|

Related Topics

|

|

Category: Stock Market and Yum Brands

Date: 31 October 2019 Stock Price: $101.34 We take a look at the 3rd quarter earnings report of their 2019 fiscal year of Yum! Brands, the owner of KFC, Pizza Hut and Taco Bell. But it seems their investment in GrubHub is hurting Yum brands.

|

|

About Yum Brands

Yum! Brands, Inc., based in Louisville, Kentucky, has over 48,000 restaurants in more than 145 countries and territories primarily operating the company’s brands -- KFC, Pizza Hut and Taco Bell -- global leaders of the chicken, pizza and Mexican-style food categories. Worldwide, the Yum! Brands system opens over eight new restaurants per day on average, making it a leader in global retail development. In 2018, Yum! Brands was named to the Dow Jones Sustainability North America Index and ranked among the top 100 Best Corporate Citizens by Corporate Responsibility Magazine. In 2019, Yum! Brands was named to the Bloomberg Gender-Equality Index for the second consecutive year.

Financial overview of Yum Brands's 3rd quarter 2019 earnings report

The numbers we are interested in (for the quarter):

We get concerned when we see a company's revenues decreasing and costs increasing as this leads to margin pressure which affects the overall profitability of a company as money coming in is decreasing while money leaving in expenses is increasing. While this is expected to happen every now and again, if this occurs regularly one has the question the continued profitability of a company.

Contribution of Yum! Brands different brands to total revenue for the 3rd quarter of 2019:

- Total revenues: $1.339 billion (down $1.399 billion for the same quarter of the previous year)

- Total revenues decreased by -4% over the last 12 months

- Total costs and expenses, net: $859 million (up from $838 million for the same quarter of the previous year)

- Total costs and expenses increased by 3% over the last 12 months

- Net Income: $255 million (down from $454 million for the same quarter of the previous year)

- Diluted earnings per share: $ 0.81 (down 42% from $1.40 for the same quarter of the previous year)

- PE ratio of Yum Brands: 30.1

- Average number of shares outstanding: 313 million (down 4% from 324 million for the same quarter of the previous year)

- Dividends declared per common share: $ 0.42 (up from 16.67% from $0.36 for the same quarter of the previous year)

- Dividend yield of Yum Brands: 1.63%

- Cash and cash equivalents: $691 million

- Cash and cash equivalents per share: $2.20 per share

- Cash and cash equivalents makes up 0.7% of Yum Brands' total market capital

- Accounts and notes receivable: $527 million

- Accounts and notes receivable makes up 10.5% of the Yum Brands' total assets

- Cash generated from operations (for 9 months): $883 million

- Cash generated from operations per share (for 9 months): $2.82

We get concerned when we see a company's revenues decreasing and costs increasing as this leads to margin pressure which affects the overall profitability of a company as money coming in is decreasing while money leaving in expenses is increasing. While this is expected to happen every now and again, if this occurs regularly one has the question the continued profitability of a company.

Contribution of Yum! Brands different brands to total revenue for the 3rd quarter of 2019:

- KFC: $609 million (45.4% of Yum! brands total revenue)

- Pizza Hut: $241 million (18.1% of Yum! brands total revenue)

- Taco Bell: $489 million (36.5% of Yum! brands total revenue)

YUM's management commentary on the results and earnings guidance

Louisville, KY (October 30, 2019) - Yum! Brands, Inc. (NYSE: YUM) today reported results for the third-quarter ended September 30, 2019. Worldwide system sales excluding foreign currency translation grew 8%, with 7% net-new units and 3% same-store sales growth. Third-quarter GAAP EPS was $0.81, a decrease of (42)%. Third-quarter EPS excluding Special Items was $0.80, a decrease of (23)%.

Greg Creed, CEO, said “Following a very strong first half of 2019 and in line with our expectations, third-quarter results were consistent with our long-term growth model. We delivered system sales growth of 8%, with same-store sales of 3% and net-new unit growth of 7%, led by continued strong performances at KFC International and Taco Bell. We’re rapidly approaching the end of a truly historic year. 2019 will not only mark the completion of our 3-year transformation of Yum!, but it will also mark the end of my tenure as Yum! CEO. I couldn’t be prouder of the progress that our teams around the world have made to become more focused, more franchised and more efficient; all while accelerating global growth. Today Yum! has a unique and powerful business model backed by a culture that is stronger than ever and by talent that is truly world class. I’m confident that as I retire, David Gibbs is the right leader to leverage our scale and key growth drivers to enhance franchisee economics, champion the customer experience and drive global growth to maximize value for our stakeholders.”

Third quarter highlights

Worldwide system sales excluding foreign currency translation grew 8%, with KFC at 8%, Pizza Hut at 7% and Taco Bell at 7%. Adjusting the prior year base to include Telepizza, system sales growth excluding foreign currency translation would have been 6% worldwide and 2% for the Pizza Hut Division. We opened 389 net units in the quarter. On a year-over-year basis, which takes into account the strategic alliance with Telepizza in the fourth-quarter 2018, net-new unit growth was 7%. We repurchased 1.5 million shares totaling $174 million at an average price per share of $115.

We recorded $60 million of pre-tax investment expense related to the change in fair value of our investment in Grubhub, which resulted in a negative ($0.15) impact in EPS. When coupled with $94 million of pre-tax investment income recorded in the third quarter of 2018, which resulted in a $0.22 benefit to EPS, our Grubhub investment unfavorably impacted year-over-year EPS growth by ($0.37). Foreign currency translation unfavorably impacted divisional operating profit by $7 million.

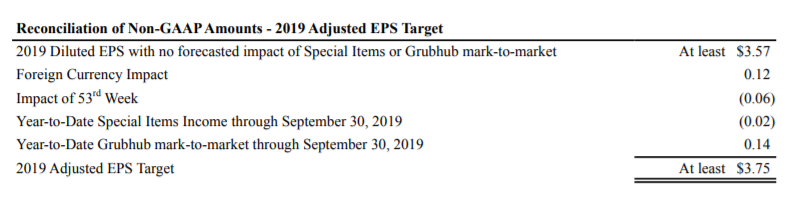

2019 EPS GUIDANCE

We have also provided certain forward-looking guidance using non-GAAP measurements. Specifically, in connection with the announcement of our strategic transformation initiatives in 2016, we announced a 2019 Diluted EPS target of at least $3.75 (“2019 Adjusted EPS Target”). This 2019 Adjusted EPS Target was intended to exclude:

• Any impact from changes in FX rates (i.e. FX rates were assumed not to change from those in place when we determined the 2019 Adjusted EPS Target in 2016)

• Any Special Items; and

• The impact of the 53rd week in 2019 for our U.S. businesses and certain international subsidiaries that report on a period calendar;

Additionally, we acquired an interest in Grubhub common stock subsequent to our original determination of the 2019 Adjusted EPS Target and thus are excluding any resulting mark-to-market adjustment for that investment from the 2019 Adjusted EPS target. At this time, we are unable to forecast any Special Items or Grubhub mark-to-market adjustments for the remainder of 2019 beyond amounts already recognized through September 30, 2019. The full year forecasted impacts of FX and the 53rd week and actual year-to-date impacts of Special Items and Grubhub mark-to-market adjustments on our 2019 Adjusted EPS Target are shown below. This impact of FX has been determined as the difference in translating our current local currency forecasts for 2019 at current FX forward rates and FX rates at the time the 2019 Adjusted EPS target was determined in 2016.

Greg Creed, CEO, said “Following a very strong first half of 2019 and in line with our expectations, third-quarter results were consistent with our long-term growth model. We delivered system sales growth of 8%, with same-store sales of 3% and net-new unit growth of 7%, led by continued strong performances at KFC International and Taco Bell. We’re rapidly approaching the end of a truly historic year. 2019 will not only mark the completion of our 3-year transformation of Yum!, but it will also mark the end of my tenure as Yum! CEO. I couldn’t be prouder of the progress that our teams around the world have made to become more focused, more franchised and more efficient; all while accelerating global growth. Today Yum! has a unique and powerful business model backed by a culture that is stronger than ever and by talent that is truly world class. I’m confident that as I retire, David Gibbs is the right leader to leverage our scale and key growth drivers to enhance franchisee economics, champion the customer experience and drive global growth to maximize value for our stakeholders.”

Third quarter highlights

Worldwide system sales excluding foreign currency translation grew 8%, with KFC at 8%, Pizza Hut at 7% and Taco Bell at 7%. Adjusting the prior year base to include Telepizza, system sales growth excluding foreign currency translation would have been 6% worldwide and 2% for the Pizza Hut Division. We opened 389 net units in the quarter. On a year-over-year basis, which takes into account the strategic alliance with Telepizza in the fourth-quarter 2018, net-new unit growth was 7%. We repurchased 1.5 million shares totaling $174 million at an average price per share of $115.

We recorded $60 million of pre-tax investment expense related to the change in fair value of our investment in Grubhub, which resulted in a negative ($0.15) impact in EPS. When coupled with $94 million of pre-tax investment income recorded in the third quarter of 2018, which resulted in a $0.22 benefit to EPS, our Grubhub investment unfavorably impacted year-over-year EPS growth by ($0.37). Foreign currency translation unfavorably impacted divisional operating profit by $7 million.

2019 EPS GUIDANCE

We have also provided certain forward-looking guidance using non-GAAP measurements. Specifically, in connection with the announcement of our strategic transformation initiatives in 2016, we announced a 2019 Diluted EPS target of at least $3.75 (“2019 Adjusted EPS Target”). This 2019 Adjusted EPS Target was intended to exclude:

• Any impact from changes in FX rates (i.e. FX rates were assumed not to change from those in place when we determined the 2019 Adjusted EPS Target in 2016)

• Any Special Items; and

• The impact of the 53rd week in 2019 for our U.S. businesses and certain international subsidiaries that report on a period calendar;

Additionally, we acquired an interest in Grubhub common stock subsequent to our original determination of the 2019 Adjusted EPS Target and thus are excluding any resulting mark-to-market adjustment for that investment from the 2019 Adjusted EPS target. At this time, we are unable to forecast any Special Items or Grubhub mark-to-market adjustments for the remainder of 2019 beyond amounts already recognized through September 30, 2019. The full year forecasted impacts of FX and the 53rd week and actual year-to-date impacts of Special Items and Grubhub mark-to-market adjustments on our 2019 Adjusted EPS Target are shown below. This impact of FX has been determined as the difference in translating our current local currency forecasts for 2019 at current FX forward rates and FX rates at the time the 2019 Adjusted EPS target was determined in 2016.

YUM! Brands (NYSE: YUM) stock price history

The image below, obtained from Google shows the stock price history of Yum! brands over the last 5 years, and it's been a pretty good time for Yum brands stockholders. 5 years ago the stock of Yum brands was trading at $51.70 and its currently trading at $103.34. That's a return of 99.8% provided to Yum brands over the last 5 years.. Yum brands stock is trading at close to the mid point between its 52 week high and 52 week low, which to us is an indication that the short term sentiment and momentum of Yum brands stock is neutral at this point in time. But with their latest earnings report disappointing it seems the stock of Yum brands might be in for more declines.

Yum Brands (NYSE: YUM) stock price history over the last 5 years.

Recent coverage of Yum Brands

The extract below discusses Yum brands 3rd quarter 20219 earnings report as obtained from TheStreet.com

KFC, Pizza Hut and Taco Bell parent Yum! Brands (YUM - Get Report) served up a third-quarter earnings and revenue miss, even after lowering the book value of its investment in Grubhub (GRUB - Get Report) and taking a hit of 15 cents a share for it. The company posted fiscal third-quarter net income of $255 million, or 81 cents a share, vs. $454 million, or $1.40 a share, a year earlier. Adjusted earnings were 80 cents a share. Analysts polled by FactSet had been expecting earnings of 96 cents a share. The company said it revalued its stake in online food delivery service Grubhub, which shaved 15 cents off its third-quarter per-share earnings.

That prompted investors to ditch the stock, with shares dropping nearly 8%, or $8.54 a share, to $101.11 in morning trading on Wednesday. Grubhub shares were up 2.64%, or 88 cents a share, at $33.98.

Read the full article here

KFC, Pizza Hut and Taco Bell parent Yum! Brands (YUM - Get Report) served up a third-quarter earnings and revenue miss, even after lowering the book value of its investment in Grubhub (GRUB - Get Report) and taking a hit of 15 cents a share for it. The company posted fiscal third-quarter net income of $255 million, or 81 cents a share, vs. $454 million, or $1.40 a share, a year earlier. Adjusted earnings were 80 cents a share. Analysts polled by FactSet had been expecting earnings of 96 cents a share. The company said it revalued its stake in online food delivery service Grubhub, which shaved 15 cents off its third-quarter per-share earnings.

That prompted investors to ditch the stock, with shares dropping nearly 8%, or $8.54 a share, to $101.11 in morning trading on Wednesday. Grubhub shares were up 2.64%, or 88 cents a share, at $33.98.

Read the full article here

Yum! Brands (NYSE: YUM) latest stock valuation

So what do we value Yum! Brands stock at after the release of their 3rd quarter 2019 earnings release. Based on Yum brands' latest earnings report and the earnings guidance provided our stock valuation models provides a target price (full value price) from Yum! brands at $83.60 a share. We therefore believe the stock of Yum Brands is overvalued.

We usually suggest that long term and fundamental investors get in at least 10% below our target (full value) price which in this case is $83.60. Therefore we believe a good entry point into Yum brands' stock is at $75.30 or below. We expect the stock of Yum brands' to pull back from current levels to levels closer to our target price (full value price) in coming weeks and moths as we believe it is overvalued at this point in time.

Since the stock of Yum Brands is trading at well above our target (full value) price and our suggested entry price we rate Yum Brands as a sell

We usually suggest that long term and fundamental investors get in at least 10% below our target (full value) price which in this case is $83.60. Therefore we believe a good entry point into Yum brands' stock is at $75.30 or below. We expect the stock of Yum brands' to pull back from current levels to levels closer to our target price (full value price) in coming weeks and moths as we believe it is overvalued at this point in time.

Since the stock of Yum Brands is trading at well above our target (full value) price and our suggested entry price we rate Yum Brands as a sell

Next earnings release of Yum Brands!

It is expected that Yum Brands will release their 4th quarter and full fiscal 2019 earnings report in late January 2020 to early February 2020