|

Related Topics

|

|

Category: Stock Market and Lululemon

Date: 7 July 2020 Stock Price of Lululemon: $314.35 We take a look at a press release from Lululemon in which the group announced that it is to acquire Mirror, an in-home fitness company for $500 million.

|

|

- Calvin McDonald, Chief Executive Officer commented: In 2019, we detailed our vision to be the experiential brand that ignites a community of people living the sweatlife through sweat, grow and connect. The acquisition of MIRROR is an exciting opportunity to build upon that vision, enhance our digital and interactive capabilities, and deepen our roots in the sweatlife "

About Lululemon

lululemon athletica inc. (NASDAQ:LULU) is a healthy lifestyle inspired athletic apparel company for yoga, running, training, and most other sweaty pursuits, creating transformational products and experiences which enable people to live a life they love. Setting the bar in technical fabrics and functional designs, lululemon works with yogis and athletes in local communities for continuous research and product feedback. A few quick facts about Lululemon

Read more about Lululemon here

- Lululemon is listed on the Nasdaq under share code ticker: LULU

- Lululemon has 491 company operated retail outlets

- Lululemon employs roughly 19 000 people

Read more about Lululemon here

Lululemon store entrance

Lululemon press release announcing the acquisition of Mirror

VANCOUVER, British Columbia--(BUSINESS WIRE)--Jun. 29, 2020-- lululemon athletica inc. (NASDAQ:LULU) today announced that it has entered into a definitive agreement to acquire MIRROR, a leading in-home fitness company that created an interactive workout platform that features live and on-demand classes, for a purchase price of $500 million.

With its best-in-class content and versatile platform, MIRROR positions lululemon to accelerate its vision and build upon an ecosystem that will fuel the Company’s Power of Three growth plan, which includes driving the business through omni guest experiences. MIRROR will bolster the company’s digital sweatlife offerings and bring immersive and personalized in-home sweat, and mindfulness solutions to new and existing lululemon guests.

Calvin McDonald, Chief Executive Officer, commented, “In 2019, we detailed our vision to be the experiential brand that ignites a community of people living the sweatlife through sweat, grow and connect. The acquisition of MIRROR is an exciting opportunity to build upon that vision, enhance our digital and interactive capabilities, and deepen our roots in the sweatlife. We look forward to learning from and working with Brynn Putnam and the team at MIRROR to accelerate the growth of personalized in-home fitness.”

MIRROR offers weekly live classes and thousands of on-demand workouts as well as immersive one-on-one personal training. MIRROR has seen rapid growth and strong engagement since it launched in 2018 as demand for in-home fitness offerings continue to increase significantly.

With its best-in-class content and versatile platform, MIRROR positions lululemon to accelerate its vision and build upon an ecosystem that will fuel the Company’s Power of Three growth plan, which includes driving the business through omni guest experiences. MIRROR will bolster the company’s digital sweatlife offerings and bring immersive and personalized in-home sweat, and mindfulness solutions to new and existing lululemon guests.

Calvin McDonald, Chief Executive Officer, commented, “In 2019, we detailed our vision to be the experiential brand that ignites a community of people living the sweatlife through sweat, grow and connect. The acquisition of MIRROR is an exciting opportunity to build upon that vision, enhance our digital and interactive capabilities, and deepen our roots in the sweatlife. We look forward to learning from and working with Brynn Putnam and the team at MIRROR to accelerate the growth of personalized in-home fitness.”

MIRROR offers weekly live classes and thousands of on-demand workouts as well as immersive one-on-one personal training. MIRROR has seen rapid growth and strong engagement since it launched in 2018 as demand for in-home fitness offerings continue to increase significantly.

This transaction builds on a successful partnership between the two companies, which began in mid-2019 with an initial investment in MIRROR by lululemon, and also includes a content partnership which brought sweat and meditation classes to the MIRROR platform by lululemon’s Global Ambassadors. This acquisition will further expand the content creation partnership between the two brands and will help lululemon, MIRROR and lululemon Ambassadors reach new guests.

Ms. Putnam, founder and chief executive officer of MIRROR, and a former lululemon Ambassador said, “We are thrilled to officially become a part of the lululemon family. As part of lululemon, MIRROR can further strengthen its position and accelerate its growth by leveraging lululemon’s deep relationships with its guests, ambassadors and communities, as well as the company’s infrastructure, including its store network and ecommerce channels, to acquire new users.”

The purchase price is expected to be paid from the company’s primary sources of liquidity, which include over $800 million in cash, its existing $400 million revolving credit facility, and a new one-year, $300 million revolving credit facility.

Following completion of the transaction, MIRROR will operate as a standalone company within lululemon and Ms. Putnam will continue as MIRROR’s chief executive officer, reporting to Mr. McDonald. The transaction is subject to customary closing conditions and is expected to close in the second quarter of fiscal 2020.

Ms. Putnam, founder and chief executive officer of MIRROR, and a former lululemon Ambassador said, “We are thrilled to officially become a part of the lululemon family. As part of lululemon, MIRROR can further strengthen its position and accelerate its growth by leveraging lululemon’s deep relationships with its guests, ambassadors and communities, as well as the company’s infrastructure, including its store network and ecommerce channels, to acquire new users.”

The purchase price is expected to be paid from the company’s primary sources of liquidity, which include over $800 million in cash, its existing $400 million revolving credit facility, and a new one-year, $300 million revolving credit facility.

Following completion of the transaction, MIRROR will operate as a standalone company within lululemon and Ms. Putnam will continue as MIRROR’s chief executive officer, reporting to Mr. McDonald. The transaction is subject to customary closing conditions and is expected to close in the second quarter of fiscal 2020.

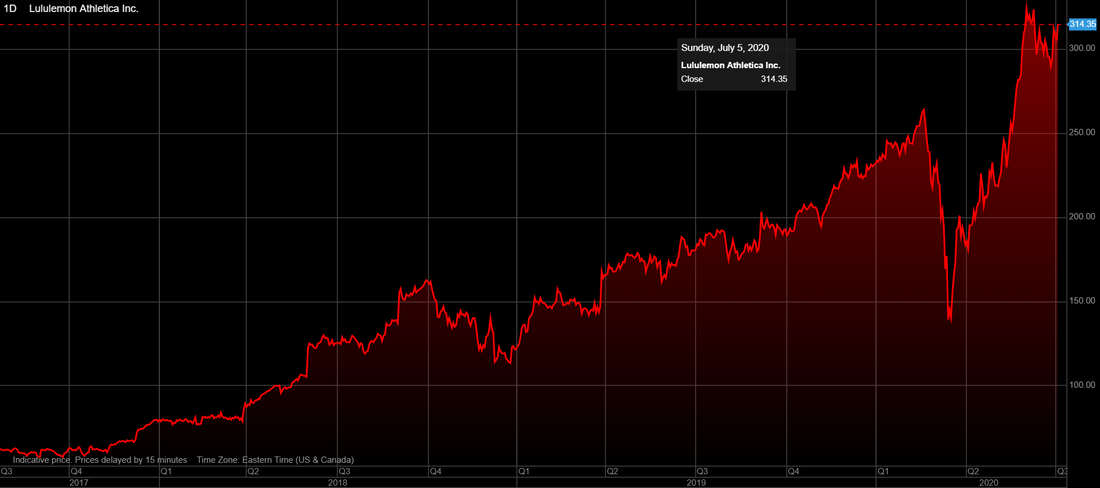

Lululemon (LULU) stock price history over the last 3 years

The image below shows the stock price history of Lululemon for the last 3 years. And its been a fantastic time for LULU stockholders. Over the last 3 years the stock of Lululemon has increased by 406.85%. No investor in the world would say no to those kinds of returns. But as we discussed in our last stock valuation of Lululemon we do believe the group's stock is hopelessly overvalued and would not recommend buying their stock at these elevated levels.

Lululemon (NASDAQ: LULU) stock price history over the last 3years

Recent coverage of Lululemon

The extract below covers the latest regarding Lululemon as obtained from TheStreet.com (10 June 2020)

What to do with a name like Lululemon Athletica (LULU) . I have written about this company on multiple occasions. I have traded it more often than I have written on it. The trades, owing to nothing other than this being a good stock in a bull market, were profitable. I think every time. I take no credit. I just rode the wave. Except this time. You'll recall that as planet earth burned back in February, and well into March, that I was quite open about the need to narrow portfolios going into a deep contraction in economic activity. LULU did not make that cut. Not a shot at LULU, a lot of good firms did not make that cut. It was not until early April when I felt that technically, a change in trend had been confirmed, and quite honestly, I was methodical in putting the risk back on. As a result of this lack of aggression, LULU is the one (one of the ones) that got away. Q1 earnings are due tomorrow (Thursday) after the closing bell. The shares have moved well beyond the February highs. Short question. Is there still some money to be made here. Let you know when it hits the P/L, but sure, we can give this a go. Let's open the door to see what we can see.

Thursday Afternoon

Wall Street consensus for what Lululemon Athletica reports tomorrow night is for EPS of $0.23. Fact is though that 32 analysts cover this name and that consensus is really more like an average. As far as I can tell, the high projection across the group is for EPS of $0.55, while the lowest is down around -$0.15. The broader view for revenue generation is for roughly $683 million, but again, there is at least one analyst all the way up at $811 million, and another way down at $552 million. I other words... at least these guys aren't copying each other's work.

That average revenue number, if realized, would represent an outright contraction in sales year over year of -12.6%. This would break a streak of eight consecutive quarters of 20% growth or more. Acceptable for a business that largely sells apparel in the age of Covid-19, while gyms everywhere have been closed for months? I think so, if temporary.

Brian Nagel, a very highly rated analyst (Oppenheimer) whose work I respect, admits that valuation at these levels may be a bit stretched, but also feels that the firm is positioned well for an economy coming out of a public health crisis. Nagel has an outperform rating on LULU and has now increased his price target to $370. He's not alone. A number of analysts have opined ahead of these earnings. Some of them are also highly rated. This one caught my eye. On Tuesday, just yesterday. If you've read me for a while, then you know that my ears perk up when I hear something, anything from Morgan Stanley's Kimberly Greenberger. She maintained her "hold" rating on LULU going into the numbers, with a price target of $296. That's down about $30 from the last sale. Hmm, what's a guy trying to make a couple of bucks, who does like the name and the business, to do?

Read the original article here

What to do with a name like Lululemon Athletica (LULU) . I have written about this company on multiple occasions. I have traded it more often than I have written on it. The trades, owing to nothing other than this being a good stock in a bull market, were profitable. I think every time. I take no credit. I just rode the wave. Except this time. You'll recall that as planet earth burned back in February, and well into March, that I was quite open about the need to narrow portfolios going into a deep contraction in economic activity. LULU did not make that cut. Not a shot at LULU, a lot of good firms did not make that cut. It was not until early April when I felt that technically, a change in trend had been confirmed, and quite honestly, I was methodical in putting the risk back on. As a result of this lack of aggression, LULU is the one (one of the ones) that got away. Q1 earnings are due tomorrow (Thursday) after the closing bell. The shares have moved well beyond the February highs. Short question. Is there still some money to be made here. Let you know when it hits the P/L, but sure, we can give this a go. Let's open the door to see what we can see.

Thursday Afternoon

Wall Street consensus for what Lululemon Athletica reports tomorrow night is for EPS of $0.23. Fact is though that 32 analysts cover this name and that consensus is really more like an average. As far as I can tell, the high projection across the group is for EPS of $0.55, while the lowest is down around -$0.15. The broader view for revenue generation is for roughly $683 million, but again, there is at least one analyst all the way up at $811 million, and another way down at $552 million. I other words... at least these guys aren't copying each other's work.

That average revenue number, if realized, would represent an outright contraction in sales year over year of -12.6%. This would break a streak of eight consecutive quarters of 20% growth or more. Acceptable for a business that largely sells apparel in the age of Covid-19, while gyms everywhere have been closed for months? I think so, if temporary.

Brian Nagel, a very highly rated analyst (Oppenheimer) whose work I respect, admits that valuation at these levels may be a bit stretched, but also feels that the firm is positioned well for an economy coming out of a public health crisis. Nagel has an outperform rating on LULU and has now increased his price target to $370. He's not alone. A number of analysts have opined ahead of these earnings. Some of them are also highly rated. This one caught my eye. On Tuesday, just yesterday. If you've read me for a while, then you know that my ears perk up when I hear something, anything from Morgan Stanley's Kimberly Greenberger. She maintained her "hold" rating on LULU going into the numbers, with a price target of $296. That's down about $30 from the last sale. Hmm, what's a guy trying to make a couple of bucks, who does like the name and the business, to do?

Read the original article here

Lululemon store in a mall

Lululemon (NASDAQ: LULU) latest stock valuation

Based on Lululemon's 1st quarter 2020 earnings report from Lululemon what do we value their stock at? Based on Lululemon's earnings reported our valuation model provides a target price (full value price) of $148.10 a Lululemon stock (down slightly from our 4th quarter 2019 earnings report valuation of Lululemon).

We therefore believe that the stock of Lululemon is overvalued. We usually recommend that long term fundamental and value investors look to enter a stock at least 10% below our target price which in this case is $148.10. A good entry point into Lululemon would therefore be at $133.30 or below. Since the stock of Lululemon is trading at well above our target price we rate the stock of Lululemon as avoid.

We expect it to pull back strongly from current levels to levels closer to our target price in coming weeks and months.

We therefore believe that the stock of Lululemon is overvalued. We usually recommend that long term fundamental and value investors look to enter a stock at least 10% below our target price which in this case is $148.10. A good entry point into Lululemon would therefore be at $133.30 or below. Since the stock of Lululemon is trading at well above our target price we rate the stock of Lululemon as avoid.

We expect it to pull back strongly from current levels to levels closer to our target price in coming weeks and months.

Next earnings release of Lululemon

It is expected that Lululemon will release their 2nd quarter 2020 earnings report in early September 2020