|

Related Topics

|

|

Category: Brown-Forman and Stock Market

Last updated: 10 June 2020 Stock price: $69.14 On this page we will look to provide more details, often not covered by mainstream financial websites of Brown-Forman, a distiller whose brands include Jack Daniels and el Jimador tequila with revenues for the 4th quarter 2020 topping $709 million.

|

|

About Brown-Forman

Brown-Forman Corporation (the “Company,” “Brown-Forman,” “we,” “us,” or “our” below) was incorporated under the laws of the State of Delaware in 1933, successor to a business founded in 1870 as a partnership and later incorporated under the laws of the Commonwealth of Kentucky in 1901. We primarily manufacture, bottle, import, export, market, and sell a wide variety of alcoholic beverages under recognized brands.

We employ approximately 4,700 people on six continents (excluding individuals that work on a part-time or temporary basis), including approximately 1,200 people in Louisville, Kentucky, USA, home of our world headquarters. We are the largest American-owned spirits and wine company with global reach. We primarily manufacture, bottle, import, export, market, and sell a wide variety of alcoholic beverages under recognized brands. We are a “controlled company” under New York Stock Exchange rules because the Brown family owns more than 50% of our voting stock. Taking into account ownership of shares of our non-voting stock, the Brown family also controls more than 50% of the economic ownership in BrownForman.

We employ approximately 4,700 people on six continents (excluding individuals that work on a part-time or temporary basis), including approximately 1,200 people in Louisville, Kentucky, USA, home of our world headquarters. We are the largest American-owned spirits and wine company with global reach. We primarily manufacture, bottle, import, export, market, and sell a wide variety of alcoholic beverages under recognized brands. We are a “controlled company” under New York Stock Exchange rules because the Brown family owns more than 50% of our voting stock. Taking into account ownership of shares of our non-voting stock, the Brown family also controls more than 50% of the economic ownership in BrownForman.

Woodford reserve bourbon

Quick facts about Brown-Forman

- Brown-Forman is listed on the New York Stock Exchange under share code ticker: BF.B

- Market capital of Brown-Forman: $35.4 billion

- Number of employees of Brown-Forman: 4 700

- Net Sales of Brown-Forman 1Q 2020: $704 million

- Net sales of Brown-Forman in fiscal 2019: $2.994 billion

- Earnings per share for Brown-Forman in fiscal 2019: $1.37

- Cash on balance sheet as at end of fiscal 2019: $239 million

- Goodwill of Brown-Forman: $763 million

- Goodwill shows the estimated value of their brands names and the brands of the group.

- Shares in issue: 510 million

- Stockholders equity in Brown-Forman: $1.316 billion

- Stockholders equity per share: $2.58

Brown-Forman Brands

Beginning in 1870 with Old Forester Kentucky Straight Bourbon Whisky – our founding brand – and spanning the generations since, we have built a portfolio of more than 40 spirit, ready-to-drink (RTD) cocktail, and wine brands that includes some of the best-known and most loved trademarks in our industry. The most important brand in our portfolio is Jack Daniel’s Tennessee Whiskey, which was ranked in the 2018 Interbrand “Best Global Brands” as the most valuable global spirits brand in the world and the second most valuable beverage alcohol brand. Jack Daniel’s Tennessee Whiskey is the largest American whiskey brand in the world and the fourth-largest spirits brand of any kind, according to Impact Databank’s “Top 100 Premium Spirits Brands Worldwide” list. Among the top five premium spirits brands on the list, Jack Daniel’s Tennessee Whiskey was the only one to grow volume in each of the past five years. Our other leading global brands on the Worldwide Impact list are Finlandia, which is the tenth-largest-selling vodka; Jack Daniel’s Tennessee Honey, which is the second-largest-selling flavored whiskey; and el Jimador, which grew to become the fourth-largest-selling tequila. Woodford Reserve was once again selected as an Impact “Hot Brand,”1 marking six consecutive years on the list. Old Forester and Pepe Lopez were also named to the 2018 “Hot Brand”1 list.

We seek to build brands and businesses that create significant shareholder value, by delivering strong and sustainable growth, solid margins, and high returns on invested capital. In addition, given our growing size and scale, we focus on building brands that can be meaningful for our company over time. Our first priority is to grow our premium spirits portfolio organically and through innovation. As opportunities arise, we also consider acquisitions and partnerships that will enhance our portfolio and our capacity to deliver growth, margins, and returns in line with our rigorous quantitative and qualitative criteria. We are the global leader in American whiskey. We see significant, additional opportunity to promote the mixability, versatility, accessibility, and premiumization of our American whiskey brands around the world. We believe that we can leverage our whiskey-making knowledge, production assets, trademarks, and brand-building skills to realize this opportunity.

The Jack Daniel’s family of brands, led by Jack Daniel’s Tennessee Whiskey (JDTW), is our most valuable asset – the engine of our overall financial performance and the foundation of our leadership position in the American whiskey category. We will always work to keep JDTW strong, healthy, and relevant to consumers worldwide while pursuing the abundant opportunities to grow the Jack Daniel’s family of brands across markets, premium price points, channels, and consumer groups. Product innovation continues to be a meaningful contributor to our performance. New Jack Daniel’s expressions have led innovation in the American whiskey category, including Honey (2011), Fire (2015), Rye (2017), and the recently announced launch of Jack Daniel’s Tennessee Apple, which we expect to introduce in the United States in the fall of 2019.

Beyond the Jack Daniel’s family of brands, we expect to sustain excellent growth around the world with our other whiskey brands, particularly Woodford Reserve and Old Forester. Woodford Reserve is the leading super-premium American whiskey globally1 , and is poised for continued growth as interest in bourbon continues to increase around the world. Old Forester has continued its return to prominence in the United States and in select international markets through its unparalleled taste and quality. Following on the success of its high-end expressions, including the Old Forester Whiskey Row Series, we recently added Old Forester Rye to the brand line up. 1 IWSR, 2018 data. 10 We believe that super- and ultra-premium whiskeys are an attractive long-term business. Through our acquisition of The BenRiach Distillery Company Limited in June 2016, we added three world-class single malt Scotch whisky brands to our portfolio: The GlenDronach, BenRiach, and Glenglassaugh. Since acquiring the Scotch business, we have evolved our portfolio and geographic strategies to ensure that these single malt brands are positioned to become meaningful contributors to Brown-Forman and significant competitors in the fast-growing single malt category over the longer term.

Similarly, Slane Irish Whiskey, which opened its distillery and visitors’center in 2018 is poised to become a meaningful contributor for the Company in the fast-growing Irish whiskey category over time. It has been over a decade since we acquired Casa Herradura, a portfolio led by two tequila brands steeped in Mexican heritage – Herradura and el Jimador. Despite current cost pressures resulting from the high price of agave, we remain pleased with the development of our tequila business in both Mexico and the United States, the brands’ two primary markets. We plan to continue expanding Herradura to reach new consumers in Mexico, the United States, and other high-potential markets. In addition to the success of the brand’s core expressions, Herradura Ultra – an ultra-premium “cristalino” line extension – continued to accelerate, surpassing 90,000 nine-liter cases in fiscal 2019. We intend to ensure el Jimador tequila remains a premium brand in Mexico by increasing pricing again in fiscal 2020, and remain encouraged by our prospects for long-term, profitable growth there.

Outside Mexico, we have more than quadrupled el Jimador’s volumes since fiscal 2008. We remain confident in el Jimador’s potential to improve its position among the world’s leading tequila brands as the category continues to develop. Finlandia, one of the top-ten selling vodkas in the world,1 is prominent in several of the world’s largest vodka markets, such as Poland, Russia, Ukraine, and Czechia. We plan to grow Finlandia where its position is strong, including in its largest market, Poland, where Finlandia accounts for one out of every two bottles of imported vodka sold.

Principal Brands

We seek to build brands and businesses that create significant shareholder value, by delivering strong and sustainable growth, solid margins, and high returns on invested capital. In addition, given our growing size and scale, we focus on building brands that can be meaningful for our company over time. Our first priority is to grow our premium spirits portfolio organically and through innovation. As opportunities arise, we also consider acquisitions and partnerships that will enhance our portfolio and our capacity to deliver growth, margins, and returns in line with our rigorous quantitative and qualitative criteria. We are the global leader in American whiskey. We see significant, additional opportunity to promote the mixability, versatility, accessibility, and premiumization of our American whiskey brands around the world. We believe that we can leverage our whiskey-making knowledge, production assets, trademarks, and brand-building skills to realize this opportunity.

The Jack Daniel’s family of brands, led by Jack Daniel’s Tennessee Whiskey (JDTW), is our most valuable asset – the engine of our overall financial performance and the foundation of our leadership position in the American whiskey category. We will always work to keep JDTW strong, healthy, and relevant to consumers worldwide while pursuing the abundant opportunities to grow the Jack Daniel’s family of brands across markets, premium price points, channels, and consumer groups. Product innovation continues to be a meaningful contributor to our performance. New Jack Daniel’s expressions have led innovation in the American whiskey category, including Honey (2011), Fire (2015), Rye (2017), and the recently announced launch of Jack Daniel’s Tennessee Apple, which we expect to introduce in the United States in the fall of 2019.

Beyond the Jack Daniel’s family of brands, we expect to sustain excellent growth around the world with our other whiskey brands, particularly Woodford Reserve and Old Forester. Woodford Reserve is the leading super-premium American whiskey globally1 , and is poised for continued growth as interest in bourbon continues to increase around the world. Old Forester has continued its return to prominence in the United States and in select international markets through its unparalleled taste and quality. Following on the success of its high-end expressions, including the Old Forester Whiskey Row Series, we recently added Old Forester Rye to the brand line up. 1 IWSR, 2018 data. 10 We believe that super- and ultra-premium whiskeys are an attractive long-term business. Through our acquisition of The BenRiach Distillery Company Limited in June 2016, we added three world-class single malt Scotch whisky brands to our portfolio: The GlenDronach, BenRiach, and Glenglassaugh. Since acquiring the Scotch business, we have evolved our portfolio and geographic strategies to ensure that these single malt brands are positioned to become meaningful contributors to Brown-Forman and significant competitors in the fast-growing single malt category over the longer term.

Similarly, Slane Irish Whiskey, which opened its distillery and visitors’center in 2018 is poised to become a meaningful contributor for the Company in the fast-growing Irish whiskey category over time. It has been over a decade since we acquired Casa Herradura, a portfolio led by two tequila brands steeped in Mexican heritage – Herradura and el Jimador. Despite current cost pressures resulting from the high price of agave, we remain pleased with the development of our tequila business in both Mexico and the United States, the brands’ two primary markets. We plan to continue expanding Herradura to reach new consumers in Mexico, the United States, and other high-potential markets. In addition to the success of the brand’s core expressions, Herradura Ultra – an ultra-premium “cristalino” line extension – continued to accelerate, surpassing 90,000 nine-liter cases in fiscal 2019. We intend to ensure el Jimador tequila remains a premium brand in Mexico by increasing pricing again in fiscal 2020, and remain encouraged by our prospects for long-term, profitable growth there.

Outside Mexico, we have more than quadrupled el Jimador’s volumes since fiscal 2008. We remain confident in el Jimador’s potential to improve its position among the world’s leading tequila brands as the category continues to develop. Finlandia, one of the top-ten selling vodkas in the world,1 is prominent in several of the world’s largest vodka markets, such as Poland, Russia, Ukraine, and Czechia. We plan to grow Finlandia where its position is strong, including in its largest market, Poland, where Finlandia accounts for one out of every two bottles of imported vodka sold.

Principal Brands

- Jack Daniel’s Tennessee Whiskey

- el Jimador Tequilas

- Jack Daniel’s RTDs

- el Jimador New Mix RTDs

- Jack Daniel’s Tennessee Honey

- Herradura Tequilas

- Gentleman Jack Rare Tennessee Whiskey

- Sonoma-Cutrer California Wines

- Jack Daniel’s Tennessee Fire

- Canadian Mist Canadian Whisky

- Jack Daniel’s Single Barrel Collection GlenDronach Single Malt Scotch Whisky Jack Daniel’s Tennessee Rye

- BenRiach Single Malt Scotch Whisky

- Jack Daniel’s Sinatra Select

- Glenglassaugh Single Malt Scotch Whisky

- Jack Daniel’s No. 27 Gold Tennessee Whiskey

- Old Forester Kentucky Straight Bourbon Whisky

- Jack Daniel’s Winter Jack

- Old Forester Whiskey Row Series

- Jack Daniel’s Bottled-in-Bond

- Old Forester Kentucky Straight Rye Whisky

- Woodford Reserve Kentucky Bourbon

- Chambord Liqueur

- Woodford Reserve Double Oaked

- Early Times Kentucky Whisky and Bourbon

- Woodford Reserve Kentucky Rye Whiskey

- Pepe Lopez Tequila

- Woodford Reserve Kentucky Straight Malt Whiskey

- Antiguo Tequila

- Finlandia Vodkas

- Slane Irish Whiskey

- Korbel California Champagnes

- Coopers’ Craft Kentucky Bourbon

Markets for Brown-Forman

Markets We sell our products in over 170 countries around the world. The United States, our most important market, accounted for 47% of our net sales in fiscal 2019. We generated 53% of our net sales outside the United States in fiscal 2019. Our largest international markets include the United Kingdom, Mexico, Australia, Germany, France, Poland, Russia, Japan, and Brazil. We present the percentage of total net sales by geographic area for our most recent five fiscal years below:

Percentage of Total Net Sales by Geographic Area Year ended April 30, 2019

United States 47%

International:

The United States remains our largest market, and continuing to grow there is important to our long-term success. We expect to foster this growth by emphasizing fast-growing spirits categories such as super-premium whiskeys and tequilas, continued product and packaging innovation, and brand building within growing consumer segments, including increasing emphasis on inclusive marketing. Over the last two decades, our business outside the United States has generally grown faster than our business within it. Achieving our long-term growth objectives requires us to deliver balanced geographic growth while increasing our competitiveness through improved routes to consumer. We expect to continue to grow our business in developed markets such as Australia, France, Germany, and the United Kingdom. We will continue to pursue RTC strategies that will expand our access to and understanding of consumers, with the most recent example being the establishment of our owned distribution organization in Spain during fiscal 2018. In addition, we expect increasingly significant contributions to our growth from emerging markets including Africa, Brazil, China, Eastern Europe, Latin America, Mexico, Poland, Russia, Southeast Asia, and Turkey.

Percentage of Total Net Sales by Geographic Area Year ended April 30, 2019

United States 47%

International:

- Europe: 26 %

- Australia: 5 %

- Other: 22 %

- Total International: 53%

The United States remains our largest market, and continuing to grow there is important to our long-term success. We expect to foster this growth by emphasizing fast-growing spirits categories such as super-premium whiskeys and tequilas, continued product and packaging innovation, and brand building within growing consumer segments, including increasing emphasis on inclusive marketing. Over the last two decades, our business outside the United States has generally grown faster than our business within it. Achieving our long-term growth objectives requires us to deliver balanced geographic growth while increasing our competitiveness through improved routes to consumer. We expect to continue to grow our business in developed markets such as Australia, France, Germany, and the United Kingdom. We will continue to pursue RTC strategies that will expand our access to and understanding of consumers, with the most recent example being the establishment of our owned distribution organization in Spain during fiscal 2018. In addition, we expect increasingly significant contributions to our growth from emerging markets including Africa, Brazil, China, Eastern Europe, Latin America, Mexico, Poland, Russia, Southeast Asia, and Turkey.

Casa Herradura

Competition of Brown-Forman

Trade information indicates that we are one of the largest global suppliers of premium spirits. According to International Wine & Spirit Research (IWSR), for calendar year 2018, the ten largest global spirits companies controlled less than 20% of the total global market for spirits (on a volume basis). While we believe that the overall market environment offers considerable growth opportunities for us, our industry is now, and will remain, highly competitive. We compete against many global, regional, and local brands in a variety of categories of beverage alcohol, but our brands compete primarily in the industry’s premium-and-higher price categories. Our competitors include major global spirits and wine companies, such as Bacardi Limited, Becle S.A.B. de C.V., Beam Suntory Inc., Davide Campari-Milano S.p.A., Diageo PLC, LVMH Moët Hennessy Louis Vuitton SE, Pernod Ricard SA, and Rémy Cointreau. In addition, particularly in the United States, we increasingly compete with national companies and craft spirit brands, many of which are recent entrants to the industry. Brand recognition, brand provenance, quality of product and packaging, availability, flavor profile, and price affect consumers’ choices among competing brands in our industry. Several factors influence consumers’ buying decisions, including advertising, promotions, merchandising at the point of sale, expert or celebrity endorsement, social media and word of mouth, and the timing and relevance of new product introductions. Although some competitors have substantially greater resources than we do, we believe that our competitive position is strong, particularly as it relates to brand recognition, quality, availability, and relevance of new product introductions

If we are unable to enhance the foregoing customer connection, our ability to compete and our financial condition, results of operations, or cash flows could be adversely affected. We believe our Restock Kroger plan provides a balanced approach that will enable us to meet the wide-ranging needs and expectations of our customers. However, we may be unsuccessful in implementing Restock Kroger, including our alternative profit strategy and our cost savings initiatives, which could adversely affect our relationships with our customers, our market share and business growth, and our operations and results. The nature and extent to which our competitors respond to the evolving and competitive industry by developing and implementing their competitive strategies could adversely affect our profitability.

If we are unable to enhance the foregoing customer connection, our ability to compete and our financial condition, results of operations, or cash flows could be adversely affected. We believe our Restock Kroger plan provides a balanced approach that will enable us to meet the wide-ranging needs and expectations of our customers. However, we may be unsuccessful in implementing Restock Kroger, including our alternative profit strategy and our cost savings initiatives, which could adversely affect our relationships with our customers, our market share and business growth, and our operations and results. The nature and extent to which our competitors respond to the evolving and competitive industry by developing and implementing their competitive strategies could adversely affect our profitability.

Intellectual property and trademarks of Brown-Forman

Our intellectual property includes trademarks, copyrights, proprietary packaging and trade dress, proprietary manufacturing technologies, know-how, and patents. Our intellectual property, especially our trademarks, is essential to our business. We register our trademarks broadly around the world, focusing primarily on where we sell or expect to sell our products. We protect our intellectual property rights vigorously but fairly. We have licensed some of our trademarks to third parties for use with services or on products other than alcoholic beverages, which enhances the awareness and protection of our brands.

Employees of Brown-Forman

Brown‑Forman has approximately 4,700 employees around the world. On average, our employees stay eight years, which is more than double the average tenure for all industries in the United States, according to the U.S. Bureau of Labor Statistics in 2018. We take care of our employees with benefits such as the recently updated flexible work options, parental leave, and extended bereavement leave for United States employees. We also offer health and wellness programs, pension and 401(k) plans, and convenient onsite amenities. On Glassdoor.com, employees have rated Brown‑Forman with 4.4 stars (out of five) for benefits.

Seasonality of Brown-Forman earnings

Holiday buying makes the fourth calendar quarter the peak season for our business. Approximately 30%, 31%, and 31% of our net sales for fiscal 2017, fiscal 2018, and fiscal 2019, respectively, were in the fourth calendar quarter.

Brown-Forman (NYSE: BF.B) stock performance

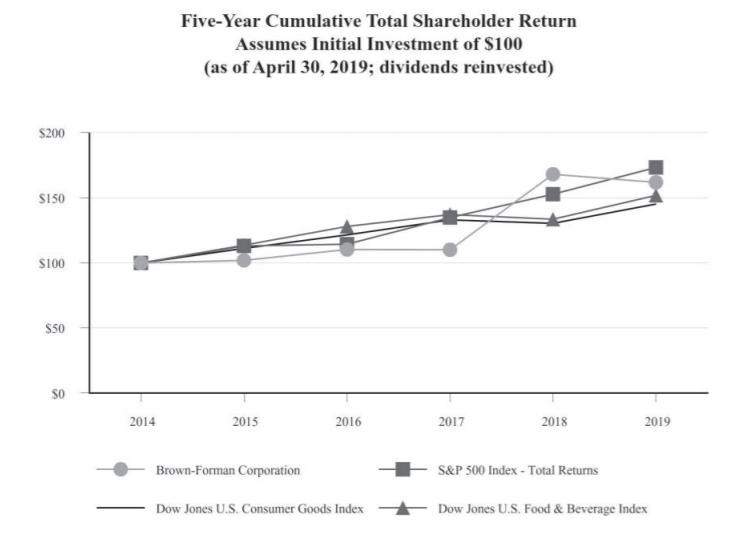

The graph below compares the cumulative total shareholder return of our Class B common stock for the last five fiscal years with the Standard & Poor’s 500 Index, the Dow Jones U.S. Consumer Goods Index, and the Dow Jones U.S. Food & Beverage Index. The information presented assumes an initial investment of $100 on April 30, 2014, and that all dividends were reinvested. The graph shows the value that each of these investments would have had on April 30 in the years since 2014.

Brown-Forman vs S&P vs Dow Jones US consumer goods vs Dow Jones US Food and Beverage Index

Our latest Brown-Foreman stock valuation (9 June 2020)

Based on the Brown-Forman's 4th quarter 2020 earnings report what do we value the group's stock at? Based on their earnings reported our valuation model prices a target price (full value price) for Brown-Forman stock at $64.20 a stock.

We therefore believe the stock of Brown-Forman is overvalued.

We usually recommend that long term and value investors look to enter a stock at least 10% below our target price (full value price) which in this case is $64.20, a good entry point would therefore be at $57.80 or below. We expect the stock of Brown-Forman to pull back slightly from its current price to levels closer to our target price (full value price) in coming weeks and months.

We therefore believe the stock of Brown-Forman is overvalued.

We usually recommend that long term and value investors look to enter a stock at least 10% below our target price (full value price) which in this case is $64.20, a good entry point would therefore be at $57.80 or below. We expect the stock of Brown-Forman to pull back slightly from its current price to levels closer to our target price (full value price) in coming weeks and months.