|

Related Topics

|

|

Category: Stock Market and Navistar

Date: 5 September 2019 Stock Price: $24.78 We take a look at the 3rd quarter earnings for their 2019 fiscal year of Navistar, the engine, truck, bus and defence vehicle builder

|

|

About Navistar

Navistar is a leading manufacturer of commercial trucks, buses, defense vehicles and engines. Wherever ingenuity drives global markets, you'll find us taking the lead. Since 1831, our history has been interwoven with some of the most defining moments in world history. Whether it was America's westward expansion or WWII, we were there, pushing the limits of what's possible and driving history forward. But that doesn't mean we're stuck in the past. We're determined to keep delivering smart, sustainable technologies - because we believe that innovation defines America's future, too. We manufacture trucks, buses, defence vehicles and engines

Financial overview of Navistar's latest earnings report

Numbers we are interested in for the quarter:

- Sales and revenue: $3.042 billion (up from $2.6 billion for the same quarter of the previous year)

- Cost and expenses: $2.852 billion (up from $2.426 billion for the same quarter of the previous year)

- Net income: $156 million (down from $170 million for the same quarter of the previous year)

- Diluted earnings per share: $1.56 (down from $1.71 for the same quarter of the previous year)

- Diluted number of shares in issue: 99.7 million (unchanged from the 99.7 million for the same quarter of the previous year)

- Cash and cash equivalents: $1.16 billion

- Cash and cash equivalents per share: $11.64

- Cash and cash equivalents makes up 46.9% of Navistar's current market capital

- Cash and cash equivalents makes up 15.9% of Navistar's total assets

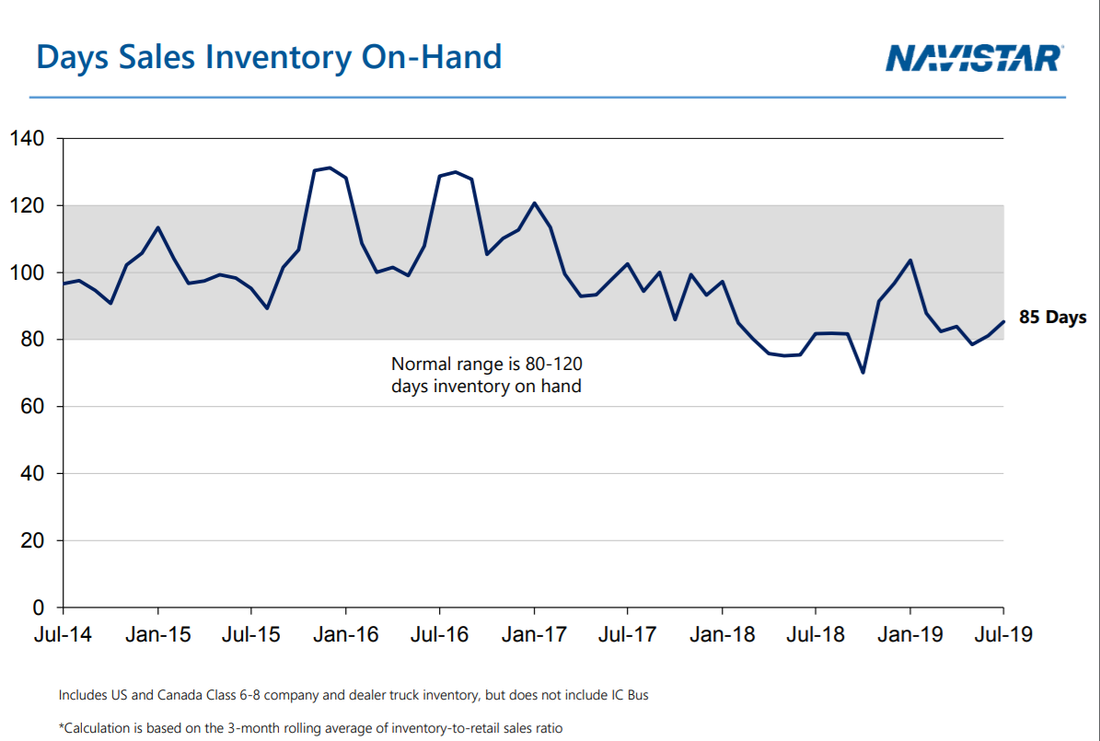

- Inventories: $1.195 billion

- Inventories on hand is currently sitting at 85 days worth of sales for Navistar. Well within their range of 80-120 days worth of days sales held in inventories (The image below shows the number of days sales is held in inventories for Navistar)

- Inventories makes up 16.38% of the group's total assets

- Finance receivables: $2.187 billion

- Finance receivables makes up 29.98% of the group's total assets. We get worried when receivables makes up more than 20% of the group's assets. We are therefore concerned about money owed to the group and if some of this will be impaired. If impairments take place it will have an impact on their future earnings

- Cash generated from operations: $135 million

- Cash generated from operations per share: $1.35

Navistar's management commentary on the results and earnings guidance

LISLE, Ill. — September 4, 2019 — Navistar International Corporation (NYSE: NAV) today announced third quarter 2019 net income of $156 million, or $1.56 per diluted share, compared to third quarter 2018 net income of $170 million, or $1.71 per diluted share. Third quarter 2019 adjusted EBITDA was $266 million, compared to $218 million in the same period one year ago. Adjusted net income in the quarter grew 55 percent to $147 million, compared to $95 million last year.

Revenues in the quarter were $3 billion, up 17 percent from the same period one year ago, primarily due to a 28 percent increase in volumes in the company’s Core market (Class 6-8 trucks and buses in the United States and Canada). “This was another great quarter for Navistar,” said Troy A. Clarke, Navistar chairman, president and chief executive officer.

“Market share increased, revenues and earnings grew at double-digit rates, and we made significant investments in our operations and our Uptime promise.” Navistar ended third quarter 2019 with $1.16 billion in consolidated cash, cash equivalents and marketable securities. Manufacturing cash, cash equivalents and marketable securities were $1.11 billion at the end of the quarter. The company generated $250 million of manufacturing free cash flow during the quarter largely due to strong adjusted EBITDA and net working capital performance.

The company had a number of uptime-related highlights during its third quarter. Navistar's warranty performance and service partnership agreement with Love's and Speedco, initially announced in March, is now fully operational, activating the commercial vehicle industry's largest service network in North America. Additionally, the company’s latest parts distribution center (PDC) opened late last month near Memphis to help cater to the growing demand for parts and quicker maintenance turnaround times. Complementing the new PDC are new enhancements to Navistar’s retail inventory management system, resulting in 50 percent lower emergency parts orders, further maximizing Uptime for the company’s customers.

Also during the quarter, the company announced it would be making capital investments of approximately $125 million in new and expanded manufacturing facilities at its Huntsville, Ala. plant to produce next-generation big-bore powertrains developed with its global alliance partner TRATON.

Industry and financial guidance

The company updated the following 2019 full-year industry and financial guidance:

• Industry retail deliveries of Class 6-8 trucks and buses in the United States and Canada are forecast to be 435,000 to 455,000 units, with Class 8 retail deliveries of 295,000 to 315,000 units.

• Gross margin is expected to be in the range of 17.75% and 18%.

• Core market share is forecast to be between 18.5% and 19%.

The company reaffirmed the following 2019 full-year financial guidance:

• Navistar revenues are expected to be between $11.25 billion and $11.75 billion.

• The company’s adjusted EBITDA is expected to be between $875 million and $925 million.

Additionally, the company forecasts the industry’s 2020 retail deliveries of Class 6-8 trucks and buses in the United States and Canada to be in the range of 335,000 to 365,000 units, with Class 8 retail deliveries between 210,000 and 240,000 units. “We are on course for a strong end to 2019, and we’re not standing still,” Clarke said. “The company is recapturing market share and is growing revenue, EBITDA and cash flow. We remain focused on setting ourselves up for long-term success.”

Revenues in the quarter were $3 billion, up 17 percent from the same period one year ago, primarily due to a 28 percent increase in volumes in the company’s Core market (Class 6-8 trucks and buses in the United States and Canada). “This was another great quarter for Navistar,” said Troy A. Clarke, Navistar chairman, president and chief executive officer.

“Market share increased, revenues and earnings grew at double-digit rates, and we made significant investments in our operations and our Uptime promise.” Navistar ended third quarter 2019 with $1.16 billion in consolidated cash, cash equivalents and marketable securities. Manufacturing cash, cash equivalents and marketable securities were $1.11 billion at the end of the quarter. The company generated $250 million of manufacturing free cash flow during the quarter largely due to strong adjusted EBITDA and net working capital performance.

The company had a number of uptime-related highlights during its third quarter. Navistar's warranty performance and service partnership agreement with Love's and Speedco, initially announced in March, is now fully operational, activating the commercial vehicle industry's largest service network in North America. Additionally, the company’s latest parts distribution center (PDC) opened late last month near Memphis to help cater to the growing demand for parts and quicker maintenance turnaround times. Complementing the new PDC are new enhancements to Navistar’s retail inventory management system, resulting in 50 percent lower emergency parts orders, further maximizing Uptime for the company’s customers.

Also during the quarter, the company announced it would be making capital investments of approximately $125 million in new and expanded manufacturing facilities at its Huntsville, Ala. plant to produce next-generation big-bore powertrains developed with its global alliance partner TRATON.

Industry and financial guidance

The company updated the following 2019 full-year industry and financial guidance:

• Industry retail deliveries of Class 6-8 trucks and buses in the United States and Canada are forecast to be 435,000 to 455,000 units, with Class 8 retail deliveries of 295,000 to 315,000 units.

• Gross margin is expected to be in the range of 17.75% and 18%.

• Core market share is forecast to be between 18.5% and 19%.

The company reaffirmed the following 2019 full-year financial guidance:

• Navistar revenues are expected to be between $11.25 billion and $11.75 billion.

• The company’s adjusted EBITDA is expected to be between $875 million and $925 million.

Additionally, the company forecasts the industry’s 2020 retail deliveries of Class 6-8 trucks and buses in the United States and Canada to be in the range of 335,000 to 365,000 units, with Class 8 retail deliveries between 210,000 and 240,000 units. “We are on course for a strong end to 2019, and we’re not standing still,” Clarke said. “The company is recapturing market share and is growing revenue, EBITDA and cash flow. We remain focused on setting ourselves up for long-term success.”

Navistar (NYSE: NAV) stock price history

The image below, obtained from Google shows the stock price history of Navistar for the last 5 years. And its not been a very profitable time for Navistar stockholders. With the stock having traded at just under $40 a stock to the current $24.78. And the fact that Navistar's stock price is trading at close to its 52 week low and is far away from its 52 week high shows that the short term sentiment towards Navistar stock is still predominantly negative.

Navistar (NYSE: NAV) latest stock valuation

So based on Navistar's latest earnings report and their guidance what do we value their stock at? Our valuation models have a target price (full value price) on Navistart of $32.40. So based on our valuation models we believe that Navistar (NYSE:NAV) is undervalued and we expect the stock price to trend upwards to levels closer to our target price in coming weeks and months. The current price point offers fundamental long term investors a solid entry point from a value point of view. Especially considering the strong amount of cash the group has on its balance sheet. All they need to look out for is their high receivables levels and their debt levels. We would want to see the group paying off their long term debt a little faster.