|

Related Topics

|

|

Category: Stock Market and Stanley Black & Decker

Date: 25 October 2019 Stock Price: $146.43 We take a look at the 3rd quarter earnings release of their 2019 fiscal year of Stanley Black & Decker a supplier of hand tools, power tools and other related accessories.

|

|

About Stanley Black & Decker

In 1843, Frederick Stanley started a small shop in New Britain, Connecticut, to manufacture bolts, hinges and other hardware of high quality from wrought iron. In 1910, Duncan Black and Alonzo Decker started their shop in Baltimore, Maryland, and six years later obtained the world’s first patent for a portable power tool. Over the years the two companies amassed an unparalleled family of iconic brands and trusted products. In 2010, they came together as Stanley Black & Decker, a leading global diversified industrial. Known for superior quality, continual innovation and rigorous operational discipline, we remain driven by a passion for excellence and a commitment to serve the builders, makers and protectors of the world.

Stanley Black & Decker, an S&P 500 company, is a diversified global provider of hand tools, power tools and related accessories, electronic security solutions, healthcare solutions, engineered fastening systems, and more

Stanley Black & Decker, an S&P 500 company, is a diversified global provider of hand tools, power tools and related accessories, electronic security solutions, healthcare solutions, engineered fastening systems, and more

Overview of Stanley Black & Decker's 3rd quarter 2019 earnings report

The numbers we are interested in (for the quarter):

- Net sales: $3.633 billion (up from $3.494 billion from the same quarter of the previous year)

- Net sales increased by 3.9% over the last 12 months

- Cost of sales: $2.393 billion (up from $2.256 billion for the same quarter of the previous year)

- Operating expenses increased by 6.07% over the last 12 months

- Net income: $230.5 million (down from $247.8 billion for the same quarter of the previous year)

- Diluted earnings per share: $1.53 (down from $1.65 for the same quarter of the previous year)

- PE ratio of Stanley Black & Decker: 23.9

- Dividend declared: $0.69

- Dividend yield: 1.89%

- Dividend yield: 1.89%

- Diluted weighted-average shares outstanding: 150.623 million (up from 150.599 million for the same quarter of the previous year)

- Cash and cash equivalents: $311.7 million

- Cash and cash equivalents per share: $1.46

- Cash and cash equivalents makes up 0.99% of Stanley Black & Decker's market capital

- Cash and cash equivalents makes up 1.46% of Stanley Black & Decker's total assets

- Inventories: $2.743 billion

- Inventories makes up 18.21% of Stanley Black & Decker's total assets

- Stanley Black & Decker's inventories grew by 15.58% over the last 12 months

- Accounts receivable: $1.902 billion

- Accounts receivable makes up 8.9% of Stanley Black & Decker's total assets

- Stockholders equity of Stanley Black & Decker: $8.262 billion

- Stockholders equity per share: $54.85

- Stanley Black & Decker is trading at 2.66 times its stockholders equity which is well outside the expected range of between 2 and 4 which most companies tend to trade at.

- Cash generated from operations: $192.7 million

- Cash generated from operations per share: $1.28

Stanley Black & Deckers management commentary on their 3rd quarter results and outlook

New Britain, Connecticut, October 24, 2019 … Stanley Black & Decker (NYSE: SWK) today announced third quarter 2019 financial results.

Stanley Black & Decker’s President and CEO, James M. Loree, commented, “In the third quarter, we successfully delivered above-market organic growth and adjusted earnings per share expansion versus prior year, overcoming $90 million in external pre-tax margin headwinds and challenges in certain end markets.

“To position the business for success in 2020 and beyond, we have begun implementing new cost and pricing actions, as well as accelerating our $300 – $500 million multi-year margin resiliency initiative. These actions will preserve our ability to continue to generate continued earnings growth and manage externally driven volatility. “Over the past three years we have produced strong organic growth and consistent adjusted EPS expansion, while absorbing approximately $900 million in pretax externally generated cost pressures (~6% of sales). We have also executed on multiple revenue growth catalysts, including Craftsman, revenue synergies, emerging markets, e-commerce and breakthrough innovations, that are generating success in the market and position us for continued share gains. It is a testament to our seasoned and capable management team and our SFS 2.0 operating system that we are successfully navigating this environment and continuing to achieve our vision: to become known as one of the world’s great innovators, deliver top-quartile financial performance, and elevate our commitment to corporate social responsibility.”

Donald Allan Jr., Executive Vice President and CFO, commented, “Security generated modest organic growth in the quarter, resulting from targeted commercial investments as part of the ongoing business transformation. Within electronic security, the order rates and backlog are in strong positions and our cost efficiency initiatives continue to generate value. We are encouraged by this momentum and believe the business is positioned to generate positive organic growth and margin expansion in the fourth quarter and beyond.”

2019 Outlook & Cost Reduction Program

Management is revising its 2019 EPS outlook to $6.50 - $6.60 from $7.50 - $7.70 on a GAAP basis primarily due to restructuring charges associated with the cost reduction program announced today, in addition to the factors below. The Company is reducing its adjusted EPS range to $8.35 - $8.45 from $8.50 - $8.70 and reiterating its free cash flow conversion estimate of approximately 85% - 90%. The cost reduction program is currently being implemented and is expected to deliver $200 million in annual cost savings with an approximate pre-tax restructuring charge of $150 million expected to be recognized primarily in 2019.

The following reflects the key assumption changes to the Company's prior full year adjusted EPS outlook:

• An incremental $55 million in tariff and currency related cost pressure

• A modestly reduced expectation for organic growth reflecting a slower growth environment for industrial and emerging markets (3.5% - 4% versus prior assumption of 4%)

• Partially offsetting these impacts are incremental benefits from the margin resiliency initiatives, incremental cost actions and a lower tax rate (~16.5%)

Allan continued, “Our 2019 guidance now incorporates $445 million of externally generated input cost headwinds while continuing to reflect our delivery of abovemarket organic growth of 3.5% - 4% and low-single digit adjusted earnings per share growth. This will be a strong end to the year, especially given the magnitude and timing of the input cost moves, as well as the current market demand environment.

“As we shift to 2020, we believe we are taking the appropriate actions to protect our margins and our competitiveness while once again positioning the business for EPS expansion. We will continue to execute our playbook to take price, optimize our global supply chain and adjust our cost structure through the actions announced today and generate significant value with our margin resiliency program. 5 “The organization remains focused on strong day-to-day execution and operational excellence and we believe the Company is well-positioned to deliver sustained above-market organic growth with operating leverage, strong free cash flow conversion and top-quartile shareholder returns over the long-term.”

The difference between 2019 GAAP and Adjusted EPS guidance is $1.85, consisting of acquisition-related and other charges. These forecasted charges primarily relate to restructuring, deal and integration costs, Security business transformation and margin resiliency initiatives, and inventory step-up amortization.

Stanley Black & Decker’s President and CEO, James M. Loree, commented, “In the third quarter, we successfully delivered above-market organic growth and adjusted earnings per share expansion versus prior year, overcoming $90 million in external pre-tax margin headwinds and challenges in certain end markets.

“To position the business for success in 2020 and beyond, we have begun implementing new cost and pricing actions, as well as accelerating our $300 – $500 million multi-year margin resiliency initiative. These actions will preserve our ability to continue to generate continued earnings growth and manage externally driven volatility. “Over the past three years we have produced strong organic growth and consistent adjusted EPS expansion, while absorbing approximately $900 million in pretax externally generated cost pressures (~6% of sales). We have also executed on multiple revenue growth catalysts, including Craftsman, revenue synergies, emerging markets, e-commerce and breakthrough innovations, that are generating success in the market and position us for continued share gains. It is a testament to our seasoned and capable management team and our SFS 2.0 operating system that we are successfully navigating this environment and continuing to achieve our vision: to become known as one of the world’s great innovators, deliver top-quartile financial performance, and elevate our commitment to corporate social responsibility.”

Donald Allan Jr., Executive Vice President and CFO, commented, “Security generated modest organic growth in the quarter, resulting from targeted commercial investments as part of the ongoing business transformation. Within electronic security, the order rates and backlog are in strong positions and our cost efficiency initiatives continue to generate value. We are encouraged by this momentum and believe the business is positioned to generate positive organic growth and margin expansion in the fourth quarter and beyond.”

2019 Outlook & Cost Reduction Program

Management is revising its 2019 EPS outlook to $6.50 - $6.60 from $7.50 - $7.70 on a GAAP basis primarily due to restructuring charges associated with the cost reduction program announced today, in addition to the factors below. The Company is reducing its adjusted EPS range to $8.35 - $8.45 from $8.50 - $8.70 and reiterating its free cash flow conversion estimate of approximately 85% - 90%. The cost reduction program is currently being implemented and is expected to deliver $200 million in annual cost savings with an approximate pre-tax restructuring charge of $150 million expected to be recognized primarily in 2019.

The following reflects the key assumption changes to the Company's prior full year adjusted EPS outlook:

• An incremental $55 million in tariff and currency related cost pressure

• A modestly reduced expectation for organic growth reflecting a slower growth environment for industrial and emerging markets (3.5% - 4% versus prior assumption of 4%)

• Partially offsetting these impacts are incremental benefits from the margin resiliency initiatives, incremental cost actions and a lower tax rate (~16.5%)

Allan continued, “Our 2019 guidance now incorporates $445 million of externally generated input cost headwinds while continuing to reflect our delivery of abovemarket organic growth of 3.5% - 4% and low-single digit adjusted earnings per share growth. This will be a strong end to the year, especially given the magnitude and timing of the input cost moves, as well as the current market demand environment.

“As we shift to 2020, we believe we are taking the appropriate actions to protect our margins and our competitiveness while once again positioning the business for EPS expansion. We will continue to execute our playbook to take price, optimize our global supply chain and adjust our cost structure through the actions announced today and generate significant value with our margin resiliency program. 5 “The organization remains focused on strong day-to-day execution and operational excellence and we believe the Company is well-positioned to deliver sustained above-market organic growth with operating leverage, strong free cash flow conversion and top-quartile shareholder returns over the long-term.”

The difference between 2019 GAAP and Adjusted EPS guidance is $1.85, consisting of acquisition-related and other charges. These forecasted charges primarily relate to restructuring, deal and integration costs, Security business transformation and margin resiliency initiatives, and inventory step-up amortization.

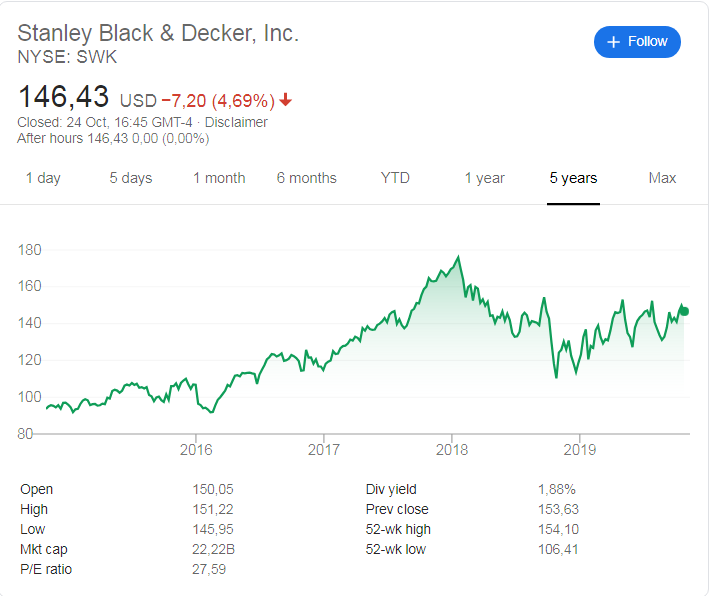

Stanley Black & Decker (NYSE: SWK) stock price history

The image below, obtained from Google, shows the stock price history of Stanley Black & Decker (NYSE: SWK) over the last 5 years. And it's been a amazing time for Stanley Black & Decker. 5 years ago the stock was trading at around $93.70 and its currently trading at $146.43. That's a decent return of 56.3% over the last 5 years. The stock of Stanley Black & Decker is trading at closer to its 52 week high of $154.10 than it is to its 52 week low of $106.41 which to us its an indication that the short term sentiment and momentum of Stanley Black & Decker is positive.

Stanley Black & Decker (NYSE: SWK) stock price history over the last 5 years.

Recent coverage of Stanley Black & Decker

The extract below shows recent coverage of Amazon as obtained from TheStreet.com

Shares of Stanley Black & Decker (SWK - Get Report) took a hit Thursday after the company cut its outlook and reported a drop in third-quarter profit. The stock fell 4% to $147.72 after the company said its net income fell to $230.5 million, or $1.53 a share, from $247.8 million, or $1.65 a share. Adjusted earnings were $2.13 a share. Sales rose 4% to $3.6 billion.

Analysts were expecting earnings of $2.03 a share on sales of $3.65 billion, according to FactSet. The company also announced a new cost-reduction program that it expects will result in annual savings of $200 million, with pretax restructuring charge of $150 million expected to be recognized primarily in 2019. Its adjusted earnings guidance for the year was reduced to a range of $8.35 to $8.45 a share from $8.50 to $8.70. Analysts were expecting adjusted full-year EPS of $8.56.

Read the full article here

Shares of Stanley Black & Decker (SWK - Get Report) took a hit Thursday after the company cut its outlook and reported a drop in third-quarter profit. The stock fell 4% to $147.72 after the company said its net income fell to $230.5 million, or $1.53 a share, from $247.8 million, or $1.65 a share. Adjusted earnings were $2.13 a share. Sales rose 4% to $3.6 billion.

Analysts were expecting earnings of $2.03 a share on sales of $3.65 billion, according to FactSet. The company also announced a new cost-reduction program that it expects will result in annual savings of $200 million, with pretax restructuring charge of $150 million expected to be recognized primarily in 2019. Its adjusted earnings guidance for the year was reduced to a range of $8.35 to $8.45 a share from $8.50 to $8.70. Analysts were expecting adjusted full-year EPS of $8.56.

Read the full article here

DeWalt hand power tool

Stanley Black & Decker (NYSE: SWK) latest stock valuation

So based on the earnings report of Stanley Black & Decker (NYSE: SWK) what do we value Stanley Black & Decker stock at? Based on their latest earnings report and the updated guidance provided our valuation models provide a target (full value) price for Stanley Black & Decker stock at $127.40 a stock. We therefore believe the stock of Stanley Black & Decker is overvalued.

We usually recommend that long term fundamental or value investors buy into a stock at least 10% below our target (full value) price, which in this case is $127.40. We therefore believe a good entry point into Stanley Black & Decker is $114.70 or below. We expect the stock of Stanley Black & Decker to pull back from current levels to levels closer to our target (full value) price in coming weeks and months.

We usually recommend that long term fundamental or value investors buy into a stock at least 10% below our target (full value) price, which in this case is $127.40. We therefore believe a good entry point into Stanley Black & Decker is $114.70 or below. We expect the stock of Stanley Black & Decker to pull back from current levels to levels closer to our target (full value) price in coming weeks and months.