Helen of Troy (HELE) earnings release review for the 1st quarter of their 2022 fiscal year

|

Category: Helen of Troy (HELE)

Date: 10 July 2021 Stock Price of Helen of Troy: $215.25 Market Capital of Helen of Troy: $5.2 billion We take a look at the 1st quarter earnings report of their 2022 fiscal year of Helen of Troy, a global consumer products company whose brands include Vicks, Hydro flask, OXO and Braun. For the quarter the group reported net revenues of $541.2 million and net income of $60.28 million

|

|

Julien R. Mininberg, Chief Executive Officer - We delivered an outstanding first quarter, with even higher sales growth and stronger profitability than we expected. The 28.6% sales growth was broad based, with Beauty and Housewares leading the way as re-openings drove store traffic and our brands continued to distinguish themselves with consumers"

About Helen of Troy (HELE)

Helen of Troy Limited (NASDAQ: HELE) is a leading global consumer products company offering creative solutions for its customers through a strong portfolio of well-recognized and widely-trusted brands, including OXO, Hydro Flask, Vicks, Braun, Honeywell, PUR, and Hot Tools. All trademarks herein belong to Helen of Troy Limited (or its affiliates) and/or are used under license from their respective licensors.

Overview of Helen of Troy's 1st quarter 2022 earnings report

- Consolidated net sales revenue increase of 28.6% to $541.2 million, including:

- An increase in Leadership Brand net sales of 22.9%

- An increase in online channel net sales of approximately 4%

- Organic business net sales growth of 27.3%

- Core business net sales growth of 28.9%

- GAAP consolidated operating income of $64.8 million, or 12.0% of net sales, which includes $13.1 million in EPA compliance costs, compared to $57.0 million, or 13.5% of net sales, for the same period last year

- Non-GAAP consolidated adjusted operating income increase of 33.6% to $95.0 million, or 17.5% of net sales, compared to $71.1 million, or 16.9% of net sales, for the same period last year

- GAAP diluted EPS of $2.31, which includes EPA compliance costs of $0.52 per share, compared to $2.37 for the same period last year

- Non-GAAP adjusted diluted EPS increase of 37.5% to $3.48, compared to $2.53 for the same period last year

- Repurchased 436,842 shares of common stock in the open market during the quarter for $95.5 million, at an average price of $218.58 per share

Helen of Troy's management commentary on their 1st quarter 2022 earnings report

EL PASO, Texas--(BUSINESS WIRE)-- Helen of Troy Limited (NASDAQ:HELE), designer, developer and worldwide marketer of consumer brand-name housewares, health and home, and beauty products, today reported results for the three-month period ended May 31, 2021.

Julien R. Mininberg, Chief Executive Officer, stated: “We delivered an outstanding first quarter, with even higher sales growth and stronger profitability than we expected. The 28.6% sales growth was broad based, with Beauty and Housewares leading the way as re-openings drove store traffic and our brands continued to distinguish themselves with consumers. Health & Home also grew, surpassing the very large COVID-related first quarter base laid down a year ago. International sales grew even faster than the fleet average as this strategic focus area benefited from prior flywheel investments. We grew adjusted EPS by 37.5%, as the very strong sales growth more than offset normalized spending versus last year and headwinds from widespread inflation affecting nearly all input costs including materials, labor, and transportation.

So far in Fiscal 2022, we have continued to take actions intended to drive long-term value for shareholders. We divested our Personal Care business in line with our long-term strategy to focus on our Leadership Brands, finalized a land purchase in Gallaway, Tennessee to build a state-of-the-art distribution center which will have high levels of automation and scalable direct-to-consumer capability, and re-purchased just under 2% of our stock. We also secured more inventory ahead of the more recent cost increases in the market, positioning us well to continue to meet demand and better manage the current period of inflation and global supply chain disruption.”

Mr. Mininberg continued: “Looking ahead to full fiscal 2022, we are now in a position to provide an outlook. Our Housewares and Beauty segments are each projecting healthy growth in revenue and profitability on top of their strong growth last year. Our projection in Health & Home includes the estimated impact of lost sales volume related to the EPA matter. Our rapid response team is working to bring this to resolution as quickly as possible. Excluding the impact of the EPA matter, we were on track to achieve growth in both Core net sales and Core adjusted EPS, which is in line with the thinking we communicated in April.

Longer term, we remain committed to our Phase II Transformation Plan and expect to return to our Phase II targets of average annual organic revenue growth of 3% and adjusted EPS growth of 8% in Fiscal 2023 and Fiscal 2024. We also remain actively focused on acquisition opportunities to further accelerate long-term value creation.”

Julien R. Mininberg, Chief Executive Officer, stated: “We delivered an outstanding first quarter, with even higher sales growth and stronger profitability than we expected. The 28.6% sales growth was broad based, with Beauty and Housewares leading the way as re-openings drove store traffic and our brands continued to distinguish themselves with consumers. Health & Home also grew, surpassing the very large COVID-related first quarter base laid down a year ago. International sales grew even faster than the fleet average as this strategic focus area benefited from prior flywheel investments. We grew adjusted EPS by 37.5%, as the very strong sales growth more than offset normalized spending versus last year and headwinds from widespread inflation affecting nearly all input costs including materials, labor, and transportation.

So far in Fiscal 2022, we have continued to take actions intended to drive long-term value for shareholders. We divested our Personal Care business in line with our long-term strategy to focus on our Leadership Brands, finalized a land purchase in Gallaway, Tennessee to build a state-of-the-art distribution center which will have high levels of automation and scalable direct-to-consumer capability, and re-purchased just under 2% of our stock. We also secured more inventory ahead of the more recent cost increases in the market, positioning us well to continue to meet demand and better manage the current period of inflation and global supply chain disruption.”

Mr. Mininberg continued: “Looking ahead to full fiscal 2022, we are now in a position to provide an outlook. Our Housewares and Beauty segments are each projecting healthy growth in revenue and profitability on top of their strong growth last year. Our projection in Health & Home includes the estimated impact of lost sales volume related to the EPA matter. Our rapid response team is working to bring this to resolution as quickly as possible. Excluding the impact of the EPA matter, we were on track to achieve growth in both Core net sales and Core adjusted EPS, which is in line with the thinking we communicated in April.

Longer term, we remain committed to our Phase II Transformation Plan and expect to return to our Phase II targets of average annual organic revenue growth of 3% and adjusted EPS growth of 8% in Fiscal 2023 and Fiscal 2024. We also remain actively focused on acquisition opportunities to further accelerate long-term value creation.”

Balance Sheet and Cash Flow Highlights - First Quarter Fiscal 2022 Compared to First Quarter Fiscal 2021

Subsequent Event

On June 7, 2021, the Company completed the sale of its Personal Care business, not including the Latin America and Caribbean regions, to HRB Brands LLC for $44.7 million in cash. The sale also includes an option that provides HRB Brands LLC the right to purchase the Latin America and Caribbean Personal Care businesses no later than the end of fiscal 2022, subject to meeting certain agreed-upon conditions. The carrying amount of the identified assets and liabilities within the disposal group were classified as held for sale as of May 31, 2021. The transaction is not reflected in the Company's condensed consolidated financial statements as of and for the period ended May 31, 2021.

Fiscal 2022 Annual Outlook

Due to the sale of the majority of the Personal Care business during the second quarter of fiscal 2022 and the expected continued classification of the remaining Latin America and Caribbean Personal Care business as Non-Core for fiscal 2022, the outlook the Company is providing is on both a consolidated and Core business basis in order to provide comparability between historical and future periods.

The Company's outlook includes the current estimated impact of the duration of the EPA-related stop shipment action previously discussed, which is based on the estimated timing of approval and implementation of the Company's compliance plans. The Company's outlook includes an estimated unfavorable sales revenue impact of $110 to $135 million and an unfavorable adjusted diluted EPS impact of $0.70 to $1.00 related to lost sales volume and earnings due to the EPA matter. The adjusted diluted EPS impact is net of the favorable impact of cost reduction actions being taken in the Health & Home segment, which include significant reductions in personnel, marketing and select new product development costs.

The Company incurred $13.1 million of EPA compliance costs in the first quarter of fiscal 2022 in conjunction with the implementation of its compliance plans. These costs were included in our GAAP operating results but were excluded in our non-GAAP adjusted operating results. The Company expects to incur additional EPA compliance costs, which may include costs to relabel or repackage existing inventory as well as incremental freight and storage costs, among other things. The Company expects to continue to exclude these costs from non-GAAP adjusted operating results, and the costs have been excluded from the annual outlook for non-GAAP adjusted diluted EPS.

The Company expects consolidated net sales revenue in the range of $1.93 to $1.98 billion, which implies a decline of 8.0% to 5.5%. The Company expects Core net sales revenue in the range of $1.9 to $1.95 billion, which implies a decline of 6.0% to 3.5%, which includes 6.7% to 5.4% of unfavorable impact related to the EPA matter.

The Company’s net sales outlook reflects the following expectations by segment:

The Company expects consolidated GAAP diluted EPS of $6.80 to $7.49 and Core diluted EPS of $6.60 to $7.28. The Company expects consolidated non-GAAP adjusted diluted EPS in the range of $10.46 to $10.97 and Core adjusted diluted EPS in the range of $10.25 to $10.75, which excludes any EPA compliance costs, asset impairment charges, restructuring charges, tax reform, share-based compensation expense and intangible asset amortization expense. The Company's Core adjusted diluted EPS outlook implies a decline of 7.0% to 2.5%, which includes 9.1% to 6.3% of impact due to the EPA matter, implying year-over-year growth of 2.1% to 3.8% not including the impact of the EPA matter.

The Company’s outlook also includes year-over-year inflationary cost pressures of approximately $55 to $60 million, or approximately $2.25 to $2.45 of adjusted diluted EPS, much of which have been mitigated through improved product mix, price increases, forward buying of inventory to delay cost impacts, utilizing previously negotiated shipping contracts at rates below current market prices, and implementing other cost reduction initiatives.

The Company’s consolidated and Core net sales and EPS outlook reflect the following:

Due to the strong growth comparison and COVID-related events in fiscal 2021, and the timing of the estimated impacts of the shipping restrictions related to the EPA matter, the Company expects consolidated Core net sales growth for fiscal 2022 to be concentrated entirely in the first quarter of the fiscal year. The Company also expects Core adjusted diluted EPS growth for fiscal 2022 to be concentrated in the first and fourth quarters of the fiscal year, with the second quarter expected to be the most impacted by the shipping restrictions as well as having the most challenging growth comparison to the prior fiscal year.

The Company expects a reported consolidated GAAP effective tax rate range of 13.0% to 14.0%, and a Core GAAP effective tax rate range of 12.8% to 13.8% for the full fiscal year 2022. The Company expects a consolidated adjusted effective tax rate range of 10.1% to 11.1% and a Core adjusted effective tax rate range of 9.9% to 10.9%.

The Company expects capital asset expenditures of $100 to $125 million for the full fiscal year 2022, which includes expected initial expenditures related to a new 2 million square foot distribution facility with state-of-the-art automation for the Housewares segment. The Company expects the total cost of the new distribution center and equipment to be in the range of $200 to $225 million spread over fiscal years 2022 and 2023, assuming construction and equipment costs remain at current levels.

- Cash and cash equivalents totaled $37.4 million, compared to $88.5 million.

- Accounts receivable turnover was 67.4 days, compared to 67.5 days.

- Inventory was $540.1 million, compared to $276.3 million. Trailing twelve-month inventory turnover was 3.0 times compared to 3.2 times.

- Total short- and long-term debt was $511.0 million, compared to $324.9 million.

- Net cash used by operating activities for the first three months of the fiscal year was $63.4 million, compared to net cash provided of $92.8 million for the same period last year.

Subsequent Event

On June 7, 2021, the Company completed the sale of its Personal Care business, not including the Latin America and Caribbean regions, to HRB Brands LLC for $44.7 million in cash. The sale also includes an option that provides HRB Brands LLC the right to purchase the Latin America and Caribbean Personal Care businesses no later than the end of fiscal 2022, subject to meeting certain agreed-upon conditions. The carrying amount of the identified assets and liabilities within the disposal group were classified as held for sale as of May 31, 2021. The transaction is not reflected in the Company's condensed consolidated financial statements as of and for the period ended May 31, 2021.

Fiscal 2022 Annual Outlook

Due to the sale of the majority of the Personal Care business during the second quarter of fiscal 2022 and the expected continued classification of the remaining Latin America and Caribbean Personal Care business as Non-Core for fiscal 2022, the outlook the Company is providing is on both a consolidated and Core business basis in order to provide comparability between historical and future periods.

The Company's outlook includes the current estimated impact of the duration of the EPA-related stop shipment action previously discussed, which is based on the estimated timing of approval and implementation of the Company's compliance plans. The Company's outlook includes an estimated unfavorable sales revenue impact of $110 to $135 million and an unfavorable adjusted diluted EPS impact of $0.70 to $1.00 related to lost sales volume and earnings due to the EPA matter. The adjusted diluted EPS impact is net of the favorable impact of cost reduction actions being taken in the Health & Home segment, which include significant reductions in personnel, marketing and select new product development costs.

The Company incurred $13.1 million of EPA compliance costs in the first quarter of fiscal 2022 in conjunction with the implementation of its compliance plans. These costs were included in our GAAP operating results but were excluded in our non-GAAP adjusted operating results. The Company expects to incur additional EPA compliance costs, which may include costs to relabel or repackage existing inventory as well as incremental freight and storage costs, among other things. The Company expects to continue to exclude these costs from non-GAAP adjusted operating results, and the costs have been excluded from the annual outlook for non-GAAP adjusted diluted EPS.

The Company expects consolidated net sales revenue in the range of $1.93 to $1.98 billion, which implies a decline of 8.0% to 5.5%. The Company expects Core net sales revenue in the range of $1.9 to $1.95 billion, which implies a decline of 6.0% to 3.5%, which includes 6.7% to 5.4% of unfavorable impact related to the EPA matter.

The Company’s net sales outlook reflects the following expectations by segment:

- Housewares net sales growth of 7.0% to 9.0%;

- Health & Home net sales decline of 27.0% to 24.0%, including 15.2% to 12.4% of decline related to the EPA matter; and

- Beauty net sales growth of 4.2% to 6.3%; Beauty Core net sales growth of 17.0% to 19.0%.

The Company expects consolidated GAAP diluted EPS of $6.80 to $7.49 and Core diluted EPS of $6.60 to $7.28. The Company expects consolidated non-GAAP adjusted diluted EPS in the range of $10.46 to $10.97 and Core adjusted diluted EPS in the range of $10.25 to $10.75, which excludes any EPA compliance costs, asset impairment charges, restructuring charges, tax reform, share-based compensation expense and intangible asset amortization expense. The Company's Core adjusted diluted EPS outlook implies a decline of 7.0% to 2.5%, which includes 9.1% to 6.3% of impact due to the EPA matter, implying year-over-year growth of 2.1% to 3.8% not including the impact of the EPA matter.

The Company’s outlook also includes year-over-year inflationary cost pressures of approximately $55 to $60 million, or approximately $2.25 to $2.45 of adjusted diluted EPS, much of which have been mitigated through improved product mix, price increases, forward buying of inventory to delay cost impacts, utilizing previously negotiated shipping contracts at rates below current market prices, and implementing other cost reduction initiatives.

The Company’s consolidated and Core net sales and EPS outlook reflect the following:

- the assumption that the severity of the cough/cold/flu season will be in line with pre-COVID historical averages;

- the assumption that June 2021 foreign currency exchange rates will remain constant for the remainder of the fiscal year; and

- an estimated weighted average diluted shares outstanding of 24.4 million.

Due to the strong growth comparison and COVID-related events in fiscal 2021, and the timing of the estimated impacts of the shipping restrictions related to the EPA matter, the Company expects consolidated Core net sales growth for fiscal 2022 to be concentrated entirely in the first quarter of the fiscal year. The Company also expects Core adjusted diluted EPS growth for fiscal 2022 to be concentrated in the first and fourth quarters of the fiscal year, with the second quarter expected to be the most impacted by the shipping restrictions as well as having the most challenging growth comparison to the prior fiscal year.

The Company expects a reported consolidated GAAP effective tax rate range of 13.0% to 14.0%, and a Core GAAP effective tax rate range of 12.8% to 13.8% for the full fiscal year 2022. The Company expects a consolidated adjusted effective tax rate range of 10.1% to 11.1% and a Core adjusted effective tax rate range of 9.9% to 10.9%.

The Company expects capital asset expenditures of $100 to $125 million for the full fiscal year 2022, which includes expected initial expenditures related to a new 2 million square foot distribution facility with state-of-the-art automation for the Housewares segment. The Company expects the total cost of the new distribution center and equipment to be in the range of $200 to $225 million spread over fiscal years 2022 and 2023, assuming construction and equipment costs remain at current levels.

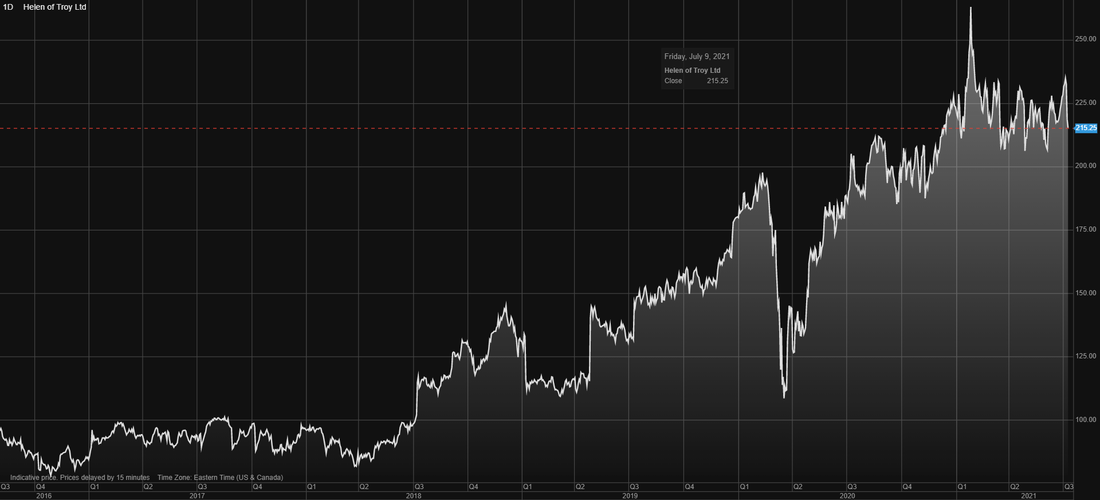

Helen of Troy (HELE) stock price chart over last 5 years

The image below shows the stock price history of Helen of Troy (HELE) over the last 5 years. And it's been a very good time for Helen of Troy's stockholders, with the stock increasing by 125.5% over the last 5 years

The stock of Helen of Troy is trading at a lot closer to its 52 week high than it is to its 52 week low which to us is a clear indication that the short term sentiment and momentum of Helen of Troy's stock is very positive at this point in time.

The stock of Helen of Troy is trading at a lot closer to its 52 week high than it is to its 52 week low which to us is a clear indication that the short term sentiment and momentum of Helen of Troy's stock is very positive at this point in time.

Helen of Troy (HELE) stock price chart over last 5 years

Helen of Troy (HELE) stock vs Lifetime Brands (LCUT) stock over the last 5 years

The image below shows the stock price performance of Helen of Troy (HELE) and Lifetime Brands (LCUT) over the last 5 years. While both owns various consumer brands, their two firms stock price trends and performance over the last 5 years are very different. The summary below shows the stock price performance of the two firms over the last 5 years.

The stock of Helen of Troy has easily outperformed that of Lifetime Brands over the last 5 years

- Helen of Troy (HELE): 125.5%

- Lifetime Brands (LCUT): -0.42%

The stock of Helen of Troy has easily outperformed that of Lifetime Brands over the last 5 years

Helen of Troy (HELE) stock vs Lifetime Brands (LCUT) stock over the last 5 years

Helen of Troy (HELE) latest stock valuation and forecast

So what is Helen of Troy's stock worth based on the release of their latest earnings report? Based on the group's latest earnings and their outlook provided our valuation model provides a target price (forecasted full value price at $201.90 a Helen of Troy stock. We therefore believe that the stock of Helen of Troy is slightly overvalued.

We usually suggest long term fundamental or value investors look to enter into a stock at least 10% below our target (full value) price which in this case is $201.90. Thus we see a good entry point into Helen of Troy's stock at $181.70 or below. We believe that Helen of Troy's stock will pull back slightly in coming weeks and months to levels closer to our target price..

Since the stock of Helen of Troy (HELE) is trading at slightly above our suggested entry point we rate the stock of HELE as a hold

We usually suggest long term fundamental or value investors look to enter into a stock at least 10% below our target (full value) price which in this case is $201.90. Thus we see a good entry point into Helen of Troy's stock at $181.70 or below. We believe that Helen of Troy's stock will pull back slightly in coming weeks and months to levels closer to our target price..

Since the stock of Helen of Troy (HELE) is trading at slightly above our suggested entry point we rate the stock of HELE as a hold

HydroFlask a brand owned by Helen of Troy

Next earnings release of Helen of Troy (HELE)

It is expected that Helen of Troy will release their 2nd quarter 2022 earnings report in early October 2021