|

Related Topics

|

|

Category: Stock Market and Walmart

Date: 18 November 2019 Stock Price: $120.36 We take a look at the latest financial results of retail group, Walmart for their 3rd quarter 2020 financial year. It is commonly known as the worlds largest retailer.

|

|

About Walmart

What started small, with a single discount store and the simple idea of selling more for less, has grown over the last 50 years into the largest retailer in the world. Each week, nearly 265 million customers and members visit our more than 11,200 stores under 55 banners in 27 countries and eCommerce websites in 10 countries. With fiscal year 2018 revenue of $500.3 billion, Walmart employs over 2.2 million associates worldwide. Walmart continues to be a leader in sustainability, corporate philanthropy and employment opportunity. It’s all part of our unwavering commitment to creating opportunities and bringing value to customers and communities around the world.

From our humble beginnings as a small discount retailer in Rogers, Ark., Walmart has opened thousands of stores in the U.S. and expanded internationally. Through innovation, we're creating a seamless experience to let customers shop anytime and anywhere online, through mobile devices and in stores. We are creating opportunities and bringing value to customers and communities around the globe. Walmart operates over 11,200 stores under 55 banners in 27 countries and eCommerce websites in 10 countries. We employ approximately 2.2 million associates around the world — 1.5 million in the U.S. alone.

Around the world, we help families save money so they can live better. We use our size and scale to provide access to high-quality goods and fresh, nutritious food at everyday low prices—while creating opportunities for our associates and small and medium-sized global suppliers. Led by President & CEO Judith McKenna, Walmart International has more than 5,900 retail units, operating outside the United States with 55 banners in 26 countries with more than 700,000 associates serving more than 100 million customers every week.

From our humble beginnings as a small discount retailer in Rogers, Ark., Walmart has opened thousands of stores in the U.S. and expanded internationally. Through innovation, we're creating a seamless experience to let customers shop anytime and anywhere online, through mobile devices and in stores. We are creating opportunities and bringing value to customers and communities around the globe. Walmart operates over 11,200 stores under 55 banners in 27 countries and eCommerce websites in 10 countries. We employ approximately 2.2 million associates around the world — 1.5 million in the U.S. alone.

Around the world, we help families save money so they can live better. We use our size and scale to provide access to high-quality goods and fresh, nutritious food at everyday low prices—while creating opportunities for our associates and small and medium-sized global suppliers. Led by President & CEO Judith McKenna, Walmart International has more than 5,900 retail units, operating outside the United States with 55 banners in 26 countries with more than 700,000 associates serving more than 100 million customers every week.

Walmart store entrance

Financial overview of Walmart's latest results

The data below refers to the latest quarter unless specified otherwise

- Revenue: $127.991 billion (up from $124.894 billion for the same quarter of the previous year)

- Revenue increased by 2.5% over the last 12 months

- Cost of sales: $95.900 billion (up from $93.116 billion for the same quarter of the previous year)

- Cost of sales increased by 3% over the last 12 months.

- Operating income: $4.78 billion (down from $4.986 billion for the same quarter of the previous year)

- Diluted income: $3.288 billion (up from $1.710 billion for the same quarter of the previous year)

- Diluted income per share: $1.15 (up from $0.58 for the same quarter of the previous year)

- Diluted weighted number of shares outstanding: 2.861 billion (down from 2.941 billion for the same quarter of the previous year)

- Cash and cash equivalents: $8.606 billion

- Cash and cash equivalents per share: $3

- Cash and cash equivalents makes up 2.5% of Walmart's market capital

- Cash and cash equivalents makes up 3.6% of Walmart's total assets

- Receivables, net: $5.612 billion

- Receivables makes up 2.33% of Walmart's total assets

- Inventories: $51.546 billion

- Inventories makes up 21.4% of Walmart's total assets

- Cash generated from operations (for the 3 quarters of their fiscal 2019): $14.539 billion

- Cash generated from operations per share (for the 3 quarters of their fiscal 2019): $5.08

Walmart (NYSE:WMT) management commentary on the results and earnings guidance

Doug McMillon: President & CEO, Walmart Inc

We continue to see good traffic in our stores. We’re growing market share in key food and consumables categories, including fresh, and we had positive comps in general merchandise. Comp sales growth of 3.2 percent, along with good expense management, helped us leverage SG&A, particularly in physical stores, even as we made investments in price. This led to growth in operating income for the sixth consecutive quarter. On a two-year stack, comp sales of 6.6 percent are among the best we’ve seen in a number of years. In eCommerce, our topline performance was strong with growth of 41 percent. Gross margins improved versus last year through improvements in merchandising mix, we leveraged operating expenses, lowered variable costs per unit, and the CVI – our Customer Value Index – score is ahead of where we planned it for the full year. We’re making progress on many fronts, but we need to do more and move faster, especially with our assortment including marketplace. I continue to challenge the team to drive a deeper, more sustainable relationship with the customer, better execute the fundamentals, and improve the overall economics of the business. Our strength is being driven by food, which is good, but we need even more progress on Walmart.com with general merchandise.

We’re mixing the business out better to achieve better margin rates, but there is more work to do. We’re committed to progress and building a larger, healthier eCommerce business. Our customers want that, our marketplace sellers want that, and so do we. Grocery pickup and delivery, along with new offerings like Unlimited Delivery and InHome Delivery, will help us unlock advantages we have to serve customers in a way that reduces friction and enhances convenience. We need to translate this repetitive food and consumable volume into a stronger Walmart.com business that’s profitable over time, so that’s what we’re working on. Near the end of the quarter, we kicked off the holidays in the U.S. with an integrated plan in stores and online. On Walmart.com, customers could find great prices on top items, including electronics, gaming, toys and home. In stores, we’ve expanded ‘Check Out with Me’ and the ‘DotCom 5 Store’ to all supercenters. Customers who want to avoid long checkout lines at the front or ask an associate to help them find a missing store item online will love the convenience we’re offering.

We continue to see good traffic in our stores. We’re growing market share in key food and consumables categories, including fresh, and we had positive comps in general merchandise. Comp sales growth of 3.2 percent, along with good expense management, helped us leverage SG&A, particularly in physical stores, even as we made investments in price. This led to growth in operating income for the sixth consecutive quarter. On a two-year stack, comp sales of 6.6 percent are among the best we’ve seen in a number of years. In eCommerce, our topline performance was strong with growth of 41 percent. Gross margins improved versus last year through improvements in merchandising mix, we leveraged operating expenses, lowered variable costs per unit, and the CVI – our Customer Value Index – score is ahead of where we planned it for the full year. We’re making progress on many fronts, but we need to do more and move faster, especially with our assortment including marketplace. I continue to challenge the team to drive a deeper, more sustainable relationship with the customer, better execute the fundamentals, and improve the overall economics of the business. Our strength is being driven by food, which is good, but we need even more progress on Walmart.com with general merchandise.

We’re mixing the business out better to achieve better margin rates, but there is more work to do. We’re committed to progress and building a larger, healthier eCommerce business. Our customers want that, our marketplace sellers want that, and so do we. Grocery pickup and delivery, along with new offerings like Unlimited Delivery and InHome Delivery, will help us unlock advantages we have to serve customers in a way that reduces friction and enhances convenience. We need to translate this repetitive food and consumable volume into a stronger Walmart.com business that’s profitable over time, so that’s what we’re working on. Near the end of the quarter, we kicked off the holidays in the U.S. with an integrated plan in stores and online. On Walmart.com, customers could find great prices on top items, including electronics, gaming, toys and home. In stores, we’ve expanded ‘Check Out with Me’ and the ‘DotCom 5 Store’ to all supercenters. Customers who want to avoid long checkout lines at the front or ask an associate to help them find a missing store item online will love the convenience we’re offering.

Guidance

The following guidance reflects the company’s expectations for fiscal year 2020. Assumptions in the guidance include that economic conditions, currency rates and the tax and regulatory landscape remain generally consistent. The company continues to assess the ongoing civil unrest in Chile and has not included any related potential discrete financial effects in its assumptions. Additionally, the guidance assumes no further change in fair value of the Company's equity investment in JD.com.

• FY20 Adjusted EPS is now expected to increase slightly compared to FY19 adjusted EPS , including Flipkart, and is expected to increase by a high single-digit percentage range, excluding Flipkart.

•Expectations for the dilution from Flipkart remain unchanged, excluding a non-cash impairment charge.

• The effective tax rate is now expected to range between 25% and 25.5%.

The following guidance reflects the company’s expectations for fiscal year 2020. Assumptions in the guidance include that economic conditions, currency rates and the tax and regulatory landscape remain generally consistent. The company continues to assess the ongoing civil unrest in Chile and has not included any related potential discrete financial effects in its assumptions. Additionally, the guidance assumes no further change in fair value of the Company's equity investment in JD.com.

• FY20 Adjusted EPS is now expected to increase slightly compared to FY19 adjusted EPS , including Flipkart, and is expected to increase by a high single-digit percentage range, excluding Flipkart.

•Expectations for the dilution from Flipkart remain unchanged, excluding a non-cash impairment charge.

• The effective tax rate is now expected to range between 25% and 25.5%.

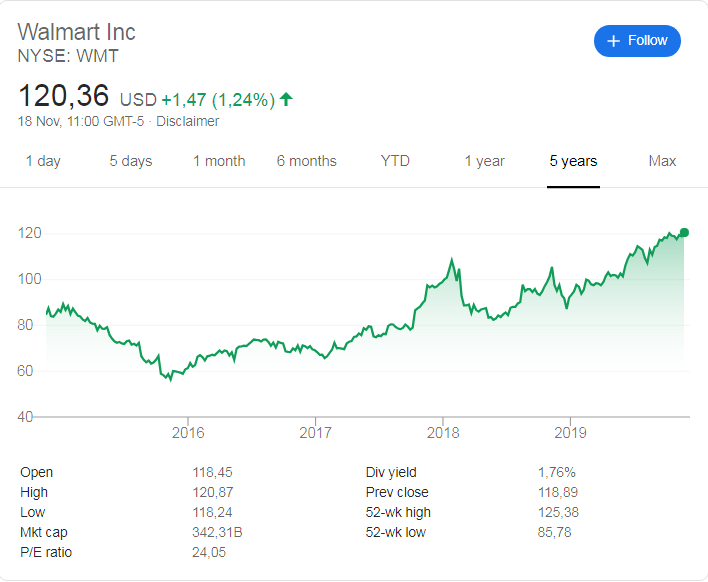

Walmart (NYSE:WMT) stock price history

The image below obtained from Google, shows the stock price history of Walmart (NYSE:WMT) for the last 5 years.Its been a pretty solid run for Walmart shares over the last 5 years. 5 years ago the stock of Walmart was trading at $84.70 and its currently trading at $120.36 a stock. That's a healthy 42.1% return provided to Walmart stockholders over the last 5 years.

Walmart's stock is trading at a lot closer to its 52 week high of $125.38 than it is to its 52 week low of $85.78 which to us is a clear indication that the short term sentiment and momentum of Walmart's stock is overwhelmingly positivel

Walmart's stock is trading at a lot closer to its 52 week high of $125.38 than it is to its 52 week low of $85.78 which to us is a clear indication that the short term sentiment and momentum of Walmart's stock is overwhelmingly positivel

Walmart (NYSE: WMT) stock price history over the last 5 years

Recent coverage of Walmart

The extract below covers the latest regarding Walmart as obtained from TheStreet.com

U.S. retail sales rose just 0.3% last month, but missed economists' forecasts when automobile sales were stripped out and declines in clothing, furniture, electronics, and building materials were computed. Previous readings for August and September were revised to the downside, which, when set against flat wage growth and looming tariffs on the next round of China-made consumer goods set to kick-in on December 15, could bode poorly for the coming Christmas period. "The 'control' measure (of U.S. retail sales data) which drives the non-durable goods component of overall consumers' spending, is on course to rise at an annualized rate of less than 3% in the fourth quarter, following a solid 6.3% increase in the third," said Ian Shepherdson of Pantheon Macroeconomics.

"This does not guarantee a sluggish performance from aggregate real consumption, because it tells us nothing about spending on discretionary services or vehicles," he added. "The latter was stronger than we expected in October, but the big picture is unfavorable as financing conditions tighten." That said, both Walmart (WMT - Get Report) , the world's biggest retailer, and J.C. Penney (JCP - Get Report) , the struggling mall-focused retailer, posted stronger-than-expected third quarter earnings last week, taking shares in both groups notably higher as investors bet that, once again, U.S. consumer spending strength would continue to drive broader economic growth. But U.S. households are staggering under a record $14 trillion in debts, when mortgages, credit cards and students loan commitments are factored in, and rising market interest rates are adding to the costs of keeping those obligations current. The broader domestic job market might be hitting a wall, as well, as tariff uncertainty clips hiring plans and manufacturing firms postpone investments amid the steepest month-on-month decline in domestic industrial output in more than a decade.

Read the full article here

U.S. retail sales rose just 0.3% last month, but missed economists' forecasts when automobile sales were stripped out and declines in clothing, furniture, electronics, and building materials were computed. Previous readings for August and September were revised to the downside, which, when set against flat wage growth and looming tariffs on the next round of China-made consumer goods set to kick-in on December 15, could bode poorly for the coming Christmas period. "The 'control' measure (of U.S. retail sales data) which drives the non-durable goods component of overall consumers' spending, is on course to rise at an annualized rate of less than 3% in the fourth quarter, following a solid 6.3% increase in the third," said Ian Shepherdson of Pantheon Macroeconomics.

"This does not guarantee a sluggish performance from aggregate real consumption, because it tells us nothing about spending on discretionary services or vehicles," he added. "The latter was stronger than we expected in October, but the big picture is unfavorable as financing conditions tighten." That said, both Walmart (WMT - Get Report) , the world's biggest retailer, and J.C. Penney (JCP - Get Report) , the struggling mall-focused retailer, posted stronger-than-expected third quarter earnings last week, taking shares in both groups notably higher as investors bet that, once again, U.S. consumer spending strength would continue to drive broader economic growth. But U.S. households are staggering under a record $14 trillion in debts, when mortgages, credit cards and students loan commitments are factored in, and rising market interest rates are adding to the costs of keeping those obligations current. The broader domestic job market might be hitting a wall, as well, as tariff uncertainty clips hiring plans and manufacturing firms postpone investments amid the steepest month-on-month decline in domestic industrial output in more than a decade.

Read the full article here

Walmart store entrance

Walmart (NYSE:WMT) stock valuation

So what do we believe Walmart stock is worth after their latest earnings report and their fiscal guidance provided? Based on their 3rd quarter 2019 earnings report and their earnings guidance our valuation model provides a target (full value) price for Walmart stock at $106.60 a stock (up slightly from our 2nd quarter 2019 earnings report valuation of Walmart).

We therefore believe the stock of Walmart is overvalued at its current price. We usually recommend that long term fundamental or value investors look to enter a stock at least 10% below our target (full value) price which in this case is $106.60. A good entry point into Walmart would therefore be at $95.90 or below. We expect the stock of Walmart to pull back from its current levels to levels closer to our target (full value) price in coming weeks and months.

We therefore believe the stock of Walmart is overvalued at its current price. We usually recommend that long term fundamental or value investors look to enter a stock at least 10% below our target (full value) price which in this case is $106.60. A good entry point into Walmart would therefore be at $95.90 or below. We expect the stock of Walmart to pull back from its current levels to levels closer to our target (full value) price in coming weeks and months.

Next earnings release of Walmart

It is expected that Walmart will release their 4th quarter and full fiscal 2020 earnings in middle February 2020