More about 401(k) and whether you should invest in a 401(k) or go it on your own?

|

Category: 401(k) and financial markets

Date: 28 April 2020 So you want to learn more about a 401(k)? What are the advantages and disadvantages of 401(k)'s? And in this day and age where more and more investment instruments are more readily available for everyday investors, should you invest in a 401(k) or should you look to manage your own investments and savings?

|

|

More about 401(k)

Lets take a look at 401(k). What are they, their benefits and their drawbacks. For this part we will look at a great write up on 401k's as obtained from the Wall Street Journal. Below the summary of 401k as obtained from WSJ.

A 401(k) is a retirement savings plan sponsored by an employer. It lets workers save and invest a piece of their paycheck before taxes are taken out. Taxes aren’t paid until the money is withdrawn from the account. 401(k) plans, named for the section of the tax code that governs them, arose during the 1980s as a supplement to pensions. Most employers used to offer pension funds. Pension funds were managed by the employer and they paid out a steady income over the course of the retirement. (If you have a government job or a strong union, you may might still be eligible for a pension.) But as the cost of running pensions escalated, employers started replacing them with 401(k)s.

With a 401(k), you control how your money is invested. Most plans offer a spread of mutual funds composed of stocks, bonds, and money market investments. The most popular option tends to be target-date funds, a combination of stocks and bonds that gradually become more conservative as you reach retirement.

While a 401(k)can help you save, it has plenty of restrictions and caveats. In most cases, you can’t tap into your employer’s contributions immediately. Vesting is the amount of time you must work for your company before gaining access to its payments to your 401(k). (Your payments, on the other hand, vest immediately.) It’s an insurance against employees leaving early. On top of that, there are complex rules about when you can withdraw your money and costly penalties for pulling funds out before retirement age.

To oversee your account, your employer usually hires an administrator like Fidelity Investments. They’ll email you updates about your plan and its performance, manage the paperwork and assist you with requests. If you want to keep watch over your account or shift your money around, go to your administrator’s web site or call their help center.

With that settled, how much should you put in? As much as possible, being mindful that you’ll need to have enough money to live, eat and pay down any debt you have. At the very least, invest enough to get the full matching amount that your company pays to match your contributions. You don’t want to leave free cash on the table. Nearly every plan offers matching funds—the most popular being 3% of your salary, according to the Profit Sharing/401k Council of America.

So how would a 3% match work? If you put in 3% of your $50,000 salary, or $1,500, your company puts another $1,500 in the pot. You can add more than that $1,500 yourself, but the company won’t match beyond 3%. The rules for matching funds vary, so be sure to check with your employer about qualifying for its contributions.

The IRS mandates contribution limits for 401(k) accounts. For 2007 and 2008, the most you can put into your fund is $15,500 in any combination of pre- and after-tax dollars. If you’re older than 49, you can kick in another $5,000. The total dollar amount that can be contributed—including both your contributions and your employers’—cannot exceed 100% of your salary or $46,000 in 2008.

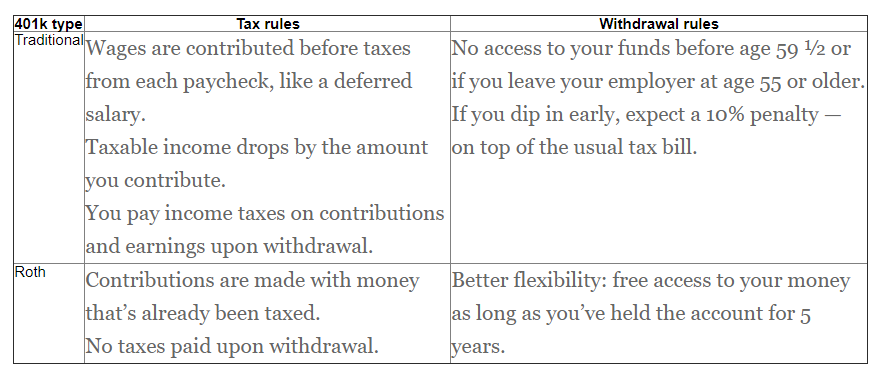

You’ll also want to consider the type of 401(k) you choose. They come in two varieties, the main differences being the tax implications and the schedule for accessing your funds. Chances are your company offers a traditional 401(k). Less common is a Roth 401(k). Here’s the breakdown of each:

A 401(k) is a retirement savings plan sponsored by an employer. It lets workers save and invest a piece of their paycheck before taxes are taken out. Taxes aren’t paid until the money is withdrawn from the account. 401(k) plans, named for the section of the tax code that governs them, arose during the 1980s as a supplement to pensions. Most employers used to offer pension funds. Pension funds were managed by the employer and they paid out a steady income over the course of the retirement. (If you have a government job or a strong union, you may might still be eligible for a pension.) But as the cost of running pensions escalated, employers started replacing them with 401(k)s.

With a 401(k), you control how your money is invested. Most plans offer a spread of mutual funds composed of stocks, bonds, and money market investments. The most popular option tends to be target-date funds, a combination of stocks and bonds that gradually become more conservative as you reach retirement.

While a 401(k)can help you save, it has plenty of restrictions and caveats. In most cases, you can’t tap into your employer’s contributions immediately. Vesting is the amount of time you must work for your company before gaining access to its payments to your 401(k). (Your payments, on the other hand, vest immediately.) It’s an insurance against employees leaving early. On top of that, there are complex rules about when you can withdraw your money and costly penalties for pulling funds out before retirement age.

To oversee your account, your employer usually hires an administrator like Fidelity Investments. They’ll email you updates about your plan and its performance, manage the paperwork and assist you with requests. If you want to keep watch over your account or shift your money around, go to your administrator’s web site or call their help center.

With that settled, how much should you put in? As much as possible, being mindful that you’ll need to have enough money to live, eat and pay down any debt you have. At the very least, invest enough to get the full matching amount that your company pays to match your contributions. You don’t want to leave free cash on the table. Nearly every plan offers matching funds—the most popular being 3% of your salary, according to the Profit Sharing/401k Council of America.

So how would a 3% match work? If you put in 3% of your $50,000 salary, or $1,500, your company puts another $1,500 in the pot. You can add more than that $1,500 yourself, but the company won’t match beyond 3%. The rules for matching funds vary, so be sure to check with your employer about qualifying for its contributions.

The IRS mandates contribution limits for 401(k) accounts. For 2007 and 2008, the most you can put into your fund is $15,500 in any combination of pre- and after-tax dollars. If you’re older than 49, you can kick in another $5,000. The total dollar amount that can be contributed—including both your contributions and your employers’—cannot exceed 100% of your salary or $46,000 in 2008.

You’ll also want to consider the type of 401(k) you choose. They come in two varieties, the main differences being the tax implications and the schedule for accessing your funds. Chances are your company offers a traditional 401(k). Less common is a Roth 401(k). Here’s the breakdown of each:

Most companies allow you to enroll in a 401(k) right away, although some smaller employers might make you wait up to a year. If that’s the case, set up an individual retirement account, and lodge a complaint with your employer’s HR office. Some companies will automatically register you. You can normally increase or decrease your contributions at any time. Don’t forget to elect a beneficiary, or the person who gets your money if you die. (If you’re married, your spouse is automatically the beneficiary.)

Finally, if your company is on shaky ground, don’t fret. Your 401(k) is off-limits. If your company goes under, the plan would most likely be terminated. If that happens, you should roll the money over into a traditional IRA to avoid paying the 10% withdrawal penalty and income taxes

Read the original article here

Finally, if your company is on shaky ground, don’t fret. Your 401(k) is off-limits. If your company goes under, the plan would most likely be terminated. If that happens, you should roll the money over into a traditional IRA to avoid paying the 10% withdrawal penalty and income taxes

Read the original article here

Updated contributions to 401(k) in 2020

The write up from the Wall Street Journal is pretty outdated and refers to values of 2007 and 2008. The annual contribution limits on 401(k) in for 2020 is as follows:

Under the age of 50 Over the age of 50

So why the increased contribution of those over 50. Well the fact is they are a lot closer to retirement and the increased contribution limits provides those closer to retirement to boost their retirement savings.

Under the age of 50 Over the age of 50

- $19 500 $19 500 + $6500

So why the increased contribution of those over 50. Well the fact is they are a lot closer to retirement and the increased contribution limits provides those closer to retirement to boost their retirement savings.

So how should you go about selecting a 401(k)

The following article written by Matt Becker and published on Thesimpledollar suggests doing the following when it comes to deciding on 401(k) investments.

Your 401(k) is one of the best and most effective ways to get started investing, even if you don’t have a lot of money to invest. But there’s a big question that comes up as soon as you start contributing: Which investments should you choose? It’s confusing trying to navigate the long list of options with strange acronyms and lots of numbers next to them. So confusing that many people end up inadvertently making poor decisions.

In this post you’ll learn how to choose the right investments in your 401(k) so you have the best possible chance of reaching your biggest personal goals.

Choosing Your 401(k) Investing GoalsHere’s one tip that will instantly make you a more sophisticated investor than almost everyone else you know: Instead of looking at your 401(k) as its own, isolated account, look at it as just one part of your overall investment plan — which includes all of your investment accounts.

That means you don’t have to perfectly or entirely match your target investment plan within your 401(k). Your real goal is to match your target investment plan once all your investments are summed up across all accounts. Which is good news! Because your 401(k) investment options are probably limited. There are likely some good options and some not-so-good ones, and it’s unlikely that there’s a good one for each type of thing you want to invest in. For example, there may be a great U.S. stock market fund, but not a great international stock market fund. And by viewing all your retirement accounts as one big pot, and including your spouse or partner’s retirement accounts as well, you can pick and choose the best investment options in each one so that the total across all accounts lines up with your overall plan.

Here’s how to do just that.

Step 1: Create an Overall Investment Plan

Start by laying out your overarching investment objectives:

Step 2: Review Your 401(k) Investment Options

Ask your employer for a list of the investment options within your 401(k) and evaluate them on the following two factors:

It’s likely that your 401(k) offers a suite of target-date retirement funds, which are essentially mutual funds comprised of other mutual funds in a mix that varies based on your expected retirement date. For example, a 2050 fund (geared toward someone expecting to retire in 34 years) might be heavily invested in stock-based funds, while a 2020 fund (aimed at someone retiring in just four years) would likely hold more bond funds or other conservative investments.

Target-date funds can make things a lot easier on you, since you may only have to pick one fund and be done with it. Just make sure that any target-date fund you choose is both low-cost and a relatively close fit with your desired asset allocation – and be aware that its own allocation will shift (usually toward less risky investments) as time goes on.

Step 3: Rank Your 401(k) Investment Options

As you go through the list, you can cross off anything that either doesn’t fit into your plan or costs too much.

Then take the remaining options and rank them in general order of fit and cost. Those at the top are the investments you’re most likely to choose.

As you do this, I would consider giving strong preference to anything labeled as an index fund. That’s because low-cost index funds have been shown to outperform other investments 80% to 90% of the time.

Step 4: Work Through Your 401(k) Options in Order of Priority

First, go back to Step 1 where you decided on your asset allocation and determined how much money you wanted to put into each type of investment. You’ll need that information here. Then, start with the 401(k) investment option you ranked as the best fit. Allocate your 401(k) money toward that investment until you’ve either used up your entire 401(k) or you’ve reached the limit for how much you want to invest in that particular thing.

For example, let’s say that you’re investing $10,000 a year across all your retirement accounts, and you want 50% of that, or $5,000, to go into the U.S. stock market. If you have a good, low-cost, U.S. stock market fund in your 401(k), you can select to put up to $5,000 of your 401(k) contributions into that fund. (To find the total amount you’re putting into your 401(k) each year, just multiply your salary by your contribution rate: for example, $60,000 x 9% = $5,400.) If you’ll contribute less than $5,000 to your 401(k) per year, then the entire balance would go into that one fund.

If you have money left over in your 401(k) after Fund No. 1, do the same thing for Fund No. 2 in your priority list. Keep working your way down the list until you’ve used up your entire 401(k).

Step 5: Fill in Any Gaps Using Other Accounts

If all of your retirement money is in your 401(k), then you’re done. Nice work!

If not, you can fill out the rest of your investment plan with your other retirement accounts, like your IRA. The reason you save this step for last is that your 401(k) options are likely limited, while your IRA options are essentially unlimited. This way you make the most of the good options in your 401(k), and fill in the gaps elsewhere.

Remember to Revisit and Rebalance

As time passes and the markets move, the amount of money you have invested in each fund will rise and fall. Your 401(k) may also change its investment lineup from time to time. So it’s a good idea to review your investments annually to rebalance and make any other necessary adjustments based on changes in your plan.

Matt Becker is a fee-only financial planner and the founder of Mom and Dad Money, where he helps new parents take control of their money so they can take care of their families. His free book, The New Family Financial Road Map, guides parents through the all most important financial decisions that come with starting a family

Read the original article here

Your 401(k) is one of the best and most effective ways to get started investing, even if you don’t have a lot of money to invest. But there’s a big question that comes up as soon as you start contributing: Which investments should you choose? It’s confusing trying to navigate the long list of options with strange acronyms and lots of numbers next to them. So confusing that many people end up inadvertently making poor decisions.

In this post you’ll learn how to choose the right investments in your 401(k) so you have the best possible chance of reaching your biggest personal goals.

Choosing Your 401(k) Investing GoalsHere’s one tip that will instantly make you a more sophisticated investor than almost everyone else you know: Instead of looking at your 401(k) as its own, isolated account, look at it as just one part of your overall investment plan — which includes all of your investment accounts.

That means you don’t have to perfectly or entirely match your target investment plan within your 401(k). Your real goal is to match your target investment plan once all your investments are summed up across all accounts. Which is good news! Because your 401(k) investment options are probably limited. There are likely some good options and some not-so-good ones, and it’s unlikely that there’s a good one for each type of thing you want to invest in. For example, there may be a great U.S. stock market fund, but not a great international stock market fund. And by viewing all your retirement accounts as one big pot, and including your spouse or partner’s retirement accounts as well, you can pick and choose the best investment options in each one so that the total across all accounts lines up with your overall plan.

Here’s how to do just that.

Step 1: Create an Overall Investment Plan

Start by laying out your overarching investment objectives:

- How much money will you sock away? Remember that your contribution rate is the most important investment decision you’ll make, so get this going before worrying about anything else.

- Which accounts will you use? Contributing to your 401(k) up to your employer match is a great start. But after that you have a number of options, and the right one depends on your specific situation. Decide which accounts you want to use and how much you’ll be contributing to each one.

- What is your target asset allocation? That is, which types of things will you be investing in (e.g., U.S. stocks, international stocks, bonds), and how much of your money will be invested in each type?

Step 2: Review Your 401(k) Investment Options

Ask your employer for a list of the investment options within your 401(k) and evaluate them on the following two factors:

- How does each one fit into your asset allocation? If it’s not a fit, you can ignore it. Morningstar is a good resource for looking up mutual funds to see what they invest in.

- How much do they cost? Cost is the single best predictor of future returns, so you should lean toward investments that cost less — meaning they have a lower expense ratio and fee structure.

It’s likely that your 401(k) offers a suite of target-date retirement funds, which are essentially mutual funds comprised of other mutual funds in a mix that varies based on your expected retirement date. For example, a 2050 fund (geared toward someone expecting to retire in 34 years) might be heavily invested in stock-based funds, while a 2020 fund (aimed at someone retiring in just four years) would likely hold more bond funds or other conservative investments.

Target-date funds can make things a lot easier on you, since you may only have to pick one fund and be done with it. Just make sure that any target-date fund you choose is both low-cost and a relatively close fit with your desired asset allocation – and be aware that its own allocation will shift (usually toward less risky investments) as time goes on.

Step 3: Rank Your 401(k) Investment Options

As you go through the list, you can cross off anything that either doesn’t fit into your plan or costs too much.

Then take the remaining options and rank them in general order of fit and cost. Those at the top are the investments you’re most likely to choose.

As you do this, I would consider giving strong preference to anything labeled as an index fund. That’s because low-cost index funds have been shown to outperform other investments 80% to 90% of the time.

Step 4: Work Through Your 401(k) Options in Order of Priority

First, go back to Step 1 where you decided on your asset allocation and determined how much money you wanted to put into each type of investment. You’ll need that information here. Then, start with the 401(k) investment option you ranked as the best fit. Allocate your 401(k) money toward that investment until you’ve either used up your entire 401(k) or you’ve reached the limit for how much you want to invest in that particular thing.

For example, let’s say that you’re investing $10,000 a year across all your retirement accounts, and you want 50% of that, or $5,000, to go into the U.S. stock market. If you have a good, low-cost, U.S. stock market fund in your 401(k), you can select to put up to $5,000 of your 401(k) contributions into that fund. (To find the total amount you’re putting into your 401(k) each year, just multiply your salary by your contribution rate: for example, $60,000 x 9% = $5,400.) If you’ll contribute less than $5,000 to your 401(k) per year, then the entire balance would go into that one fund.

If you have money left over in your 401(k) after Fund No. 1, do the same thing for Fund No. 2 in your priority list. Keep working your way down the list until you’ve used up your entire 401(k).

Step 5: Fill in Any Gaps Using Other Accounts

If all of your retirement money is in your 401(k), then you’re done. Nice work!

If not, you can fill out the rest of your investment plan with your other retirement accounts, like your IRA. The reason you save this step for last is that your 401(k) options are likely limited, while your IRA options are essentially unlimited. This way you make the most of the good options in your 401(k), and fill in the gaps elsewhere.

Remember to Revisit and Rebalance

As time passes and the markets move, the amount of money you have invested in each fund will rise and fall. Your 401(k) may also change its investment lineup from time to time. So it’s a good idea to review your investments annually to rebalance and make any other necessary adjustments based on changes in your plan.

Matt Becker is a fee-only financial planner and the founder of Mom and Dad Money, where he helps new parents take control of their money so they can take care of their families. His free book, The New Family Financial Road Map, guides parents through the all most important financial decisions that come with starting a family

Read the original article here

So should one invest in a 401(k) or IRA

This is the million dollar question. While there are significant tax benefits in investing in a 401(k) or IRA the problem is the restrictions and limitations on these. For example for some 401(k) investors can only access their employers contribution to their 401(k) after a prolonged period of time, keeping investors locked in at a particular employer for longer, and access these funds before the age of 60 has penalty implications. So one has to weigh up the benefits against the drawbacks.

Another option is to skip the 401(k) and just invest after tax salary money in a particular fund or exchange traded fund (ETF). Preferably a low cost index tracker type fund or two which gives exposure to the US stock market as well as few offshore options. Depending on your age and risk appetite a few funds or tracker funds in higher growth countries such as China and India which are a little riskier but could potentially offer far greater returns over longer periods of time should be considered.

In the end there is no silver bullet or one package that address all the needs of all investors, and it all depends on one's individual circumstances. But one thing all financial planners and investment analysts agree on. Start investing and saving for retirement as soon as you can and keep an eye on the fees of the funds you invest in and look to rebalance and adjust your retirement savings and investments as your age and circumstances and the investment environment change

Another option is to skip the 401(k) and just invest after tax salary money in a particular fund or exchange traded fund (ETF). Preferably a low cost index tracker type fund or two which gives exposure to the US stock market as well as few offshore options. Depending on your age and risk appetite a few funds or tracker funds in higher growth countries such as China and India which are a little riskier but could potentially offer far greater returns over longer periods of time should be considered.

In the end there is no silver bullet or one package that address all the needs of all investors, and it all depends on one's individual circumstances. But one thing all financial planners and investment analysts agree on. Start investing and saving for retirement as soon as you can and keep an eye on the fees of the funds you invest in and look to rebalance and adjust your retirement savings and investments as your age and circumstances and the investment environment change

Google search term trends for 401(K) and ETF

The graphic below shows the search trends from Google Trends for 401(k) and ETF over the last 12 months in the United States. While 401k generates more search results than ETF's at this point in time the trends in ETF has seen a significant spike since the start of March. Question is whether this is due to the fact that the number of unemployed in the USA has increased significantly over the last 2 months as the full impact of the Coronavirus and related lockdowns takes its toll. Are people who lost their jobs looking to invest their vested 401(k)'s in ETF's? We certainly think so.