|

Related Topics

|

|

Category: Stock Market and Steel Dynamics

Date: 17 October 2019 Stock Price: $28.84 We take a look at the 3rd quarter earnings release of their 2019 fiscal year of Steel Dynamics, one of the largest steel producers and metal recyclers in the United States.

|

|

About Steel Dynamics

Steel Dynamics is one of the largest domestic steel producers and metals recyclers in the United States based on estimated annual steelmaking and metals recycling capability, with facilities located throughout the United States, and in Mexico. Steel Dynamics produces steel products, including hot roll, cold roll, and coated sheet steel, structural steel beams and shapes, rail, engineered special-bar-quality steel, cold finished steel, merchant bar products, specialty steel sections and steel joists and deck. In addition, the company produces liquid pig iron and processes and sells ferrous and nonferrous scrap.

Steel Dynamics Business Highlights

Overview of Steel Dynamics' latest earnings report

The numbers we are interested in (for the quarter):

- Net Sales $2.526 billion (down from $3.223 billion from the same quarter of the previous year)

- Sales decreased by -21.6% over the last 12 months

- Cost of Sales: $2.167 billion (up from $2.537 billion for the same quarter of the previous year)

- Cost of revenues decreased by -14.6% over the last 12 months

- Net income: $151.048 million (down from $398.375 million for the same quarter of the previous year)

- Diluted earnings per share: $0.69 (down from $1.69 for the same quarter of the previous year)

- Diluted weighted-average shares outstanding: 219.109 million (down from 235.649 million for the same quarter of the previous year)

- Dividend declared: $0.24 (up from $0.1875 for the same quarter of the previous year)

- Dividend yield: 3.3%

- Cash and cash equivalents: $1.146 billion

- Cash and cash equivalents per share: $5.23

- Cash and cash equivalents makes up 18.18% of Steel Dynamics' market capital

- Cash and cash equivalents makes up 14.42% of Steel Dynamics' total assets

- Accounts receivable: $986.946 million

- Accounts receivable makes up 12.42% of Steel Dynamics' total assets

- Stockholders equity: $3.901 billion

- Stockholders equity per Steel Dynamics stock: $17.80

- Steel Dynamics is trading at 1.62 times its stockholders equity per share which is outside the expected range of between 2 and 4 times that most firms tend to trade at.

- Cash generated from operations: $444.202 million

- Cash generated from operations per share: $2.03

Steel Dynamics' management commentary on the results and earnings guidance

FORT WAYNE, Ind., Oct. 16, 2019 /PRNewswire/ -- Steel Dynamics, Inc. (NASDAQ/GS: STLD) today announced third quarter 2019 financial results. The company reported third quarter 2019 net sales of $2.5 billion and net income of $151 million, or $0.69 per diluted share. Comparatively, prior year third quarter net sales were $3.2 billion, with net income of $398 million, or $1.69 per diluted share, which included charges related to fair value purchase accounting adjustments of $0.04 per diluted share and a tax benefit of $0.04 per diluted share. Sequential second quarter 2019 net sales were $2.8 billion, with net income of $194 million, or $0.87 per diluted share.

"Our third quarter 2019 consolidated operating income was $228 million and adjusted EBITDA $315 million," said Mark D. Millett, President and Chief Executive Officer. "The team delivered a solid third quarter performance in a challenging steel pricing environment, as average steel pricing declined in the quarter more than offsetting the benefit of lower scrap costs. Steel customer inventory destocking has subsided, and underlying domestic steel demand remains principally intact for the primary steel consuming sectors, with particular strength in construction, as supported by our continued seasonally strong steel fabrication backlog."

The company generated strong cash flow from operations of $444 million during the third quarter 2019 and increased liquidity to a record high $2.4 billion. The company paid cash dividends of $53 million and repurchased $115 million of its common stock during the third quarter 2019. "We are pleased by the recent rating upgrades to an investment grade credit by all three credit rating agencies," stated Theresa E. Wagler, Executive Vice President and Chief Financial Officer. "This is a natural progression of our growth, and recognition of our strong balance sheet profile and through-cycle free cash flow generation capability. Due to the strength of our liquidity profile, capital structure and free cash flow generating business model, we have the flexibility for continued growth and responsible shareholder distributions, while also being committed to maintaining investment grade credit metrics."

Third Quarter 2019 Comments

Third quarter 2019 operating income for the company's steel operations was $240 million, or 19 percent lower than sequential second quarter 2019 results. The sequential earnings decline was driven by lower realized product pricing and decreased shipments in the company's sheet steel operations, which more than offset the benefit of lower scrap costs in the quarter. The third quarter 2019 average external product selling price for the company's overall steel operations decreased $70 sequentially to $809 per ton. The average ferrous scrap cost per ton melted at the company's steel mills decreased $41 to $275 per ton.

The company's steel processing locations represented 17 percent of the shipment mix in the third quarter 2019, compared to 16 percent in the sequential quarter and 12 percent in the prior year third quarter. These locations use steel products as their primary raw material, and the associated steel procurement costs represented 17 percent of the steel operations cost of goods sold in the third quarter 2019, 18 percent in the sequential quarter, and 9 percent in the prior year third quarter.

Third quarter 2019 operating income from the company's metals recycling operations decreased to $3 million, compared to $11 million in the sequential second quarter, primarily as a result of the continued decline in aluminum demand and associated selling values. London Metal Exchange aluminum prices have declined more than 10 percent in 2019. Ferrous shipments and selling values also declined in the quarter, with prime scrap indices falling almost $30 per gross ton from July to September 2019.

Third quarter 2019 operating income from the company's steel fabrication operations was a strong $35 million, or 15 percent higher than sequential second quarter results. Earnings improved as higher shipments and lower raw material steel input costs resulted in expanded profit margins. The steel fabrication platform's order backlog remains strong, and customers remain optimistic concerning non-residential construction projects.

Outlook

"Based on domestic steel demand fundamentals, we are constructive regarding 2020 North American steel market dynamics," said Millett. "We believe North American steel consumption will experience modest growth and will be supported by further steel import reductions and the end of steel inventory destocking. We believe current trade actions could have a positive impact in further reducing unfairly traded steel imports into the United States, including coated flat roll steel, which could have a significant positive impact for Steel Dynamics, as we are the largest non-automotive flat roll steel coater in the United States.

"In combination with our existing and newly announced expansion initiatives, there are firm drivers in place for our continued growth. We are excited about our Sinton, Texas flat roll steel mill project, and the associated long-term value creation it will bring through geographic and value-added product diversification. This facility is designed to have product size and quality capabilities beyond that of existing electric-arc-furnace flat roll steel producers, competing even more effectively with the integrated steel model and foreign competition. We have targeted regional markets that represent over 27 million tons of relevant flat roll steel consumption, which includes the growing Mexican flat roll steel market. This facility is located and designed to have a meaningful competitive advantage in those regions. "We are competitively positioned and remain focused on delivering long-term shareholder value creation through organic and transactional growth opportunities," concluded Millett.

"Our third quarter 2019 consolidated operating income was $228 million and adjusted EBITDA $315 million," said Mark D. Millett, President and Chief Executive Officer. "The team delivered a solid third quarter performance in a challenging steel pricing environment, as average steel pricing declined in the quarter more than offsetting the benefit of lower scrap costs. Steel customer inventory destocking has subsided, and underlying domestic steel demand remains principally intact for the primary steel consuming sectors, with particular strength in construction, as supported by our continued seasonally strong steel fabrication backlog."

The company generated strong cash flow from operations of $444 million during the third quarter 2019 and increased liquidity to a record high $2.4 billion. The company paid cash dividends of $53 million and repurchased $115 million of its common stock during the third quarter 2019. "We are pleased by the recent rating upgrades to an investment grade credit by all three credit rating agencies," stated Theresa E. Wagler, Executive Vice President and Chief Financial Officer. "This is a natural progression of our growth, and recognition of our strong balance sheet profile and through-cycle free cash flow generation capability. Due to the strength of our liquidity profile, capital structure and free cash flow generating business model, we have the flexibility for continued growth and responsible shareholder distributions, while also being committed to maintaining investment grade credit metrics."

Third Quarter 2019 Comments

Third quarter 2019 operating income for the company's steel operations was $240 million, or 19 percent lower than sequential second quarter 2019 results. The sequential earnings decline was driven by lower realized product pricing and decreased shipments in the company's sheet steel operations, which more than offset the benefit of lower scrap costs in the quarter. The third quarter 2019 average external product selling price for the company's overall steel operations decreased $70 sequentially to $809 per ton. The average ferrous scrap cost per ton melted at the company's steel mills decreased $41 to $275 per ton.

The company's steel processing locations represented 17 percent of the shipment mix in the third quarter 2019, compared to 16 percent in the sequential quarter and 12 percent in the prior year third quarter. These locations use steel products as their primary raw material, and the associated steel procurement costs represented 17 percent of the steel operations cost of goods sold in the third quarter 2019, 18 percent in the sequential quarter, and 9 percent in the prior year third quarter.

Third quarter 2019 operating income from the company's metals recycling operations decreased to $3 million, compared to $11 million in the sequential second quarter, primarily as a result of the continued decline in aluminum demand and associated selling values. London Metal Exchange aluminum prices have declined more than 10 percent in 2019. Ferrous shipments and selling values also declined in the quarter, with prime scrap indices falling almost $30 per gross ton from July to September 2019.

Third quarter 2019 operating income from the company's steel fabrication operations was a strong $35 million, or 15 percent higher than sequential second quarter results. Earnings improved as higher shipments and lower raw material steel input costs resulted in expanded profit margins. The steel fabrication platform's order backlog remains strong, and customers remain optimistic concerning non-residential construction projects.

Outlook

"Based on domestic steel demand fundamentals, we are constructive regarding 2020 North American steel market dynamics," said Millett. "We believe North American steel consumption will experience modest growth and will be supported by further steel import reductions and the end of steel inventory destocking. We believe current trade actions could have a positive impact in further reducing unfairly traded steel imports into the United States, including coated flat roll steel, which could have a significant positive impact for Steel Dynamics, as we are the largest non-automotive flat roll steel coater in the United States.

"In combination with our existing and newly announced expansion initiatives, there are firm drivers in place for our continued growth. We are excited about our Sinton, Texas flat roll steel mill project, and the associated long-term value creation it will bring through geographic and value-added product diversification. This facility is designed to have product size and quality capabilities beyond that of existing electric-arc-furnace flat roll steel producers, competing even more effectively with the integrated steel model and foreign competition. We have targeted regional markets that represent over 27 million tons of relevant flat roll steel consumption, which includes the growing Mexican flat roll steel market. This facility is located and designed to have a meaningful competitive advantage in those regions. "We are competitively positioned and remain focused on delivering long-term shareholder value creation through organic and transactional growth opportunities," concluded Millett.

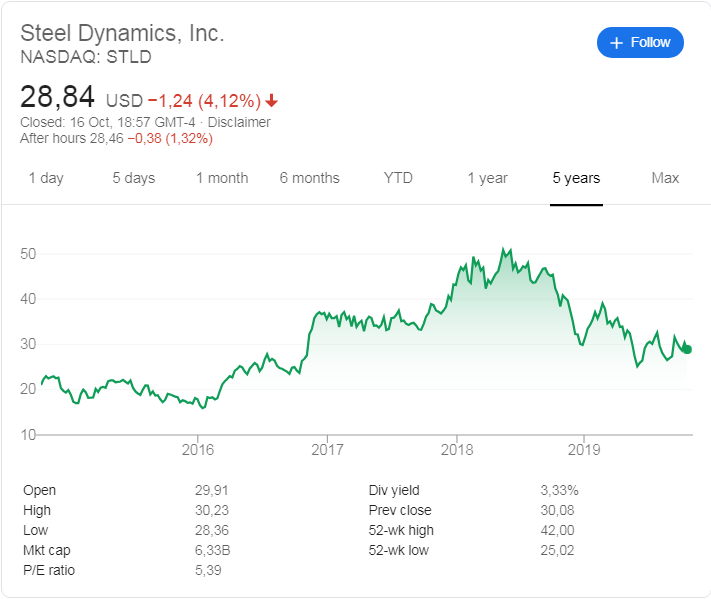

Steel Dynamics (NASDAQ:STLD) stock price history

The image below, obtained from Google, shows the stock price history of Steel Dynamics (NASDAQ: STLD) for the last 5 years. And it's been a decent time for Steel Dynamics stockholders. 5 years ago Steel Dynamics was trading at around $21.06 and its currently trading at $28.84. So the stock has grown by 36.9% over the last 5 years.

While its not bad the opportunity cost of holding the stock is pretty high when one looks as the strong growth over the last 5 years some of the othe stock we valued recently showed, with a large number of companies having grown by well over 100% over a 5 year period, for example Netflix that increased by over 300% over the last 5 years. Steel Dynamics is trading at a lot closer to its 52 week low of $25.02 than it is to its 52 week high of $42.00, which to us is a clear indication that the short term sentiment and momentum of the stock of Steel Dynamics is negative.

While its not bad the opportunity cost of holding the stock is pretty high when one looks as the strong growth over the last 5 years some of the othe stock we valued recently showed, with a large number of companies having grown by well over 100% over a 5 year period, for example Netflix that increased by over 300% over the last 5 years. Steel Dynamics is trading at a lot closer to its 52 week low of $25.02 than it is to its 52 week high of $42.00, which to us is a clear indication that the short term sentiment and momentum of the stock of Steel Dynamics is negative.

Steel Dynamics (NASDAQ: STLD) stock price history over the last 5 years.

Recent coverage of Steel Dynamics

The extract below discusses Steel Dynamics at more detail, as obtained from Zacks.

Steel Dynamics (STLD - Free Report) came out with quarterly earnings of $0.69 per share, missing the Zacks Consensus Estimate of $0.70 per share. This compares to earnings of $1.69 per share a year ago. These figures are adjusted for non-recurring items. This quarterly report represents an earnings surprise of -1.43%. A quarter ago, it was expected that this steel producer and metals recycler would post earnings of $0.89 per share when it actually produced earnings of $0.87, delivering a surprise of -2.25%.

Over the last four quarters, the company has surpassed consensus EPS estimates just once. Steel Dynamics, which belongs to the Zacks Steel - Producers industry, posted revenues of $2.53 billion for the quarter ended September 2019, missing the Zacks Consensus Estimate by 3.51%. This compares to year-ago revenues of $3.22 billion. The company has topped consensus revenue estimates two times over the last four quarters.

Read the full article here

Steel Dynamics (STLD - Free Report) came out with quarterly earnings of $0.69 per share, missing the Zacks Consensus Estimate of $0.70 per share. This compares to earnings of $1.69 per share a year ago. These figures are adjusted for non-recurring items. This quarterly report represents an earnings surprise of -1.43%. A quarter ago, it was expected that this steel producer and metals recycler would post earnings of $0.89 per share when it actually produced earnings of $0.87, delivering a surprise of -2.25%.

Over the last four quarters, the company has surpassed consensus EPS estimates just once. Steel Dynamics, which belongs to the Zacks Steel - Producers industry, posted revenues of $2.53 billion for the quarter ended September 2019, missing the Zacks Consensus Estimate by 3.51%. This compares to year-ago revenues of $3.22 billion. The company has topped consensus revenue estimates two times over the last four quarters.

Read the full article here

Steel Dynamics (NASDAQ: STLD) latest stock valuation

So based on the 3rd quarter 2019 earnings report of Steel Dynamics (NASDAQ:STLD) and the latest earnings guidance provided what do we value Steel Dynamics (STLD) stock at? Based on the earnings reported and the fiscal guidance provided by the group our valuation model provides a target (full value) price for Steel Dynamics at $41 a stock. We therefore believe the stock of Steel Dynamics is undervalued.

In our 2nd quarter earnings review of Steel Dynamics we valued the group at just below $37, thus our valuation of the group has increased, largely due to their stronger balance sheet.

We suggest long term fundamental and value investors look to enter the stock at least 10% below our target price of $41. Therefore we believe a good entry point into Steel Dynamics is at $36.90 or below. Since the stock of Steel Dynamics is trading at well below our target (full value) price we rate Steel Dynamics as a buy.

Our valuation takes into account a slow down in US economic activity as well as potential trade war negative effects that could affect Steel Dynamics in the medium term.

In our 2nd quarter earnings review of Steel Dynamics we valued the group at just below $37, thus our valuation of the group has increased, largely due to their stronger balance sheet.

We suggest long term fundamental and value investors look to enter the stock at least 10% below our target price of $41. Therefore we believe a good entry point into Steel Dynamics is at $36.90 or below. Since the stock of Steel Dynamics is trading at well below our target (full value) price we rate Steel Dynamics as a buy.

Our valuation takes into account a slow down in US economic activity as well as potential trade war negative effects that could affect Steel Dynamics in the medium term.

Next earnings release of Steel Dynamics

It is expected that the 4th quarter earnings release of Steel Dynamics will be released in late January 2020.