|

Related Topics

|

|

Category: Molson Coors and Stock Market

Last updated: 1 June 2020 Stock price: $38.09 On this page we will look to provide more details about Molson Coors Beverage Company one of the world's largest brewers with brands such as Blue Moon, Coors Lite and Miller Genuine Draft. The company's net revenues topped $10.5 billion in fiscal 2019

|

|

About Molson Coors Beverage Company

We are one of the world's largest brewers and have a diverse portfolio of owned and partner brands, including global priority brands Blue Moon, Coors Banquet, Coors Light, Miller Genuine Draft, Miller Lite, and Staropramen, regional champion brands Carling, Molson Canadian and other leading country-specific brands, as well as craft and specialty beers such as Creemore Springs, Cobra, Sharp's Doom Bar, Henry's Hard and Leinenkugel's. With centuries of brewing heritage, we craft high-quality, innovative beverages with the purpose of uniting people to celebrate all life’s moments. As a business, our ambition is to be the first choice for our people, our consumers and our customers, and our success depends on our ability to make our products available to meet a wide range of consumer segments and occasions.

Molson and Coors were founded in 1786 and 1873, respectively. Our commitment to producing the highest quality beers is a key part of our heritage and remains so to this day. Our brands are designed to appeal to a wide range of consumer tastes, styles and price preferences. Our largest markets are the U.S., Canada and Europe. Coors was incorporated in June 1913 under the laws of the state of Colorado. In October 2003, Coors merged with and into Adolph Coors Company, a Delaware corporation. In February 2005, Adolph Coors Company merged with Molson Inc. ("the Merger").

Upon completion of the Merger, Adolph Coors Company changed its name to Molson Coors Brewing Company. In January 2020, we changed our name from Molson Coors Brewing Company to Molson Coors Beverage Company, as further discussed below

Molson and Coors were founded in 1786 and 1873, respectively. Our commitment to producing the highest quality beers is a key part of our heritage and remains so to this day. Our brands are designed to appeal to a wide range of consumer tastes, styles and price preferences. Our largest markets are the U.S., Canada and Europe. Coors was incorporated in June 1913 under the laws of the state of Colorado. In October 2003, Coors merged with and into Adolph Coors Company, a Delaware corporation. In February 2005, Adolph Coors Company merged with Molson Inc. ("the Merger").

Upon completion of the Merger, Adolph Coors Company changed its name to Molson Coors Brewing Company. In January 2020, we changed our name from Molson Coors Brewing Company to Molson Coors Beverage Company, as further discussed below

Molson Coors Brands

Quick facts about Molson Coors

- Molson Coors is listed on the New York Stock Exchange under share code ticker: TAP

- Market Capital of Molson Coors: $8.26 billion as at 1 June 2020

- Owns Coors Lite

- Owns Blue Moon

- Owns Miller Genuine Draft

- Number of employees of Molson Coors as at end of 2019: 17 700

- Net sales in fiscal 2019: $10.59 billion

- Earnings per share for fiscal 2019: $1.11

- Shares in issue: 216.9 million

- Cash on their balance sheet: $523.4 million

- Stockholders equity in Molson Coors: $13.673 billion

Brands of Molson Coors

We have a diverse portfolio of owned and partner brands which are positioned to meet a wide range of consumer segments and occasions in a variety of markets, including Blue Moon, Coors Banquet, Coors Light, Miller Genuine Draft, Miller Lite and Staropramen. We consider these our global priority brands which we continue to invest in and focus on growing globally. We believe our portfolio encompasses all segments of the beer industry with the purpose of uniting people to celebrate all life’s moments, including premium and premium lights, economy, above premium and craft, as well as adjacencies such as ciders and other malt beverages. Additionally, as we continue to evolve our strategy and portfolio to appeal to the ever-changing preferences of our consumer base, we are also broadening our range of products and offerings within our portfolio to include other beverage categories outside of traditional beer, including our emerging plans in the non-alcoholic beverage segment. The following includes our primary brands sold in each of our segments.

Competition of Molson Coors

We evaluate ourselves in relation to other global brewers using various metrics, including overall market capitalization, volume, net sales revenue, gross margins and net profits, as well as our position within each of our core markets, with the goal to be the first choice for our consumers and customers. To provide a perspective of the relative size of the major participants in the global brewing market, the market capitalizations of our primary global competitors, based on foreign exchange rates as of December 31, 2019, were as follows (in $ billions)

Our portfolio of beers competes with numerous above premium, premium, and economy brands. These competing brands are produced by international, national, regional and local brewers. We compete most directly with ABI brands, but also compete with imported and craft beer brands, as well as flavored malt beverages

- Anheuser-Busch InBev SA/NV ("ABI"): $164.6

- Heineken N.V. ("Heineken"): $61.3

- Carlsberg Group ("Carlsberg"): $22.6

- Asahi Group Holdings, Ltd. ("Asahi"): $22.2

- Molson Coors Brewing Company (MCBC) :$11.8

Our portfolio of beers competes with numerous above premium, premium, and economy brands. These competing brands are produced by international, national, regional and local brewers. We compete most directly with ABI brands, but also compete with imported and craft beer brands, as well as flavored malt beverages

Truly Hard Seltzer, Angry Orchard Hard Cider, Wild Leaf Craft Hard Tear and Twisted Tea Hard Ice Tea

Distribution channels of Molson Coors

In the United States, beer is generally distributed through a three-tier system consisting of manufacturers, distributors and retailers. A national network of approximately 380 independent distributors and one owned distributor, Coors Distributing Company, purchases our products and distributes them to on- and off-premise retail accounts. References to on- and off-premise sales volumes are the sales to retailers of these distributors, which we believe is a useful data point relative to consumer trends

In Canada, provincial governments regulate the beer industry, particularly with regard to the pricing, mark-up, container management, sale, distribution and advertising of beer. Distribution and the retail sale of alcohol products involve a wide range and varied degree of Canadian government control through their respective provincial liquor boards.

In Europe, the on-premise channel includes sales to pubs and restaurants. The installation and maintenance of draught beer dispensing equipment in the on-premise channel is generally the responsibility of the brewer. Accordingly, we own refrigeration units and other equipment used to dispense beer from kegs to consumers that are used in on-premise outlets. This includes beer lines, cooling equipment, taps, and counter mounts. The off-premise channel includes sales to supermarkets, convenience stores, liquor stores, distributors, and wholesalers. Over the last few years, the off-premise channel has become increasingly concentrated among a small number of super-store chains. Generally, over the years, industry volumes in Europe have shifted from the higher margin on-premise channel, where products are consumed in pubs and restaurants, to the lower margin off-premise channel, also referred to as the "take-home" market. In 2019, approximately 40% of sales were on-premise and 60% were off-premise. Consistent with prior years, the on-premise channel has continued to experience declines from shifting consumer preference to off-premise partially due to smoking bans in many countries.

As of the end of 2019, we employed approximately 17,700 employees within our business globally. Specifically, we employed approximately 7,300 within our U.S. segment, 6,600 within our Europe segment, 2,600 within our Canada segment, 400 within our International segment, 200 within our Corporate headquarters in Colorado and 600 within our Global Business Services center. Under our recently announced revitalization plan the company is consolidating business units and offices to streamline the organization and find savings that will be reinvested back into the business. After taking into account all changes in each of the business units, including Europe, the plan is expected to reduce employment levels, in aggregate, by approximately 500 to 600 employees globally. The company expects the costs associated with the restructuring to be substantially recognized by the end of fiscal year 2021.

In Canada, provincial governments regulate the beer industry, particularly with regard to the pricing, mark-up, container management, sale, distribution and advertising of beer. Distribution and the retail sale of alcohol products involve a wide range and varied degree of Canadian government control through their respective provincial liquor boards.

In Europe, the on-premise channel includes sales to pubs and restaurants. The installation and maintenance of draught beer dispensing equipment in the on-premise channel is generally the responsibility of the brewer. Accordingly, we own refrigeration units and other equipment used to dispense beer from kegs to consumers that are used in on-premise outlets. This includes beer lines, cooling equipment, taps, and counter mounts. The off-premise channel includes sales to supermarkets, convenience stores, liquor stores, distributors, and wholesalers. Over the last few years, the off-premise channel has become increasingly concentrated among a small number of super-store chains. Generally, over the years, industry volumes in Europe have shifted from the higher margin on-premise channel, where products are consumed in pubs and restaurants, to the lower margin off-premise channel, also referred to as the "take-home" market. In 2019, approximately 40% of sales were on-premise and 60% were off-premise. Consistent with prior years, the on-premise channel has continued to experience declines from shifting consumer preference to off-premise partially due to smoking bans in many countries.

As of the end of 2019, we employed approximately 17,700 employees within our business globally. Specifically, we employed approximately 7,300 within our U.S. segment, 6,600 within our Europe segment, 2,600 within our Canada segment, 400 within our International segment, 200 within our Corporate headquarters in Colorado and 600 within our Global Business Services center. Under our recently announced revitalization plan the company is consolidating business units and offices to streamline the organization and find savings that will be reinvested back into the business. After taking into account all changes in each of the business units, including Europe, the plan is expected to reduce employment levels, in aggregate, by approximately 500 to 600 employees globally. The company expects the costs associated with the restructuring to be substantially recognized by the end of fiscal year 2021.

Coors Light, Miller Genuine Draft and Blue Moon

Trademarks of Molson Coors

We own trademarks on the majority of the brands we produce and have licenses for the remainder. We also hold several patent and design registrations with expiration dates through 2038 relating to brewing methods, beer dispensing systems, packaging and certain other innovations. We are not reliant on patent royalties for our financial success. Therefore, these expirations are not expected to have a significant impact on our business.

Employees of Molson Coors

As of the end of 2019, we employed approximately 17,700 employees within our business globally. Specifically, we employed approximately 7,300 within our U.S. segment, 6,600 within our Europe segment, 2,600 within our Canada segment, 400 within our International segment, 200 within our Corporate headquarters in Colorado and 600 within our Global Business Services center. Under our recently announced revitalization plan the company is consolidating business units and offices to streamline the organization and find savings that will be reinvested back into the business. After taking into account all changes in each of the business units, including Europe, the plan is expected to reduce employment levels, in aggregate, by approximately 500 to 600 employees globally. The company expects the costs associated with the restructuring to be substantially recognized by the end of fiscal year 2021.

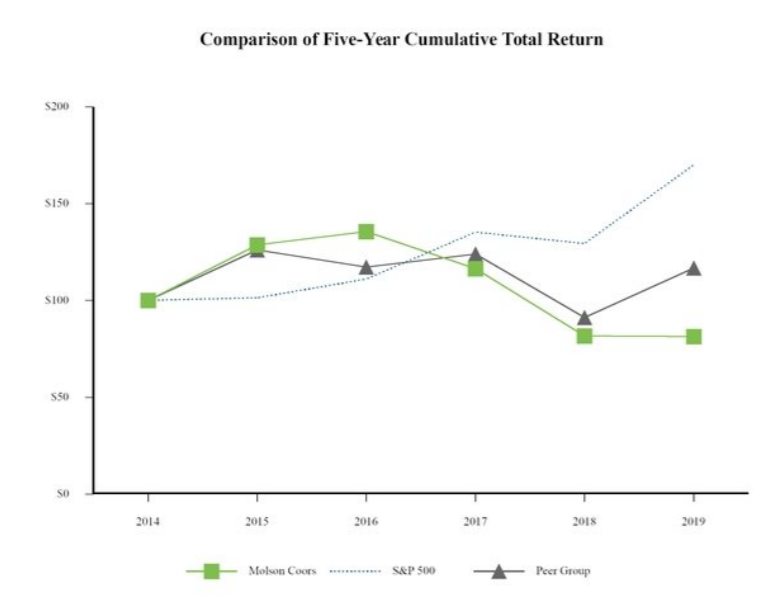

Molson Coors (NYSE:TAP) stock performance

The following graph compares our cumulative total stockholder return over the last five fiscal years with the S&P 500 and a customized peer index including MCBC, ABI, Carlsberg, Heineken and Asahi (the "Peer Group"). We have used a weighted average based on market capitalization to determine the return for the Peer Group. The graph assumes $100 was invested on December 31, 2014, in our Class B common stock, the S&P 500 and the Peer Group, and assumes reinvestment of all dividends. The below is provided for informational purposes and is not indicative of future performance

Molson Coors vs S&P 500 vs Peer Group

Over the 5 year period Molson Coors provided an average annual loss of -4% while the S&P 500 returned 11.2%. So the S&P 500 has comfortably outperformed the stock of Molson Coors. Even the peers of Molson Coors easily outperformed them.

Our latest Molson Coors stock valuation (12 February 2020)

So what do we value Molson Coors stock at after the release of their 4th quarter 2019 earnings report? Based on Molson Coors' 4th quarter 2019 earnings report our valuation models provides a target price (full value price) for Molson Coors at $64.30 a stock. We therefore believe that the stock of Molson Coors is close to fully valued.

We usually suggest that long term and fundamental investors get in at least 10% below our target (full value) price which in this case is $64.30 therefore we believe a good entry point into Molson Coors stock is at $57.80 or below. We expect the stock of Molson Coors to slowly make its way up to our target price (full value price) in coming weeks and months as we believe is slightly undervalued and that their cost savings program will filter through to higher earnings and better valuations in coming reporting quarters.

We usually suggest that long term and fundamental investors get in at least 10% below our target (full value) price which in this case is $64.30 therefore we believe a good entry point into Molson Coors stock is at $57.80 or below. We expect the stock of Molson Coors to slowly make its way up to our target price (full value price) in coming weeks and months as we believe is slightly undervalued and that their cost savings program will filter through to higher earnings and better valuations in coming reporting quarters.