|

Related Topics

|

|

Category: Stock Market and Netflix (NFLX)

Date: 21 October 2020 Stock Price of Netflix: $525.42 We take a look at the 3rd quarter earnings release of their 2020 fiscal year of Netflix, the world's leading internet entertainment service group with over 195 million paid memberships (up by 2.2 million subscribers for the latest quarter). The group recorded revenue of $6.436 billion in the 3rd quarter of their 2020 fiscal year and net income came in at $790 million

|

|

We are making good and careful progress returning to production, particularly in EMEA and APAC, but also across much of LATAM and UCAN. We’ve restarted production on some of our biggest titles including season four of Stranger Things, action film Red Notice (starring Dwayne Johnson, Gal Gadot and Ryan Reynolds) and The Witcher season two."

About Netflix (NFLX)

Netflix is the world's leading internet entertainment service with over 151 million paid memberships in over 190 countries enjoying TV series, documentaries and feature films across a wide variety of genres and languages. Members can watch as much as they want, anytime, anywhere, on any internet-connected screen. Members can play, pause and resume watching, all without commercials or commitments.

Ten years ago a company like Netflix would have been given a very slim chance of survival. Today its one of the largest companies in the world based on its market capital, and its also part of famed FAANG stocks. FAANG is a acronym for Facebook, Apple, Amazon, Netflix and Google.

Ten years ago a company like Netflix would have been given a very slim chance of survival. Today its one of the largest companies in the world based on its market capital, and its also part of famed FAANG stocks. FAANG is a acronym for Facebook, Apple, Amazon, Netflix and Google.

Enola Holmes the Netflix movie has been watched over 76 million times

Overview of Netflix's 3rd quarter 2020 earnings report

The data refers to the latest quarter unless specified otherwise:

Regional information for Netflix

The summary below shows the revenue earned for Netflix from various regions for the 3rd quarter of their 2020 fiscal year (in $ billions)

- Revenue: $6.435 billion (up from $5.244 billion from the same quarter of the previous year)

- Revenue increased by 22.7% over the last 12 months

- Cost of revenue: $3.867 billion (up from $3.097 billion for the same quarter of the previous year)

- Cost of revenue increased by 24.9% over the last 12 months

- Net income $789.9 million (up from $665.2 million for the same quarter of the previous year)

- Diluted earnings per share: $1.74 (up from $1.47 for the same quarter of the previous year)

- PE ratio of Netflix: 84.7

- Diluted weighted-average shares outstanding: 455.088 million (up from 451.552 million for the same quarter of the previous year)

- Cash and cash equivalents: $8.392 billion

- Cash and cash equivalents per share: $18.44

- Cash and cash equivalents makes up 3.5% of Netflix's market capital

- Cash and cash equivalents makes up 21.7% of Netflix's total assets

- Stockholders equity of Netflix: $10.333 billion

- Stockholders equity per share: $22.70

- Netflix is trading at 23.1 times its stockholders equity which is well outside the expected range of between 2 and 4 which most companies tend to trade at.

- For reference the S&P500 is trading at a price to book of 3.7

Regional information for Netflix

The summary below shows the revenue earned for Netflix from various regions for the 3rd quarter of their 2020 fiscal year (in $ billions)

- United States and Canada: 2.933

- Europe, Middle East and Africa: 2.019

- Latin America: 0.789

- Asia- Pacific: 0.634

Netflix' management commentary on their 3rd quarter 2020 earnings

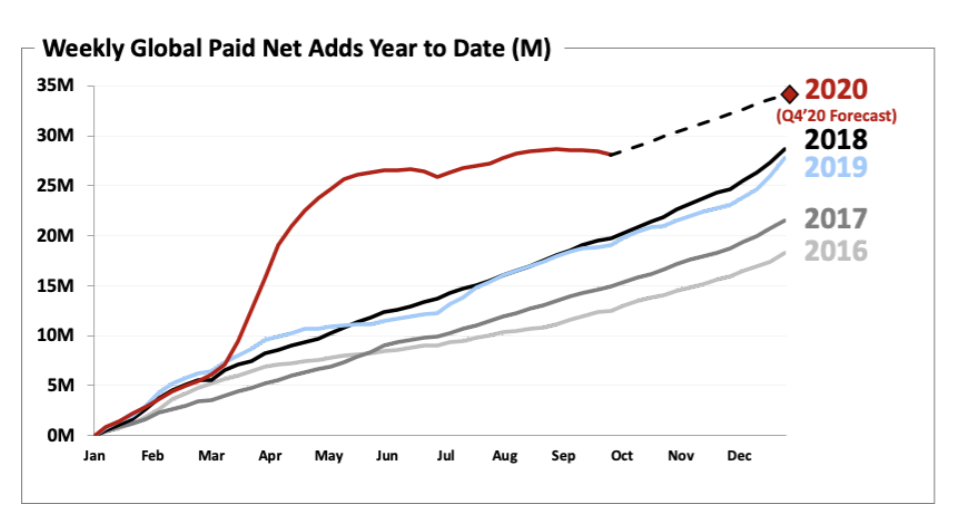

As we expected, growth has slowed with 2.2m paid net adds in Q3 vs. 6.8m in Q3’19. We think this is primarily due to our record first half results and the pull-forward effect we described in our April and July letters. In the first nine months of 2020, we added 28.1m paid memberships, which exceeds the 27.8m that we added for all of 2019. In these challenging times, we’re dedicated to serving our members.

Q3 average streaming paid memberships rose 25%, while streaming ARPU decreased 1.6% year over year. Excluding a foreign exchange (F/X) impact of -$158m, streaming ARPU increased 1% vs. prior year. Revenue was 2% above our beginning-of-quarter guidance primarily due to slightly higher than expected ARPU (favorable plan mix in our UCAN, LATAM and APAC regions plus intra-quarter appreciation in the Euro and British pound which helped lift EMEA ARPU). As a result, operating margin of 20% (up 170bps year over year) exceeded our guidance forecast as well. EPS of $1.74 vs. $1.47 a year ago included a $249m non-cash unrealized loss from F/X remeasurement on our Euro denominated debt, which accounted for the variance with our EPS guidance. We added 2.2m net memberships in Q3, compared with our 2.5m guidance. Retention remains healthy and engagement per member household was up solidly year over year in Q3’20. As a reminder, our guidance is our internal forecast and we strive for accuracy. That means in some quarters our results will be high relative to our guidance forecast and, in others, it will be low.

Q3 average streaming paid memberships rose 25%, while streaming ARPU decreased 1.6% year over year. Excluding a foreign exchange (F/X) impact of -$158m, streaming ARPU increased 1% vs. prior year. Revenue was 2% above our beginning-of-quarter guidance primarily due to slightly higher than expected ARPU (favorable plan mix in our UCAN, LATAM and APAC regions plus intra-quarter appreciation in the Euro and British pound which helped lift EMEA ARPU). As a result, operating margin of 20% (up 170bps year over year) exceeded our guidance forecast as well. EPS of $1.74 vs. $1.47 a year ago included a $249m non-cash unrealized loss from F/X remeasurement on our Euro denominated debt, which accounted for the variance with our EPS guidance. We added 2.2m net memberships in Q3, compared with our 2.5m guidance. Retention remains healthy and engagement per member household was up solidly year over year in Q3’20. As a reminder, our guidance is our internal forecast and we strive for accuracy. That means in some quarters our results will be high relative to our guidance forecast and, in others, it will be low.

Content

We are making good and careful progress returning to production, particularly in EMEA and APAC, but also across much of LATAM and UCAN. We’ve restarted production on some of our biggest titles including season four of Stranger Things, action film Red Notice (starring Dwayne Johnson, Gal Gadot and Ryan Reynolds) and The Witcher season two. Since the almost-global shutdown of production back in mid-March, we have already completed principal photography on 50+ productions and, while the course and impact of C-19 remains unpredictable, we’re optimistic we will complete shooting on over 150 other productions by year-end. For our 2021 slate, we continue to expect the number of Netflix originals launched on our service to be up year over year in each quarter of 2021 and we’re confident that we’ll have an exciting range of programming for our members, particularly relative to other entertainment service options. As discussed last quarter, some of our most popular returning titles are expected to launch in the second half of next year.

This past quarter, the breadth of our programming was demonstrated with standout titles across many genres. In English language series, we debuted new seasons of The Umbrella Academy and Lucifer; 43m and 38m member households chose to watch these titles in the first 28 days, respectively. In mid-September, we also premiered Ryan Murphy’s Ratched, a thriller based on the character from One Flew Over the Cuckoo’s Nest.

In its first four weeks, 48m member households chose to watch Ratched. Our #1 and #2 most watched documentary feature films ever were released in Q3. American Murder: The Family Next Door is projected to have 52m members households choose the title in its first 28 days and The Social Dilemma had 38m in its first 28 days. We continue to invest heavily in local language content because we believe that great stories are universal: they can come from anywhere and be loved everywhere. Season one of the Mexican telenovela Oscuro Deseo (Dark Desire) was our biggest local language original globally this quarter. Our slate of Korean dramas continue to travel well throughout APAC and beyond, while anime is another category of content with fans all over the world. Another example of our content traveling around the globe is our non-fiction series Indian Matchmaking, which was watched by a quarter of our members in India and millions of members outside of India in its first four weeks.

Original film continues to be an area of opportunity for us and we had several big hits in Q3. Action thriller The Old Guard (starring Charlize Theron and directed by Gina Prince-Bythewood) was our most popular title of the quarter with 78m member households choosing to watch in its first four weeks. Our romantic comedy The Kissing Booth 2 received strong reception (66m member households chose to watch in the first 28 days), while action film Project Power (starring Jamie Foxx) was also very popular (75m member households chose to watch in the first four weeks). Late in September, we debuted Enola Holmes, starring Millie Bobby Brown and Henry Cavill as her famed detective brother. We estimate 76m member households will have chosen this film in the first 28 days. Our content successes highlight our ability to tap into our global audience of nearly 200m members and underscore the notion that content is discovered on Netflix. This applies not only to Netflix originals, but also to second run programming, like Schitt’s Creek and earlier seasons of Lucifer, both of which are very popular with our members. The latest example is Cobra Kai (based on The Karate Kid films), which originally debuted on YouTube’s subscription service in May 2018 and recently launched on Netflix on August 28. In its first four weeks of release on Netflix, 50m member households chose to watch season one, dramatically expanding its audience

We are making good and careful progress returning to production, particularly in EMEA and APAC, but also across much of LATAM and UCAN. We’ve restarted production on some of our biggest titles including season four of Stranger Things, action film Red Notice (starring Dwayne Johnson, Gal Gadot and Ryan Reynolds) and The Witcher season two. Since the almost-global shutdown of production back in mid-March, we have already completed principal photography on 50+ productions and, while the course and impact of C-19 remains unpredictable, we’re optimistic we will complete shooting on over 150 other productions by year-end. For our 2021 slate, we continue to expect the number of Netflix originals launched on our service to be up year over year in each quarter of 2021 and we’re confident that we’ll have an exciting range of programming for our members, particularly relative to other entertainment service options. As discussed last quarter, some of our most popular returning titles are expected to launch in the second half of next year.

This past quarter, the breadth of our programming was demonstrated with standout titles across many genres. In English language series, we debuted new seasons of The Umbrella Academy and Lucifer; 43m and 38m member households chose to watch these titles in the first 28 days, respectively. In mid-September, we also premiered Ryan Murphy’s Ratched, a thriller based on the character from One Flew Over the Cuckoo’s Nest.

In its first four weeks, 48m member households chose to watch Ratched. Our #1 and #2 most watched documentary feature films ever were released in Q3. American Murder: The Family Next Door is projected to have 52m members households choose the title in its first 28 days and The Social Dilemma had 38m in its first 28 days. We continue to invest heavily in local language content because we believe that great stories are universal: they can come from anywhere and be loved everywhere. Season one of the Mexican telenovela Oscuro Deseo (Dark Desire) was our biggest local language original globally this quarter. Our slate of Korean dramas continue to travel well throughout APAC and beyond, while anime is another category of content with fans all over the world. Another example of our content traveling around the globe is our non-fiction series Indian Matchmaking, which was watched by a quarter of our members in India and millions of members outside of India in its first four weeks.

Original film continues to be an area of opportunity for us and we had several big hits in Q3. Action thriller The Old Guard (starring Charlize Theron and directed by Gina Prince-Bythewood) was our most popular title of the quarter with 78m member households choosing to watch in its first four weeks. Our romantic comedy The Kissing Booth 2 received strong reception (66m member households chose to watch in the first 28 days), while action film Project Power (starring Jamie Foxx) was also very popular (75m member households chose to watch in the first four weeks). Late in September, we debuted Enola Holmes, starring Millie Bobby Brown and Henry Cavill as her famed detective brother. We estimate 76m member households will have chosen this film in the first 28 days. Our content successes highlight our ability to tap into our global audience of nearly 200m members and underscore the notion that content is discovered on Netflix. This applies not only to Netflix originals, but also to second run programming, like Schitt’s Creek and earlier seasons of Lucifer, both of which are very popular with our members. The latest example is Cobra Kai (based on The Karate Kid films), which originally debuted on YouTube’s subscription service in May 2018 and recently launched on Netflix on August 28. In its first four weeks of release on Netflix, 50m member households chose to watch season one, dramatically expanding its audience

Netflix weekly net paid additions to subscriber numbers

Product and Partnerships

We strive to be a global entertainment service that can satisfy the needs of members all over the world. Commissioning and producing local language content is an important part of that. But we also invest heavily into improving our product, partnerships and overall consumer experience. For example, in India in Q3, we localized our service to support Hindi in our user interface.

We’re also working with local partners like Reliance Jio, India’s largest mobile operator, where in Q3 we launched a bundle with their mobile and fiber broadband plans. As part of this broad partnership, we’ll integrate Netflix with two of Jio’s set top boxes. We’ve also partnered with financial institutions in India to make payment processing easier and more seamless for our members, which we expect will have retention benefits. All of these initiatives are important and work in concert with our big investment in local originals to improve the Netflix experience for our members.

Competition

Competition for consumers’ time and engagement remains vibrant. Linear television and other big categories of entertainment, like video games and user generated content from YouTube and TikTok are all vying for consumers’ attention and are strong drivers of screen time usage. We remain quite small relative to overall screen time. This past quarter, we saw the debut of Comcast’s Peacock, which comes on the heels of the launch of HBO Max and Disney+. Disney’s recent management reorganization signals that it is embracing the shift to streaming entertainment. We’re thrilled to be competing with Disney and a growing number of other players to entertain people; both consumers and content creators will benefit from our mutual desire to bring the best stories to audiences all over the world. We’ll continue to focus on pleasing our members and improving our service as quickly as possible so that we can be everyone's first choice for online entertainment. Cash Flow and Capital Structure Net cash generated by operating activities in Q3 was +$1.3 billion vs. -$502 million in the prior year period. Free cash flow (FCF) was positive for a third consecutive quarter at +$1.1b vs. -$551 million in 1 Q3‘19. Year to date free cash flow is +$2.2 billion vs. -$1.6 billion in the first nine months of 2019.

As productions increasingly restart, we expect Q4’20 FCF to be slightly negative and therefore, for the full year 2020, we forecast FCF to be approximately $2 billion, up from our prior expectation of break-even to positive. This change is due primarily to our higher operating margin expectation for 2020 and the timing of cash spending on content. We expect our FCF profile over the coming years to continue to improve as we increase our profitability and our transition to the production of Netflix originals (which requires more cash upfront vs. second run content) matures. For 2021, we currently expect free cash flow to be -$1 billion to break-even. With $8.4 billion in cash on our balance sheet at the end of the quarter plus our $750m credit facility (which is undrawn), our need for external financing is diminishing. As indicated last quarter, we don’t have plans to access the capital markets this year

We strive to be a global entertainment service that can satisfy the needs of members all over the world. Commissioning and producing local language content is an important part of that. But we also invest heavily into improving our product, partnerships and overall consumer experience. For example, in India in Q3, we localized our service to support Hindi in our user interface.

We’re also working with local partners like Reliance Jio, India’s largest mobile operator, where in Q3 we launched a bundle with their mobile and fiber broadband plans. As part of this broad partnership, we’ll integrate Netflix with two of Jio’s set top boxes. We’ve also partnered with financial institutions in India to make payment processing easier and more seamless for our members, which we expect will have retention benefits. All of these initiatives are important and work in concert with our big investment in local originals to improve the Netflix experience for our members.

Competition

Competition for consumers’ time and engagement remains vibrant. Linear television and other big categories of entertainment, like video games and user generated content from YouTube and TikTok are all vying for consumers’ attention and are strong drivers of screen time usage. We remain quite small relative to overall screen time. This past quarter, we saw the debut of Comcast’s Peacock, which comes on the heels of the launch of HBO Max and Disney+. Disney’s recent management reorganization signals that it is embracing the shift to streaming entertainment. We’re thrilled to be competing with Disney and a growing number of other players to entertain people; both consumers and content creators will benefit from our mutual desire to bring the best stories to audiences all over the world. We’ll continue to focus on pleasing our members and improving our service as quickly as possible so that we can be everyone's first choice for online entertainment. Cash Flow and Capital Structure Net cash generated by operating activities in Q3 was +$1.3 billion vs. -$502 million in the prior year period. Free cash flow (FCF) was positive for a third consecutive quarter at +$1.1b vs. -$551 million in 1 Q3‘19. Year to date free cash flow is +$2.2 billion vs. -$1.6 billion in the first nine months of 2019.

As productions increasingly restart, we expect Q4’20 FCF to be slightly negative and therefore, for the full year 2020, we forecast FCF to be approximately $2 billion, up from our prior expectation of break-even to positive. This change is due primarily to our higher operating margin expectation for 2020 and the timing of cash spending on content. We expect our FCF profile over the coming years to continue to improve as we increase our profitability and our transition to the production of Netflix originals (which requires more cash upfront vs. second run content) matures. For 2021, we currently expect free cash flow to be -$1 billion to break-even. With $8.4 billion in cash on our balance sheet at the end of the quarter plus our $750m credit facility (which is undrawn), our need for external financing is diminishing. As indicated last quarter, we don’t have plans to access the capital markets this year

Netflix (NASDAQ: NFLX) stock price history over the last 5 years

The image below, obtained from Google, shows the stock price history of Netflix (NASDAQ: NFLX) over the last 5 years. And it's been a exceptional time for Netflix (NASDAQ: NFLX). 5 years ago the stock was trading at around $100 and its currently trading at $525.42. That's a excellent return of 425% over the last 5 years.

The stock of Netflix is trading at a lot closer to its 52 week high of $575.37 and is far far away from its 52 week low of $265.80, which to us is a clear indication that the short term sentiment and momentum of Netflix is very positive at this point in time.

However looking at the pre-market activity in Netflix stock it looks like market participants did not like their latest earnings report as the stock of Netflix is trading down -5.7% in pre-market trade following the release of NetFlix's latest results

The stock of Netflix is trading at a lot closer to its 52 week high of $575.37 and is far far away from its 52 week low of $265.80, which to us is a clear indication that the short term sentiment and momentum of Netflix is very positive at this point in time.

However looking at the pre-market activity in Netflix stock it looks like market participants did not like their latest earnings report as the stock of Netflix is trading down -5.7% in pre-market trade following the release of NetFlix's latest results

Netflix (NASDAQ: NFLX) stock price history over the last 5 years.

Netflix (NFLX) stock vs Walt Disney (DIS) stock over the last 5 years

The image below shows the stock price performance of Netflix (NFLX) and Walt Disney (DIS) over the last 3 years. While both these firms are active in the consumer entertainment industry and both are active in the video streaming service industry, the stock price performance and trends of these two firms are very different. Over the 5 year period Netflix returned 425% while the stock of Disney returned 7.6% over the same period of time. Netflix being the clear winner when it comes to stock performance of the streaming serviec groups over the last 5 years.

Netflix (NFLX) stock vs Walt Disney (DIS) stock over the last 5 years

Recent coverage of Netflix

Recent coverage of Netflix's latest results as obtained from CNBC.com

It wasn’t Netflix’s finest quarter, but if you’re a long-term Netflix believer, you’ve got reason to smile. The streaming video giant reported 300,000 fewer global net subscriber additions than it forecast. Netflix shares fell about 6% after hours.

The quarterly results shouldn’t distract faithful Netflix bulls from the driving reason they’ve been investing in the company, summed up concisely in three sentences from the company’s shareholder letter. “For the full year 2020, we forecast [free cash flow] to be approximately $2 billion, up from our prior expectation of break-even to positive,” Netflix wrote. “We expect our FCF profile over the coming years to continue to improve as we increase our profitability and our transition to the production of Netflix originals matures.”

And then: “With $8.4 billion in cash on our balance sheet at the end of the quarter plus our $750m credit facility (which is undrawn), our need for external financing is diminishing.”

The exact numbers aren’t the important part. Here’s the bottom line: Netflix is no longer burning cash. It has been borrowing billions each year to fund its plethora of original and licensed shows and movies. Believers in Netflix have predicted that as the company’s price-value proposition wins over the global population (with a product far cheaper than traditional pay TV in almost all regions of the world), it will eventually be able to fund its own programming without lending. This will propel the company into a reliable money-maker with plenty of growth runway ahead of it.

Read the full article here

It wasn’t Netflix’s finest quarter, but if you’re a long-term Netflix believer, you’ve got reason to smile. The streaming video giant reported 300,000 fewer global net subscriber additions than it forecast. Netflix shares fell about 6% after hours.

The quarterly results shouldn’t distract faithful Netflix bulls from the driving reason they’ve been investing in the company, summed up concisely in three sentences from the company’s shareholder letter. “For the full year 2020, we forecast [free cash flow] to be approximately $2 billion, up from our prior expectation of break-even to positive,” Netflix wrote. “We expect our FCF profile over the coming years to continue to improve as we increase our profitability and our transition to the production of Netflix originals matures.”

And then: “With $8.4 billion in cash on our balance sheet at the end of the quarter plus our $750m credit facility (which is undrawn), our need for external financing is diminishing.”

The exact numbers aren’t the important part. Here’s the bottom line: Netflix is no longer burning cash. It has been borrowing billions each year to fund its plethora of original and licensed shows and movies. Believers in Netflix have predicted that as the company’s price-value proposition wins over the global population (with a product far cheaper than traditional pay TV in almost all regions of the world), it will eventually be able to fund its own programming without lending. This will propel the company into a reliable money-maker with plenty of growth runway ahead of it.

Read the full article here

Netflix (NASDAQ: NFLX) latest stock valuation

So based on the earnings report of Netflix (NASDAQ: NFLX) what do we value Netflix (NFLX) stock at? Based on the earnings report and the increased competition our valuation models sets a target (full value) price on Netflix of $391.40. (up slightly from our 2nd quarter 2020 Netflix earnings report valuation). Based on our target price (full value price) we believe the stock of Netflix is overvalued.

We usually recommend that long term fundamental or value investors look to enter a stock at least 10% below our target price (full value price) which in this case is $391.40 We therefore believe a good entry point into Netflix is $352.30 or below. Since the stock of Netflix is well above our recommended entry point we would not recommend buying into Netflix right now as we believe there is still a lot of hope and fairytales and butterflies built into their future earnings expectations with the group trading at a PE ratio of over 80

We therefore rate the stock of Netflix (NFLX) as a SELL

We usually recommend that long term fundamental or value investors look to enter a stock at least 10% below our target price (full value price) which in this case is $391.40 We therefore believe a good entry point into Netflix is $352.30 or below. Since the stock of Netflix is well above our recommended entry point we would not recommend buying into Netflix right now as we believe there is still a lot of hope and fairytales and butterflies built into their future earnings expectations with the group trading at a PE ratio of over 80

We therefore rate the stock of Netflix (NFLX) as a SELL

Next earnings release for Netflix

It is expected that Netflix will release its 4th quarter earnings report for their 2020 fiscal year towards the end of January 2021.