage on a 21 percent increase in scheduled capacity and realized savings from the employee retention tax credit and third-party rate reductions.

Non-operating expense for the June quarter was down $181 million compared to the June quarter 2019, driven primarily by mark-to-market gains on certain of our investments, partially offset by higher interest expense.

Balance Sheet, Cash and Liquidity

"Improving financial performance and a strong liquidity position enable us to use cash on the balance sheet to reduce leverage, and restore our financial flexibility," Chase said. "Strengthening our financial foundation remains a top priority at Delta as we position for the future and deliver value to our owners," he said.

At the end of the June quarter, the company had total debt and finance lease obligations of $29.1 billion with adjusted net debt of $18.3 billion, $7.8 billion higher than December 2019. The company's total debt had a weighted average interest rate of 4.3 percent at June quarter-end. In addition to maturities and normal amortizations of nearly $875 million, the company prepaid approximately $450 million in aircraft-related debt during the quarter.

As previously announced, Delta voluntarily contributed $1.5 billion into its pension plans during the quarter. By year-end 2021, the company expects the plans to be fully funded on a Pension Protection Act (PPA) basis based on terms included in the American Rescue Plan Act of 2021 and to achieve GAAP funding of 90 percent. At this level of funding, investment returns are expected to satisfy future benefit payments, which the company believes will eliminate any need for material cash contributions to the pension plans going forward. With the plans frozen to new participants, Delta began to reduce the investment risk of the plans during the quarter to protect the funded status.

Since October 2020, Delta has reduced its financial obligations by $11 billion, freeing $6 billion in collateral and driving $500 million in annualized pension and interest expense savings.

Cash generated from operations during the quarter was $1.9 billion, including the benefit from the payroll support programs. Free cash flow was $1.5 billion, with free cash flow, adjusted of $195 million for the quarter. With consumer travel demand returning at an accelerated rate, the company's Air Traffic Liability increased approximately $1.5 billion quarter-over-quarter to $6.9 billion, approximately $300 million higher than at June quarter 2019. Travel credits represent 35 percent of the Air Traffic Liability and represent approximately 5 percent of average daily bookings.

Delta ended the June quarter with $17.8 billion in liquidity, including $2.6 billion in undrawn revolver capacity.

"With accelerating demand for air travel and growing affinity for Delta's best-in-class products, June quarter adjusted operating revenue improved 76 percent from the March quarter. Increasing customer engagement is evident with spend on the American Express co-brand credit card already exceeding 2019 levels and a record number of new customers signing up for SkyMiles accounts during the June month," said Glen Hauenstein, Delta's president. "I am excited to see this momentum continuing in the September quarter as business travel rebounds and international markets continue to reopen."

"We have the industry's best domestic and global network, an increasingly efficient and simplified fleet, a de-commoditized product, a highly valued brand, and the industry's best employees," Hauenstein continued. "Combined with our more efficient cost structure, we are on a path to improve on pre-pandemic margins and generate sustainable free cash flow."

Adjusted operating revenue of $6.3 billion for the June quarter improved 76 percent from March quarter 2021. Compared to the same period in 2019, adjusted operating revenue declined 49 percent, an improvement from the company's guidance update in June of down 50 to 52 percent. Passenger revenue declined 53 percent in the June quarter 2021 compared to June quarter 2019 on 32 percent lower scheduled capacity and 39 percent lower sellable capacity, which included the blocking of the middle seat through the month of April 2021.

Total unit revenue, adjusted was 45.4 percent higher than the March quarter 2021 as adjusted operating revenue grew 76 percent on a 21 percent increase in scheduled capacity over the same period. Compared to the March quarter 2021, system yields improved 4.8 percent and load factors improved 24 points.

Revenue-related Highlights:

- Booking curve normalized as customers made future travel plans: Average daily net cash sales, defined as tickets purchased less tickets refunded, doubled compared to the March quarter and were 20 percent higher than our initial internal forecast. For the month of June, our average daily net cash sales were 70 percent restored to 2019 levels and roughly 10 points ahead of revenue recovery as consumers continue to make future travel plans.

- Premium cabins outperformed main cabin where demand is strongest: Domestic and short-haul Latin premium revenue outperformed main cabin revenue recovery by 5 to 10 points during the quarter. This recovery is expected to be reflected at a system level as premium revenue in other entities continues to improve with the return of business and international travel at scale.

- Pace of corporate recovery accelerated during the quarter: Corporate volumes experienced steady improvement through the quarter, doubling from 20 percent recovered in March to 40 percent recovered in June, driven by increased vaccination rates, the re-opening of offices and improvements in demand in business-heavy markets like New York and Boston.

- Non-ticket revenue demonstrated resilience: Non-ticket revenue continued to demonstrate resilience, with cargo revenue up 35 percent versus the June quarter 2019 and total loyalty revenue down 30 percent, a 17 percent and 43 percent improvement from the March quarter 2021, respectively.

- Remuneration from American Express returned to 2019 levels in June: American Express remuneration in the quarter was more than 90 percent recovered compared to June quarter 2019 levels as co-brand card spend surpassed 2019 levels while co-brand card acquisitions were nearly fully restored. For the month of June, remuneration exceeded 2019 levels and is expected to remain at or above 2019 levels in the second half.

Cost Performance

"The cost performance in the first half of the year was strong as we continue to restore the business efficiently. September quarter non-fuel CASM is expected to be between 11 percent and 14 percent above the same period in 2019 as the significantly improving demand environment is driving some welcome cost pressures with an increase in rebuild and selling-related costs," said Gary Chase, Delta's interim co-chief financial officer. "As we continue to leverage our network restoration, we remain on a path to achieve non-fuel CASM below 2019 levels by the fourth quarter," he said.

Total adjusted operating expense for the June quarter decreased $3.3 billion excluding $1.5 billion in benefits from PSP2 and PSP3. Expense performance was driven by an $811 million, or 36 percent reduction in fuel expense, adjusted versus the June quarter 2019, a 34 percent reduction in maintenance expense, and lower volume- and revenue-related expenses. Salaries and related costs and profit sharing of $2.3 billion were down 31 percent compared to the June quarter 2019.

Fuel efficiency (see Note A) improved 7.1 percent in the June quarter versus the same period in 2019, with nearly five points of the improvement a result of our fleet renewal efforts, with the remaining improvement temporary in nature due to reduced airport congestion and lower load factors. Adjusted fuel price of $2.12 per gallon was up 11.1 percent compared to the March qarter 2021 and higher than initial guidance in April on increased market prices and losses at the refinery equivalent to 23¢ per gallon.

CASM, adjusted was up 0.5 percent compared to June quarter 2019. CASM-Ex was 9.0 percent higher than the June quarter 2019 on 32 percent less capacity. The company saw four points of CASM-Ex pressure related to rebuild expense, including accelerated maintenance, training and hiring to prepare for summer 2022 flying. Additionally, the company made the decision to reward our employees for winning the J.D. Power Award for #1 North American Airline with travel passes, which drove 1.3 points of non-cash CASM-Ex expense in the quarter. CASM-Ex declined 12.3 percent sequentially from operating leverage on a 21 percent increase in scheduled capacity and realized savings from the employee retention tax credit and third-party rate reductions.

Non-operating expense for the June quarter was down $181 million compared to the June quarter 2019, driven primarily by mark-to-market gains on certain of our investments, partially offset by higher interest expense.

Balance Sheet, Cash and Liquidity

"Improving financial performance and a strong liquidity position enable us to use cash on the balance sheet to reduce leverage, and restore our financial flexibility," Chase said. "Strengthening our financial foundation remains a top priority at Delta as we position for the future and deliver value to our owners," he said.

At the end of the June quarter, the company had total debt and finance lease obligations of $29.1 billion with adjusted net debt of $18.3 billion, $7.8 billion higher than December 2019. The company's total debt had a weighted average interest rate of 4.3 percent at June quarter-end. In addition to maturities and normal amortizations of nearly $875 million, the company prepaid approximately $450 million in aircraft-related debt during the quarter.

As previously announced, Delta voluntarily contributed $1.5 billion into its pension plans during the quarter. By year-end 2021, the company expects the plans to be fully funded on a Pension Protection Act (PPA) basis based on terms included in the American Rescue Plan Act of 2021 and to achieve GAAP funding of 90 percent. At this level of funding, investment returns are expected to satisfy future benefit payments, which the company believes will eliminate any need for material cash contributions to the pension plans going forward. With the plans frozen to new participants, Delta began to reduce the investment risk of the plans during the quarter to protect the funded status.

Since October 2020, Delta has reduced its financial obligations by $11 billion, freeing $6 billion in collateral and driving $500 million in annualized pension and interest expense savings.

Cash generated from operations during the quarter was $1.9 billion, including the benefit from the payroll support programs. Free cash flow was $1.5 billion, with free cash flow, adjusted of $195 million for the quarter. With consumer travel demand returning at an accelerated rate, the company's Air Traffic Liability increased approximately $1.5 billion quarter-over-quarter to $6.9 billion, approximately $300 million higher than at June quarter 2019. Travel credits represent 35 percent of the Air Traffic Liability and represent approximately 5 percent of average daily bookings.

Delta ended the June quarter with $17.8 billion in liquidity, including $2.6 billion in undrawn revolver capacity.

Delta Airlines (DAL) stock chart over the last 5 years

The image below shows the stock price history of Delta Airlines (DAL) over the last 5 years. And its not been a good time for Delta Airlines stockholders with the stock increasing by a mere 9.5% over the last 5 years. Not the type of returns investors would like to see but considering the impact of Covid-19 any gain by airline stocks over this period should be celebrated.

The stock of Delta Airlines is trading at close to the midpoint between its 52 week high and 52 week low which is an indication to us that the short term sentiment and momentum of Delta's stock is neutral at this point in time.

The stock of Delta Airlines is trading at close to the midpoint between its 52 week high and 52 week low which is an indication to us that the short term sentiment and momentum of Delta's stock is neutral at this point in time.

Delta Airlines (DAL) stock chart over the last 5 years

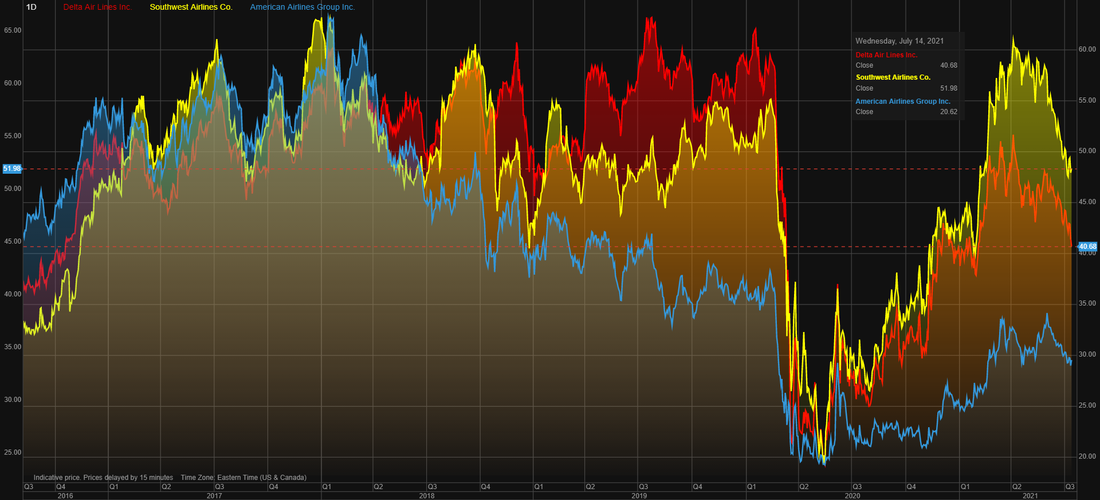

Delta (DAL) vs Southwest Airlines (LUV) vs American Airlines (AAL) stock over last 5 years

The image below shows the stock price performance of Delta Airlines (DAL), Southwestern (LUV) and American Airlines (AAL) over the last 5 years. As the image shows its been a pretty horrible time for the stocks of airline companies. Over the 5 year period all three these airline stocks lost investors money. Below the returns of the three airline stocks (sorted from best to worst performer)

- Southwest Airlines: 38.8%

- Delta Airlines: 9.5%

- American Airlines: -40.4%

Delta (DAL) vs Southwest Airlines (LUV) vs American Airlines (AAL) stock over last 5 years

Delta Airlines ( DAL) latest stock valuation

So what is Delta Airlines' stock worth based on the release of their 2nd quarter 2021 earnings report provided by Delta Airlines? Based on the latest earnings results, and the difficult period Delta is facing our valuation models provide a target price (full value price) for Delta Airlines at $62.10 a Delta Airlines stock (up slightly from our 4th quarter 2020 earnings report valuation of Delta Airlines). Thus we forecast a stock price for Delta Airlines by year end of $62.10

We therefore believe that the stock is undervalued at its current price of $40.68

We usually suggest long term fundamental or value investors look to enter into a stock at least 10% below our target price (full value price) which in this case is $62.10. Therefore we see a good entry point into Delta Airlines stock at $55.90 or below.

Since Delta Airlines is trading at well below our suggested entry point into the stock we rate Delta Airlines as a buy.

We therefore believe that the stock is undervalued at its current price of $40.68

We usually suggest long term fundamental or value investors look to enter into a stock at least 10% below our target price (full value price) which in this case is $62.10. Therefore we see a good entry point into Delta Airlines stock at $55.90 or below.

Since Delta Airlines is trading at well below our suggested entry point into the stock we rate Delta Airlines as a buy.

Delta Airlines planes at boarding gates

Next earnings release of Delta Airlines

It is expected that Delta Airlines will release their 3rd quarter 2021 earnings report in middle October 2021