|

Related Topics

|

|

Category: Stock Market and Netflix

Date: 22 April 2020 Stock Price: $433.83 We take a look at the 1st quarter earnings release of their 2020 fiscal year of Netflix, the world's leading internet entertainment service group with over 182.86 million paid memberships (up by 15.77 million subscribers for the quarter). The group recorded revenue of $5.768 billion in the 1st quarter of their 2020 fiscal year.

|

|

About Netflix

Netflix is the world's leading internet entertainment service with over 151 million paid memberships in over 190 countries enjoying TV series, documentaries and feature films across a wide variety of genres and languages. Members can watch as much as they want, anytime, anywhere, on any internet-connected screen. Members can play, pause and resume watching, all without commercials or commitments.

Ten years ago a company like Netflix would have been given a vert slim chance of survival. Today its one of the largest companies in the world based on its market capital, and its also part of famed FAANG stocks. FAANG is a acronym for Facebook, Apple, Amazon, Netflix and Google.

Ten years ago a company like Netflix would have been given a vert slim chance of survival. Today its one of the largest companies in the world based on its market capital, and its also part of famed FAANG stocks. FAANG is a acronym for Facebook, Apple, Amazon, Netflix and Google.

The Witcher, one of Netflix's most popular shows right now

Overview of Netflix's 1st quarter 2020 earnings report

The data refers to the latest quarter unless specified otherwise:

Regional information for Netflix

The summary below shows the revenue earned for Netflix from various regions for the 1st quarter of their 2020 fiscal year (in $ thousands)

- Revenue: $5.767 billion (up from $4.520 billion from the same quarter of the previous year)

- Revenue increased by 27.6% over the last 12 months

- Cost of revenue: $3.599 billion (up from $2.870 billion for the same quarter of the previous year)

- Cost of revenue increased by 25.4% over the last 12 months

- Net income $709.067 million (up from $344.052 million for the same quarter of the previous year)

- Diluted earnings per share: $1.57 (up from $0.76 for the same quarter of the previous year)

- PE ratio of Netflix: 68.9

- Diluted weighted-average shares outstanding: 452.494 million (up from 451.922 million for the same quarter of the previous year)

- Cash and cash equivalents: $5.151 billion

- Cash and cash equivalents per share: $11.38

- Cash and cash equivalents makes up 2.6% of Netflix's market capital

- Cash and cash equivalents makes up 14.6% of Netflix's total assets

- Stockholders equity of Netflix: $8.409 billion

- Stockholders equity per share: $18.6

- Netflix is trading at 23.3 times its stockholders equity which is well outside the expected range of between 2 and 4 which most companies tend to trade at.

- For reference the S&P500 is trading at a price to book of 3.34. For more about the S&P500 read here

Regional information for Netflix

The summary below shows the revenue earned for Netflix from various regions for the 1st quarter of their 2020 fiscal year (in $ thousands)

- United States and Canada: $2 702 776

- Europe, Middle East and Africa: $1 723 474

- Latin America: $793 453

- Asia- Pacific: $483 660

Netflix' management commentary on the results and earnings guidance

Fellow shareholders, In our 20+ year history, we have never seen a future more uncertain or unsettling. The coronavirus has reached every corner of the world and, in the absence of a widespread treatment or vaccine, no one knows how or when this terrible crisis will end. What’s clear is the escalating human cost in terms of lost lives and lost jobs, with tens of millions of people now out of work. At Netflix, we’re acutely aware that we are fortunate to have a service that is even more meaningful to people confined at home, and which we can operate remotely with minimal disruption in the short to medium term. Like other home entertainment services, we’re seeing temporarily higher viewing and increased membership growth. In our case, this is offset by a sharply stronger US dollar, depressing our international revenue, resulting in revenue-as-forecast. We expect viewing to decline and membership growth to decelerate as home confinement ends, which we hope is soon. By helping people connect with stories they love, we are able to provide comfort and escape as well as a sense of community during this pandemic. So our focus has been on maintaining the quality of our service while our employees around the world adapt to working from home.

For the most part, this has gone smoothly. Our product teams, for example, have been relatively unaffected. As a precaution, we have temporarily reduced the number of product innovations we try, while continuing to release features that we know will add meaningful value for our members, such as improved parental controls. However, we have seen significant disruption when it comes to customer support and content production. On the customer support side, we’ve now fixed most of our work-from-home challenges. In addition, we’ve taken on another 2,000 agents (all working remotely), so our customer service levels are almost fully restored despite the increased deman

For the most part, this has gone smoothly. Our product teams, for example, have been relatively unaffected. As a precaution, we have temporarily reduced the number of product innovations we try, while continuing to release features that we know will add meaningful value for our members, such as improved parental controls. However, we have seen significant disruption when it comes to customer support and content production. On the customer support side, we’ve now fixed most of our work-from-home challenges. In addition, we’ve taken on another 2,000 agents (all working remotely), so our customer service levels are almost fully restored despite the increased deman

There are three primary effects on our financial performance from the crisis.

More on each of these three effects below. During the first two months of Q1, our membership growth was similar to the prior two years, including in UCAN. Then, with lockdown orders in many countries starting in March, many more households joined Netflix to enjoy entertainment. This timing of paid membership additions also affected our Q1’20 global streaming ARPU; this was the primary driver of the sequential decline in streaming ARPU as the revenue impact from these additions late in the quarter will be mostly felt in Q2’20 and beyond. Hopefully, progress against the virus will allow governments to lift the home confinement soon.

As that happens, we expect viewing and growth to decline. Our internal forecast and guidance is for 7.5 million global paid net additions in Q2. Given the uncertainty on home confinement timing, this is mostly guesswork. The actual Q2 numbers could end up well below or well above that, depending on many 3 factors including when people can go back to their social lives in various countries and how much people take a break from television after the lockdown. Some of the lockdown growth will turn out to be pull-forward from the multi-year organic growth trend, resulting in slower growth after the lockdown is lifted country-by-country. Intuitively, the person who didn’t join Netflix during the entire confinement is not likely to join soon after the confinement. Plus, last year we had new seasons of Money Heist and Stranger Things in Q3, which were not planned for this year’s Q3. Therefore, we currently guess that Q3’20 and Q4’20 will have lower net additions than last year due to these effects.

Second, partially due to the crisis, the US dollar has appreciated significantly, which creates a drag on international revenue growth. As an example, the price for our standard plan in Brazil is R$33, which used to be $8.5 last year but now is $6.5 based on April 2020 F/X rates, so we have a ~25% decline in US dollar average subscription price from Brazil, which offsets strong membership growth.

Third, we’ve paused most of our productions across the world in response to government lockdowns and guidance from local public health officials. In Q2, there is only a modest impact on our new releases, which is primarily language dubbing. No one knows how long it will be until we can safely restart physical production in various countries, and, once we can, what international travel will be possible, and how negotiations for various resources (e.g., talent, stages, and post-production) will play out.

The impact on us is less cash spending this year as some content projects are pushed out. We are working hard to complete the content we know our members want and we’re complementing this effort with additional licensed films and series. Our content competitors and suppliers will be impacted about as much as we are, in terms of new titles. Since we have a large library with thousands of titles for viewing and very strong recommendations, our member satisfaction may be less impacted than our peers’ by a shortage of new content, but it will take time to tell. We continue to target a 16% operating margin for the full year 2020, despite the extra costs in Q1.

As a reminder, more than half of our revenue is not denominated in US dollars and we don’t hedge our foreign exchange exposure. If the US dollar remains at these elevated levels (or strengthens further), we may target modestly slower growth in our annual operating margin progression next year. Given that lead time, we believe we can readjust our model to be appropriate in that new stronger US dollar world.

- First, our membership growth has temporarily accelerated due to home confinement.

- Second, our international revenue will be less than previously forecast due to the dollar rising sharply.

- Third, due to the production shutdown, some cash spending on content will be delayed, improving our free cash flow, and some title releases will be delayed, typically by a quarter.

More on each of these three effects below. During the first two months of Q1, our membership growth was similar to the prior two years, including in UCAN. Then, with lockdown orders in many countries starting in March, many more households joined Netflix to enjoy entertainment. This timing of paid membership additions also affected our Q1’20 global streaming ARPU; this was the primary driver of the sequential decline in streaming ARPU as the revenue impact from these additions late in the quarter will be mostly felt in Q2’20 and beyond. Hopefully, progress against the virus will allow governments to lift the home confinement soon.

As that happens, we expect viewing and growth to decline. Our internal forecast and guidance is for 7.5 million global paid net additions in Q2. Given the uncertainty on home confinement timing, this is mostly guesswork. The actual Q2 numbers could end up well below or well above that, depending on many 3 factors including when people can go back to their social lives in various countries and how much people take a break from television after the lockdown. Some of the lockdown growth will turn out to be pull-forward from the multi-year organic growth trend, resulting in slower growth after the lockdown is lifted country-by-country. Intuitively, the person who didn’t join Netflix during the entire confinement is not likely to join soon after the confinement. Plus, last year we had new seasons of Money Heist and Stranger Things in Q3, which were not planned for this year’s Q3. Therefore, we currently guess that Q3’20 and Q4’20 will have lower net additions than last year due to these effects.

Second, partially due to the crisis, the US dollar has appreciated significantly, which creates a drag on international revenue growth. As an example, the price for our standard plan in Brazil is R$33, which used to be $8.5 last year but now is $6.5 based on April 2020 F/X rates, so we have a ~25% decline in US dollar average subscription price from Brazil, which offsets strong membership growth.

Third, we’ve paused most of our productions across the world in response to government lockdowns and guidance from local public health officials. In Q2, there is only a modest impact on our new releases, which is primarily language dubbing. No one knows how long it will be until we can safely restart physical production in various countries, and, once we can, what international travel will be possible, and how negotiations for various resources (e.g., talent, stages, and post-production) will play out.

The impact on us is less cash spending this year as some content projects are pushed out. We are working hard to complete the content we know our members want and we’re complementing this effort with additional licensed films and series. Our content competitors and suppliers will be impacted about as much as we are, in terms of new titles. Since we have a large library with thousands of titles for viewing and very strong recommendations, our member satisfaction may be less impacted than our peers’ by a shortage of new content, but it will take time to tell. We continue to target a 16% operating margin for the full year 2020, despite the extra costs in Q1.

As a reminder, more than half of our revenue is not denominated in US dollars and we don’t hedge our foreign exchange exposure. If the US dollar remains at these elevated levels (or strengthens further), we may target modestly slower growth in our annual operating margin progression next year. Given that lead time, we believe we can readjust our model to be appropriate in that new stronger US dollar world.

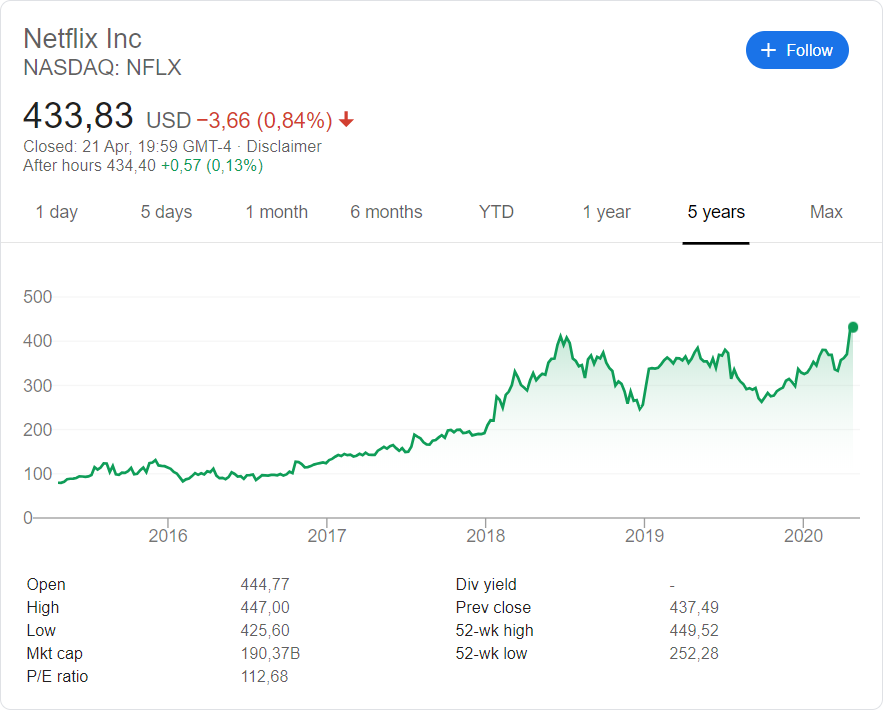

Netflix (NASDAQ: NFLX) stock price history

The image below, obtained from Google, shows the stock price history of Netflix (NASDAQ: NFLX) over the last 5 years. And it's been a exceptional time for Netflix (NASDAQ: NFLX). 5 years ago the stock was trading at around $80 and its currently trading at $433.83. That's a excellent return of 442% over the last 5 years.

The stock is however trading at very close to its 52 week high of $449.52 and is far far away from its 52 week low of $252.28, which to us is a clear indication that the short term sentiment and momentum of Netflix is very positive at this point in time. While stock market sentiment has been very negative due to the impact of Covid-19 and the ensuing lockdowns instituted due to it, this has benefitted Netflix greatly as more people stay at home they have seen a sharp increase in their revenues and subscriber numbers.

The stock is however trading at very close to its 52 week high of $449.52 and is far far away from its 52 week low of $252.28, which to us is a clear indication that the short term sentiment and momentum of Netflix is very positive at this point in time. While stock market sentiment has been very negative due to the impact of Covid-19 and the ensuing lockdowns instituted due to it, this has benefitted Netflix greatly as more people stay at home they have seen a sharp increase in their revenues and subscriber numbers.

Netflix (NASDAQ: NFLX) stock price history over the last 5 years.

Recent coverage of Netflix

Recent coverage of Netflix's latest results as obtained from Fool.com

Netflix Inc. revealed Tuesday that it added more than double the new subscribers it expected amid the spread of COVID-19 for record growth. Netflix NFLX, -0.83% reported the addition of 15.77 million paid subscribers globally in the first quarter. Netflix’s biggest quarter for paid net additions to its subscriber total previously was 9.6 million in the year-ago quarter, according to FactSet. Analysts were looking for global paid streaming subscriber additions of 8.22 million on average, according to FactSet, after Netflix projected 7 million new subscribers three months ago.

Netflix reported first-quarter earnings of $709 million, or $1.57 a share, compared with $344 million, or 76 cents a share, in the year-ago period. Revenue grew to $5.77 billion from $4.52 billion in the year-ago period. Analysts surveyed by FactSet had estimated $1.64 a share on revenue of $5.75 billion on average.

The first-quarter results, announced after the market’s close Tuesday, initially sent Netflix shares up more than 9% in after-hours trading, but the stock eventually calmed down to trade closer to the closing price of $433.83 and even dipping below that mark at times. The streaming service’s stock has shown more than just resilience during the coronavirus pandemic, closing at a record high of $437.49 on Monday before falling 0.8% in Tuesday’s trading session.

“During the first two months of the Q1, our membership growth was similar to the prior two years, including in [the U.S. and Canada],” Netflix executives said in a letter to shareholders. “Then, with lockdown orders in many countries starting in March, many more households joined Netflix to enjoy entertainment.” In a video interview late Tuesday, Netflix Chief Executive Reed Hastings referred to the quarter as a “pull-forward” for the rest of the fiscal year before paid net paid subscriptions cool the next few quarters. The company’s chief product officer, Greg Peters, quickly ruled out price increases in the foreseeable future.

Read the full article here

Netflix Inc. revealed Tuesday that it added more than double the new subscribers it expected amid the spread of COVID-19 for record growth. Netflix NFLX, -0.83% reported the addition of 15.77 million paid subscribers globally in the first quarter. Netflix’s biggest quarter for paid net additions to its subscriber total previously was 9.6 million in the year-ago quarter, according to FactSet. Analysts were looking for global paid streaming subscriber additions of 8.22 million on average, according to FactSet, after Netflix projected 7 million new subscribers three months ago.

Netflix reported first-quarter earnings of $709 million, or $1.57 a share, compared with $344 million, or 76 cents a share, in the year-ago period. Revenue grew to $5.77 billion from $4.52 billion in the year-ago period. Analysts surveyed by FactSet had estimated $1.64 a share on revenue of $5.75 billion on average.

The first-quarter results, announced after the market’s close Tuesday, initially sent Netflix shares up more than 9% in after-hours trading, but the stock eventually calmed down to trade closer to the closing price of $433.83 and even dipping below that mark at times. The streaming service’s stock has shown more than just resilience during the coronavirus pandemic, closing at a record high of $437.49 on Monday before falling 0.8% in Tuesday’s trading session.

“During the first two months of the Q1, our membership growth was similar to the prior two years, including in [the U.S. and Canada],” Netflix executives said in a letter to shareholders. “Then, with lockdown orders in many countries starting in March, many more households joined Netflix to enjoy entertainment.” In a video interview late Tuesday, Netflix Chief Executive Reed Hastings referred to the quarter as a “pull-forward” for the rest of the fiscal year before paid net paid subscriptions cool the next few quarters. The company’s chief product officer, Greg Peters, quickly ruled out price increases in the foreseeable future.

Read the full article here

Netflix (NASDAQ: NFLX) latest stock valuation

So based on the earnings report of Netflix (NASDAQ: NFLX) what do we value Netflix (NFLX) stock at? Based on the earnings report and the increased competition our valuation models sets a target (full value) price on Netflix of $319.20. (up strongly from our 4th quarter 2019 Netflix earnings report valuation). Based on our target price (full value price) we believe the stock of Netflix is overvalued.

We usually recommend that long term fundamental or value investors look to enter a stock at least 10% below our target (full value) price which in this case is $319,20. We therefore believe a good entry point into Netflix is $287.30 or below. Since the stock of Netflix is well above our recommended entry point we would not recommend buying into Netflix right now as we believe there is still a lot of hope and fairytales and butterflies built into their future earnings expectations with the group trading at a PE ratio of over 69

We usually recommend that long term fundamental or value investors look to enter a stock at least 10% below our target (full value) price which in this case is $319,20. We therefore believe a good entry point into Netflix is $287.30 or below. Since the stock of Netflix is well above our recommended entry point we would not recommend buying into Netflix right now as we believe there is still a lot of hope and fairytales and butterflies built into their future earnings expectations with the group trading at a PE ratio of over 69

Next earnings release for Netflix

It is expected that Netflix will release its 2nd quarter earnings report for their 2020 fiscal year towards the end of July 2020.