|

Related Topics

|

|

Category: Stock Market and Hormel Foods

Date: 25 August 2019 Stock Price: $42 We take a look at the 3rd quarter 2019 financial results of Hormel Foods Corporation, the owner of various branded food products such as Skippy,Spam and Black Label

|

|

About Hormel Foods Corporation

Hormel Foods Corporation, based in Austin, Minn., is a leading global branded food company with over $9 billion in annual revenues across more than 80 countries worldwide. Its brands include Skippy®, SPAM®, Hormel® Natural Choice®, Columbus®, Applegate®, Justin's®, Wholly®, Hormel® Black Label® and more than 30 other beloved brands. The company is a member of the S&P 500 Index and the S&P 500 Dividend Aristocrats. In 2016, the company celebrated its 125th anniversary and announced its new vision for the future – Inspired People. Inspired Food.™ - focusing on its legacy of innovation.

Financial overview

Numbers the group's management highlighted:

Numbers we are interested in: (for the quarter)

- Volume of 1.1 billion lbs., down 4%; organic volume down 1%

- Net sales of $2.3 billion, down 3%

- Organic net sales flat

- Pretax earnings of $261 million, up 1%

- Operating margin of 11.2% compared to 10.9% last year

- Effective tax rate of 23.6% compared to 18.4% last year

- Diluted earnings per share of $0.37, down 5% due to a higher effective tax rate

- Year-to-date cash flow from operations of $573 million, down 23% due to higher working capital

- Fiscal 2019 earnings guidance reaffirmed at $1.71 to $1.85 per share

Numbers we are interested in: (for the quarter)

- Net sales: $2.3 billion (down from $2.36 billion for the same quarter in the previous year)

- Cost of products sold: $1,86 billion (down from $1,9 billion for the same quarter in the previous year)

- Gross profit: $433.4 million (down from $455.1 million for the same quarter in the previous year)

- Net earnings: $199.4 million (down from $210.4 million for the same quarter in the previous year)

- Earnings per share-basic: $ 0.37 (down from $ 0.40 for the same quarter in the previous year)

- Earnings per share- diluted: $0.37 (down from $0.39 for the same quarter in the previous year)

- Diluted number of shares in issue: 543.678 million

- Dividend per share: $0.21 (so far $0.63 for the 3 quarters of the financial year)

- Cash and equivalents: $560.2 million

- Cash and equivalents per share: $1.03 (or 2.45% of the group's share price)

- Accounts receivable $528.6 (down from $600.4 million for the same quarter in the previous year)

- Inventories: $1,11 billion (up from $963.5 million)

- Cash generated from operations: $ 723.6 million (down from $ 751.1 million for the same quarter in the previous year)

- Cash generated from operations per share: $1.33 (or 3.2% of the group's share price)

- PE ratio: 22.7 (based on the earnings guidance provided for the full year)

- Dividend yield: 2%

Hormel Food Corporation management commentary on the results and earnings guidance

"We delivered earnings in line with our expectations this quarter as our experienced management team reacted quickly and appropriately to rapidly changing market conditions," said Jim Snee, chairman of the board, president and chief executive officer. "Disciplined pricing, strategic promotional activity, effective advertising and insight-led innovation all played a positive role in our performance.

The fundamentals of our company are strong, and we remain focused on delivering our key results as we navigate near-term commodity market uncertainty." "Innovative branded product lines such as Hormel® Bacon 1TM cooked bacon, Hormel® Fire BraisedTM products, Skippy® P.B. & Jelly Minis, and Herdez® salsas all delivered strong sales growth," Snee said.

"Our team also grew sales across many core brands such as SPAM® , Dinty Moore® , Mary Kitchen® and Old Smokehouse® ." "Double-digit earnings growth in Refrigerated Foods offset weaker results in Grocery Products," Snee said. "Refrigerated Foods effectively managed sales growth and profitability in the midst of volatile input costs caused by African swine fever. Many of our established brands in Grocery Products continue to outpace center store growth. However, the disappointing bottom-line performance for Grocery Products was driven by higher avocado costs in our MegaMex joint venture and lower results for our Skippy® peanut butter spreads business." "The Jennie-O Turkey Store team is working diligently to regain lean ground turkey distribution following the two voluntary product recalls," Snee said.

"Our International team made progress growing the SPAM® and Skippy® brands in China while U.S. exports continue to be impacted by global trade uncertainty."

Outlook

"We are reaffirming our fiscal 2019 earnings guidance range," Snee said. "While we have yet to see sustained higher pork prices due to African swine fever, we have seen input cost volatility and are expecting further volatility. The Refrigerated Foods team has proven its ability to operate in various market conditions with a continued focus on value-added growth, disciplined pricing and innovation. Earnings pressure from higher avocado prices and peanut butter category dynamics will continue to impact results in Grocery Products in the fourth quarter." "Our experienced management team will continue to leverage our company's long-term strategy of building brands, innovating, making strategic acquisitions and increasing balance in our business to deliver long-term growth," Snee said.

The fundamentals of our company are strong, and we remain focused on delivering our key results as we navigate near-term commodity market uncertainty." "Innovative branded product lines such as Hormel® Bacon 1TM cooked bacon, Hormel® Fire BraisedTM products, Skippy® P.B. & Jelly Minis, and Herdez® salsas all delivered strong sales growth," Snee said.

"Our team also grew sales across many core brands such as SPAM® , Dinty Moore® , Mary Kitchen® and Old Smokehouse® ." "Double-digit earnings growth in Refrigerated Foods offset weaker results in Grocery Products," Snee said. "Refrigerated Foods effectively managed sales growth and profitability in the midst of volatile input costs caused by African swine fever. Many of our established brands in Grocery Products continue to outpace center store growth. However, the disappointing bottom-line performance for Grocery Products was driven by higher avocado costs in our MegaMex joint venture and lower results for our Skippy® peanut butter spreads business." "The Jennie-O Turkey Store team is working diligently to regain lean ground turkey distribution following the two voluntary product recalls," Snee said.

"Our International team made progress growing the SPAM® and Skippy® brands in China while U.S. exports continue to be impacted by global trade uncertainty."

Outlook

"We are reaffirming our fiscal 2019 earnings guidance range," Snee said. "While we have yet to see sustained higher pork prices due to African swine fever, we have seen input cost volatility and are expecting further volatility. The Refrigerated Foods team has proven its ability to operate in various market conditions with a continued focus on value-added growth, disciplined pricing and innovation. Earnings pressure from higher avocado prices and peanut butter category dynamics will continue to impact results in Grocery Products in the fourth quarter." "Our experienced management team will continue to leverage our company's long-term strategy of building brands, innovating, making strategic acquisitions and increasing balance in our business to deliver long-term growth," Snee said.

- Net Sales Guidance (in billions) $9.50 - $10.0

- Earnings Per Share Guidance $1.71 - $1.85

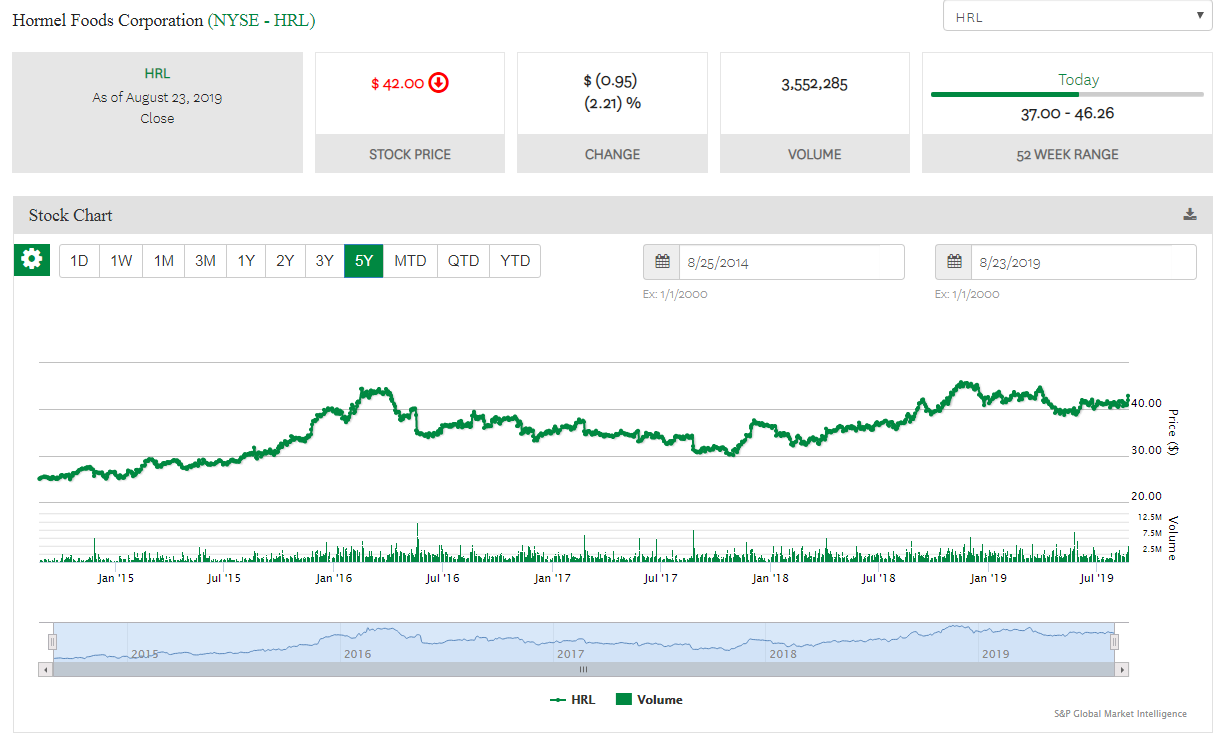

Hormel Food Corporation (NYSE:HRL) stock price history

The image below shows the stock price history of Hormel Foods (NYSE:HRL) for the last 5 years. While the group's share price has provided decent returns for shareholders it has moved sideways in recent times.

Hormel Foods Corporation (NYSE:HRL) stock valuation

So the question is what do we value Hormel shares at based on their latest financial results and their earnings guidance provided? Earnings per share declined by almost 6%. And revenues for the group declined marginally when compared to the same quarter of the previous year. While accounts receivable declined (which is a good thing as less money is owed to the group), their inventories increased steadily from $963 million to around $1.11 billion. Are inventories building up due to the fact that their products are not moving fast enough? It certainly looks like it when one looks at the revenue decline being recorded too.

All things considered we value the group's stock at $38.40 a share. We feel they are overvalued at their current price and we suspect that the group's share price will continue to trade sideways until there is a new catalyst for driving the group's growth in terms of revenue and earnings. For now it seems they as a group are in a consolidation period and it looks like their share price is consolidating around the late $30 to early $40 a share. We don't think investors will benefit from strong capital growth by investing in Hormel Foods Corporation right now.

All things considered we value the group's stock at $38.40 a share. We feel they are overvalued at their current price and we suspect that the group's share price will continue to trade sideways until there is a new catalyst for driving the group's growth in terms of revenue and earnings. For now it seems they as a group are in a consolidation period and it looks like their share price is consolidating around the late $30 to early $40 a share. We don't think investors will benefit from strong capital growth by investing in Hormel Foods Corporation right now.