|

Related Topics

|

|

Category: Stock Market and PVH

Date: 8 September 2019 Stock Price: $85.39 We take a look at the 2nd quarter earnings release of their 2019 fiscal year of clothing brands owner PVH, whose brands include Calvin Klein and Speedo

|

|

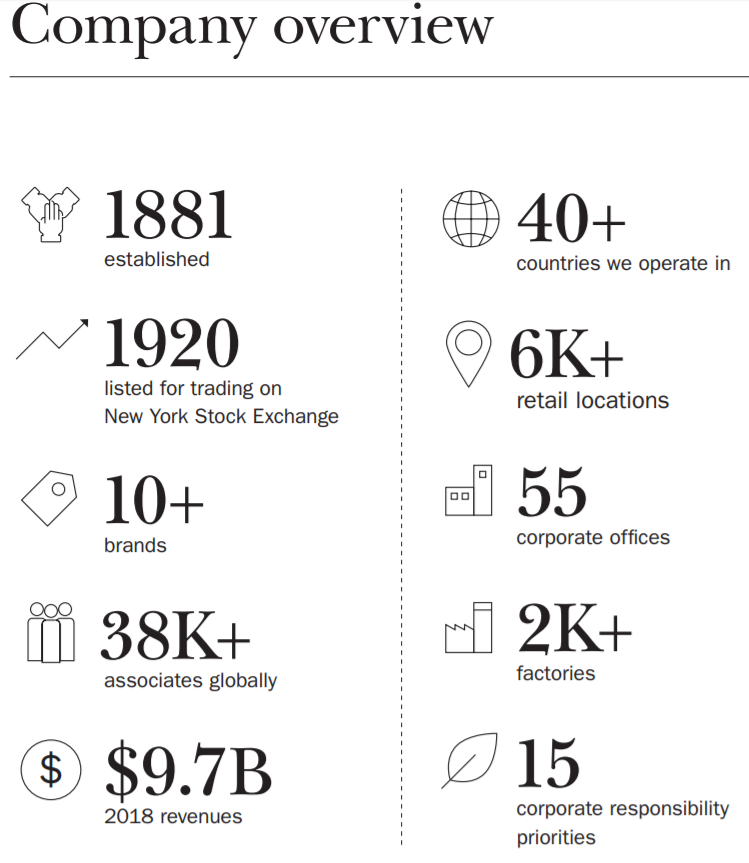

About PVH

Our brand portfolio includes the iconic CALVIN KLEIN, TOMMY HILFIGER, Van Heusen, IZOD, ARROW, Speedo*, Warner’s, Olga and Geoffrey Beene brands, as well as the digital-centric True & Co. intimates brand. We market a variety of goods under these and other nationally and internationally known owned and licensed brands. PVH has over 38,000 associates operating in over 40 countries and $9.7 billion in annual revenues. That’s the Power of Us. That’s the Power of PVH.

The image below shows some of the business highlights of PVH.

The image below shows some of the business highlights of PVH.

Financial overview of PVH's latest earnings report

The numbers we are interested in (for the quarter):

- Total Revenue: $2.364 billion (up from $2.223 billion from the same quarter of the previous year)

- Total Operating Expenses : $1.154 billion (up from $1.071 million for the same quarter of the previous year)

- Net income: $193.1 million (up from from $165.2 billion for the same quarter of the previous year)

- Diluted earnings per share: $2.58 (up from $2.12 for the same quarter of the previous year)

- Diluted weighted-average shares outstanding: 74.8 million (up from 77 million for the same quarter of the previous year)

- PE ratio: 32 (based on the earnings per share for the current quarter being reported for full fiscal year)

- Cash and cash equivalents: $433.5 million

- Cash and cash equivalents per share: $5.79

- Cash and cash equivalents makes up 6.7% of PVH's current market capital

- Cash and cash equivalents makes up 3.13% of PVH's total assets

- Inventories: $1.862 billion (up from $1.731 billion for the same quarter of the previous year)

- Inventories makes up 13.47% of PVH's total assets

- Inventories increased by 7.57% over the last year

- Total shareholders' equity of PVH.: $5.871 billion

- Shareholders' equity per share: $78.4

- Accounts receivable: $808.9 million (up from $731.6 million for the same quarter of the previous year)

- Accounts receivable makes up 5.85% of PVH's total assets

- Accounts receivable grew by 10.44% over the last year

PVH's management commentary on the results and earnings guidance

Commenting on these results, Emanuel Chirico, Chairman and Chief Executive Officer, noted, “We are pleased to report our second quarter results, which saw continued outperformance by our European businesses. However, our businesses in North America and across China experienced weak traffic trends, including the impact of protests in Hong Kong, resulting in a more promotional environment. Although we are pleased with our second quarter and first half results, we have taken a conservative approach to our second half outlook. As such, we lowered our annual revenue and EPS outlook based on our current trends and our expectation that the volatility in the macro environment, the global retail landscape and the continuing escalation of the trade tensions between the U.S. and China will cause our business to remain under pressure, as will the ongoing impact of protests in Hong Kong.

We have great confidence in our diversified business model and the underlying power of CALVIN KLEIN and TOMMY HILFIGER, and believe we are positioning our businesses to succeed in the ever-changing consumer landscape. As we execute on our strategic priorities, our ongoing data and digital transformation, together with delivering the best product and consumer experience, should allow us to capture the heart of the consumer. We believe that with our two greatest assets, our people and our brands, we will unlock the long term brand growth opportunities we see and deliver sustainable long term returns for our stockholders.”

2019 Outlook:

The Company’s revised 2019 guidance is based on the assumption that current trends in the business continue for the remainder of the year. Specifically, the reductions in revenue and margins reflect the trade tensions between the U.S. and China, the ongoing protests in Hong Kong and the increasingly promotional U.S. retail environment.

The 2019 guidance incorporates the impact on certain of the Company’s products of tariffs imposed and expected to be imposed by the U.S. on goods imported from China into the U.S., including (i) $250 billion of total goods imported from China into the U.S. (Tranches 1, 2 and 3) currently at 25%, with an expected increase to 30% in October 2019, and (ii) $300 billion of total goods imported from China into the U.S. (Tranche 4) at 15% expected to be imposed in September 2019 and December 2019. These tariffs are expected to have a negative impact of approximately $0.20 per share in 2019. The Company’s 2019 guidance also reflects the Australia acquisition and the TH CSAP acquisition that closed in the second quarter of 2019, and the impact of the CK Collection closure and the G-III license. These transactions are expected to result in a net addition to revenue of approximately $75 million in 2019.

Full Year Guidance

The Company currently projects that 2019 earnings per share on a GAAP basis will be in a range of $7.95 to $8.05 compared to $9.65 in 2018. The Company currently projects that 2019 earnings per share on a non-GAAP basis will be in a range of $9.30 to $9.40 compared to $9.60 in 2018. Both the GAAP and non-GAAP projections include the estimated negative impact of approximately $0.35 per share related to foreign currency translation.

Revenue in 2019 is projected to increase approximately 1% (increase approximately 3% on a constant currency basis) as compared to 2018. Revenue for the Tommy Hilfiger business is projected to increase approximately 5% (increase approximately 8% on a constant currency basis). Revenue for the Calvin Klein business is projected to decrease approximately 2% (flat on a constant currency basis). Revenue for the Heritage Brands business is projected to decrease approximately 1%.

Net interest expense in 2019 is projected to decrease to approximately $110 million compared to $116 million in 2018. The Company estimates that the 2019 effective tax rate will be in a range of 11.5% to 12.5% on a GAAP basis and in a range of 14% to 15% on a non-GAAP basis.

The Company’s estimate of 2019 earnings per share on a non-GAAP basis excludes approximately $138 million of pre-tax net costs, consisting of (i) $105 million of pre-tax costs expected to be incurred in connection with the Calvin Klein restructuring, consisting of a noncash lease asset impairment resulting from the closure of the Company’s flagship store on Madison Avenue in New York, New York, severance, contract termination and other costs, other noncash asset impairments, and inventory markdowns, (ii) $60 million of pre-tax costs incurred in connection with the Socks and hosiery transaction, (iii) $55 million of pre-tax costs incurred in connection with the closure of the Company’s TOMMY HILFIGER flagship and anchor stores in the United States (the “TH U.S. store closures”), primarily consisting of noncash lease asset impairments, (iv) $6 million of pre-tax costs incurred in connection with 11 the refinancing of the Company’s senior credit facilities, (v) a pre-tax gain of $113 million recorded to write up the Company's equity investments in Gazal and PVH Australia to fair value in connection with the Australia acquisition and (vi) $25 million of pre-tax costs expected to be incurred in connection with the Australia and TH CSAP acquisitions, primarily consisting of noncash valuation adjustments, and the resulting estimated tax effects of these pre-tax items.

Third Quarter Guidance

The Company currently projects that third quarter 2019 earnings per share on a GAAP basis will be in a range of $2.70 to $2.75 compared to $3.15 in the prior year period. The Company currently projects that third quarter 2019 earnings per share on a non-GAAP basis will be in a range of $2.95 to $3.00 compared to $3.21 in the prior year period. Both the GAAP and nonGAAP projections include an estimated negative impact of approximately $0.09 per share related to foreign currency translation. Revenue in the third quarter of 2019 is projected to increase approximately 1% (increase approximately 3% on a constant currency basis) compared to the prior year period. Revenue for the Tommy Hilfiger business in the third quarter is projected to increase approximately 5% (increase approximately 8% on a constant currency basis).

Revenue for the Calvin Klein business in the third quarter is projected to be flat (increase approximately 2% on a constant currency basis). Revenue for the Heritage Brands business in the third quarter is projected to decrease approximately 10%. Net interest expense in the third quarter of 2019 is projected to decrease to approximately $27 million compared to $29 million in the prior year period. The Company estimates that the third quarter 2019 effective tax rate will be in a range of 8% to 9% on a GAAP basis and in a range of 6.5% to 7.5% on a non-GAAP basis. The Company’s estimate of third quarter 2019 earnings per share on a non-GAAP basis excludes approximately $16 million of pre-tax costs, consisting of (i) $12 million of pre-tax costs expected to be incurred in connection with the Australia and TH CSAP acquisitions, and (ii) $4 million of pre-tax costs expected to be incurred in connection with the Calvin Klein restructuring, and the resulting estimated tax effects of these pre-tax costs.

We have great confidence in our diversified business model and the underlying power of CALVIN KLEIN and TOMMY HILFIGER, and believe we are positioning our businesses to succeed in the ever-changing consumer landscape. As we execute on our strategic priorities, our ongoing data and digital transformation, together with delivering the best product and consumer experience, should allow us to capture the heart of the consumer. We believe that with our two greatest assets, our people and our brands, we will unlock the long term brand growth opportunities we see and deliver sustainable long term returns for our stockholders.”

2019 Outlook:

The Company’s revised 2019 guidance is based on the assumption that current trends in the business continue for the remainder of the year. Specifically, the reductions in revenue and margins reflect the trade tensions between the U.S. and China, the ongoing protests in Hong Kong and the increasingly promotional U.S. retail environment.

The 2019 guidance incorporates the impact on certain of the Company’s products of tariffs imposed and expected to be imposed by the U.S. on goods imported from China into the U.S., including (i) $250 billion of total goods imported from China into the U.S. (Tranches 1, 2 and 3) currently at 25%, with an expected increase to 30% in October 2019, and (ii) $300 billion of total goods imported from China into the U.S. (Tranche 4) at 15% expected to be imposed in September 2019 and December 2019. These tariffs are expected to have a negative impact of approximately $0.20 per share in 2019. The Company’s 2019 guidance also reflects the Australia acquisition and the TH CSAP acquisition that closed in the second quarter of 2019, and the impact of the CK Collection closure and the G-III license. These transactions are expected to result in a net addition to revenue of approximately $75 million in 2019.

Full Year Guidance

The Company currently projects that 2019 earnings per share on a GAAP basis will be in a range of $7.95 to $8.05 compared to $9.65 in 2018. The Company currently projects that 2019 earnings per share on a non-GAAP basis will be in a range of $9.30 to $9.40 compared to $9.60 in 2018. Both the GAAP and non-GAAP projections include the estimated negative impact of approximately $0.35 per share related to foreign currency translation.

Revenue in 2019 is projected to increase approximately 1% (increase approximately 3% on a constant currency basis) as compared to 2018. Revenue for the Tommy Hilfiger business is projected to increase approximately 5% (increase approximately 8% on a constant currency basis). Revenue for the Calvin Klein business is projected to decrease approximately 2% (flat on a constant currency basis). Revenue for the Heritage Brands business is projected to decrease approximately 1%.

Net interest expense in 2019 is projected to decrease to approximately $110 million compared to $116 million in 2018. The Company estimates that the 2019 effective tax rate will be in a range of 11.5% to 12.5% on a GAAP basis and in a range of 14% to 15% on a non-GAAP basis.

The Company’s estimate of 2019 earnings per share on a non-GAAP basis excludes approximately $138 million of pre-tax net costs, consisting of (i) $105 million of pre-tax costs expected to be incurred in connection with the Calvin Klein restructuring, consisting of a noncash lease asset impairment resulting from the closure of the Company’s flagship store on Madison Avenue in New York, New York, severance, contract termination and other costs, other noncash asset impairments, and inventory markdowns, (ii) $60 million of pre-tax costs incurred in connection with the Socks and hosiery transaction, (iii) $55 million of pre-tax costs incurred in connection with the closure of the Company’s TOMMY HILFIGER flagship and anchor stores in the United States (the “TH U.S. store closures”), primarily consisting of noncash lease asset impairments, (iv) $6 million of pre-tax costs incurred in connection with 11 the refinancing of the Company’s senior credit facilities, (v) a pre-tax gain of $113 million recorded to write up the Company's equity investments in Gazal and PVH Australia to fair value in connection with the Australia acquisition and (vi) $25 million of pre-tax costs expected to be incurred in connection with the Australia and TH CSAP acquisitions, primarily consisting of noncash valuation adjustments, and the resulting estimated tax effects of these pre-tax items.

Third Quarter Guidance

The Company currently projects that third quarter 2019 earnings per share on a GAAP basis will be in a range of $2.70 to $2.75 compared to $3.15 in the prior year period. The Company currently projects that third quarter 2019 earnings per share on a non-GAAP basis will be in a range of $2.95 to $3.00 compared to $3.21 in the prior year period. Both the GAAP and nonGAAP projections include an estimated negative impact of approximately $0.09 per share related to foreign currency translation. Revenue in the third quarter of 2019 is projected to increase approximately 1% (increase approximately 3% on a constant currency basis) compared to the prior year period. Revenue for the Tommy Hilfiger business in the third quarter is projected to increase approximately 5% (increase approximately 8% on a constant currency basis).

Revenue for the Calvin Klein business in the third quarter is projected to be flat (increase approximately 2% on a constant currency basis). Revenue for the Heritage Brands business in the third quarter is projected to decrease approximately 10%. Net interest expense in the third quarter of 2019 is projected to decrease to approximately $27 million compared to $29 million in the prior year period. The Company estimates that the third quarter 2019 effective tax rate will be in a range of 8% to 9% on a GAAP basis and in a range of 6.5% to 7.5% on a non-GAAP basis. The Company’s estimate of third quarter 2019 earnings per share on a non-GAAP basis excludes approximately $16 million of pre-tax costs, consisting of (i) $12 million of pre-tax costs expected to be incurred in connection with the Australia and TH CSAP acquisitions, and (ii) $4 million of pre-tax costs expected to be incurred in connection with the Calvin Klein restructuring, and the resulting estimated tax effects of these pre-tax costs.

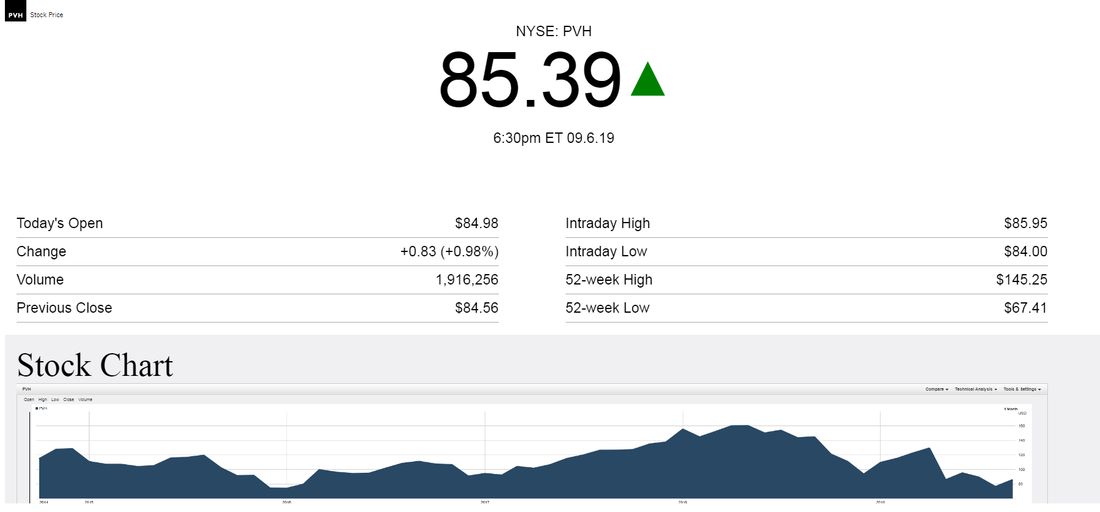

PVH (NYSE: PVH) stock price history

The image below shows the stock price history of PVH for the last 5 years. And its not been a good time for PVH investors over this period. 5 years ago the stock was trading around $127 and its currently trading at $85.39 . Thats a stock price decline of -32.7% over the last 5 years. The group is also trading at a lot closer to its 52 week low of $67.41 than what it is trading to its 52 week high of $145.25, which shows that the shorter term sentiment towards PVH is largely negative.

Recent coverage of PVH

The extract below obtained from Zacks shows some of the recent stock coverage of PVH after their earnings release

PVH Corp. (PVH - Free Report) was a big mover last session, as the company saw its shares rise more than 6% on the day. The move came on solid volume with far more shares changing hands than in a normal session. This reverses the recent trend for the company—as the stock is now down 14.7% in the past one-month time frame.

The move came after the company reported better-than-expected second-quarter fiscal 2019 (ended Aug 04, 2019) results.

The company has seen three negative estimate revisions in the past few weeks, while its Zacks Consensus Estimate for the current quarter has also moved lower over the past few weeks, suggesting there may be trouble down the road. So, make sure to keep an eye on this stock going forward, to see if this recent move higher can last.

The original article can be found here

PVH Corp. (PVH - Free Report) was a big mover last session, as the company saw its shares rise more than 6% on the day. The move came on solid volume with far more shares changing hands than in a normal session. This reverses the recent trend for the company—as the stock is now down 14.7% in the past one-month time frame.

The move came after the company reported better-than-expected second-quarter fiscal 2019 (ended Aug 04, 2019) results.

The company has seen three negative estimate revisions in the past few weeks, while its Zacks Consensus Estimate for the current quarter has also moved lower over the past few weeks, suggesting there may be trouble down the road. So, make sure to keep an eye on this stock going forward, to see if this recent move higher can last.

The original article can be found here

PVH (NYSE: PVH) latest stock valuation

So based on the latest earnings report from PVH and the fiscal guidance provided what do we value PVH stock at? Based on the earnings reported and the fiscal guidance provided our valuation models provides a stock price target (full value price) of $138.10 per PVH share. We therefore believe the stock of PVH is undervalued and offers long term fundamental or value investors a great entry point into the stock. We predict that the stock will move upwards in coming weeks and months to a level closer to our target price for PVH of $138.10.