|

Related Topics

|

|

Category: Stock Market and Restoration Hardware

Date: 5 December 2019 Stock Price: $205.62 We take a look at the 3rd quarter earnings release of their 2019 fiscal year of Restoration Hardware the luxury brand home furnishings group.

|

|

About Restoration Hardware

We believe RH is one of the most innovative and fastest growing luxury brands in the home furnishings marketplace. We believe our brand stands alone and is redefining this highly fragmented and growing market, contributing to our superior sales growth and market share gains over the past several years as compared to industry growth rates. Our ability to innovate, curate and integrate products, categories, services and businesses with a completely authentic and distinctive point of view, then rapidly scale them across our fully integrated multi-channel infrastructure is a powerful platform for continued long-term growth. We evolved our brand to become RH, positioning our Company to curate a lifestyle beyond the four walls of the home. Our unique product development, go-to-market and supply chain capabilities, together with our significant scale, enable us to offer a compelling combination of design, quality and value that we believe is unparalleled in the marketplace.

Restoration Warehouse outdoor furniture

Overview of Restoration Hardware's 3rd quarter 2019 earnings report

The data below refers to the latest quarter unless specified otherwise:

- Net sales $677.526 million (up from $636.558million from the same quarter of the previous year)

- Net sales increased by 6.4% over the last 12 months

- Cost of sales: $393.360 million (up from $386.537 million for the same quarter of the previous year)

- Cost of sales increased by 1.76% over the last 12 months

- Net income: $52.463 million (down from $20.114 million for the same quarter of the previous year)

- Diluted earnings per share: $2.17 (up from $0.73 for the same quarter of the previous year)

- PE ratio: 23.6 (based on the earnings per share for the current quarter being reported for full fiscal year)

- Diluted weighted-average shares outstanding: 24.170 million (down from 27.703 million for the same quarter of the previous year)

- Cash and cash equivalents: $38.253 million

- Cash and cash equivalents per share: $1.58

- Cash and cash equivalents makes up 0.77% of Restoration Hardware's market capital

- Cash and cash equivalents makes up 1.62% of Restoration Hardware's total assets

- Merchandise inventories: $429.189 million

- Merchandise inventories makes up 18.17% of the group's total assets.

- Cash generated from operations (for 9 months): $210.997 million

- Cash generated from operations per share (for six months): $8.73

Restoration Hardware's management commentary on the results and earnings guidance

To Our People, Partners, and Shareholders,

We are pleased to report record third quarter results and are raising our fiscal 2019 guidance for the fourth time this year.

We generated record GAAP revenues of $678 million in the quarter, an increase of 6.4%, inclusive of a two point drag from eliminating unproductive product categories and fringe promotions. Taking into account the two point drag, revenues for the quarter would have increased 8.4%. We also generated record adjusted operating earnings of $88 million, up 44% versus last year; record adjusted operating margin of 13.0%, a 340 basis points increase versus 9.6% a year ago; record adjusted diluted earnings per share of $2.79, up 74% versus $1.60 last year; and $96 million of free cash flow in the quarter versus $16 million a year ago.

We believe real models will become wildly popular in the post WeWork era

We have spent decades building a business model that generates industry leading profitability and return on invested capital, and believe real models will become wildly popular in the post WeWork era. We also believe this recent period has been reminiscent of previous times when growth without profitability has been unjustly rewarded, and valuations were based on the misplaced belief that an online retail business is more profitable than a physical store. This view has driven new concepts to launch as “digitally native brands” chasing internet valuations and cheap capital from private and public markets who have somehow confused an online retail startup, or in the case of WeWork, an office subleasing business, with a technology company. It’s becoming clear that retail brands birthed online desperately need a store lifeline to survive, as many are finding the variable cost of marketing an invisible store an unprofitable path to the future.

Traditional retailers hoping for the same favorable valuations, and in some cases driven by the fear of not being viewed as fashionable by millennials, have allocated the vast majority of their capital to unnaturally grow their digital business. This has resulted in shifting, not lifting, sales online at greater costs, driving down margins while physical stores have been left to rot.

We on the other hand have chosen to take the road less traveled, and believe, like Robert Frost, that it will make all the difference. Our focus on elevating the RH brand by building architecturally inspiring spaces that blur the lines between residential and retail, indoors and outdoors, home and hospitality with seamlessly integrated restaurants and services, have rendered our brand more valuable while creating a customer experience that cannot be replicated online.

Our dominant physical presence combined with our integrated multi-channel platform that generates over a billion dollars online will continue to enable the RH brand to disrupt the highly fragmented luxury home furnishings market and take share for years to come. Add to the above the most efficient operating platform in our industry, a vertically integrated real estate development model that is dramatically lowering capital requirements and occupancy costs, and our discipline of driving high quality profitable growth and you begin to understand why RH is one of the only brands that is expanding operating margins while generating industry leading returns on invested capital and significant free cash flow.

The emergence of RH as a luxury brand generating luxury margins

We expect our operating margin to expand at least 200 basis points in fiscal 2020 and now see a clear path to a 20% operating margin over the next several years.

We are pleased to report record third quarter results and are raising our fiscal 2019 guidance for the fourth time this year.

We generated record GAAP revenues of $678 million in the quarter, an increase of 6.4%, inclusive of a two point drag from eliminating unproductive product categories and fringe promotions. Taking into account the two point drag, revenues for the quarter would have increased 8.4%. We also generated record adjusted operating earnings of $88 million, up 44% versus last year; record adjusted operating margin of 13.0%, a 340 basis points increase versus 9.6% a year ago; record adjusted diluted earnings per share of $2.79, up 74% versus $1.60 last year; and $96 million of free cash flow in the quarter versus $16 million a year ago.

We believe real models will become wildly popular in the post WeWork era

We have spent decades building a business model that generates industry leading profitability and return on invested capital, and believe real models will become wildly popular in the post WeWork era. We also believe this recent period has been reminiscent of previous times when growth without profitability has been unjustly rewarded, and valuations were based on the misplaced belief that an online retail business is more profitable than a physical store. This view has driven new concepts to launch as “digitally native brands” chasing internet valuations and cheap capital from private and public markets who have somehow confused an online retail startup, or in the case of WeWork, an office subleasing business, with a technology company. It’s becoming clear that retail brands birthed online desperately need a store lifeline to survive, as many are finding the variable cost of marketing an invisible store an unprofitable path to the future.

Traditional retailers hoping for the same favorable valuations, and in some cases driven by the fear of not being viewed as fashionable by millennials, have allocated the vast majority of their capital to unnaturally grow their digital business. This has resulted in shifting, not lifting, sales online at greater costs, driving down margins while physical stores have been left to rot.

We on the other hand have chosen to take the road less traveled, and believe, like Robert Frost, that it will make all the difference. Our focus on elevating the RH brand by building architecturally inspiring spaces that blur the lines between residential and retail, indoors and outdoors, home and hospitality with seamlessly integrated restaurants and services, have rendered our brand more valuable while creating a customer experience that cannot be replicated online.

Our dominant physical presence combined with our integrated multi-channel platform that generates over a billion dollars online will continue to enable the RH brand to disrupt the highly fragmented luxury home furnishings market and take share for years to come. Add to the above the most efficient operating platform in our industry, a vertically integrated real estate development model that is dramatically lowering capital requirements and occupancy costs, and our discipline of driving high quality profitable growth and you begin to understand why RH is one of the only brands that is expanding operating margins while generating industry leading returns on invested capital and significant free cash flow.

The emergence of RH as a luxury brand generating luxury margins

We expect our operating margin to expand at least 200 basis points in fiscal 2020 and now see a clear path to a 20% operating margin over the next several years.

China tariffs – the long and winding road

Regarding trade with China, we do not expect the current tariffs to impair our ability to achieve stated financial goals and the impact from the increased tariffs is embedded in our guidance for the year. We continue to receive pricing accommodations from vendors and have implemented price increases where necessary with little to no impact to our business.

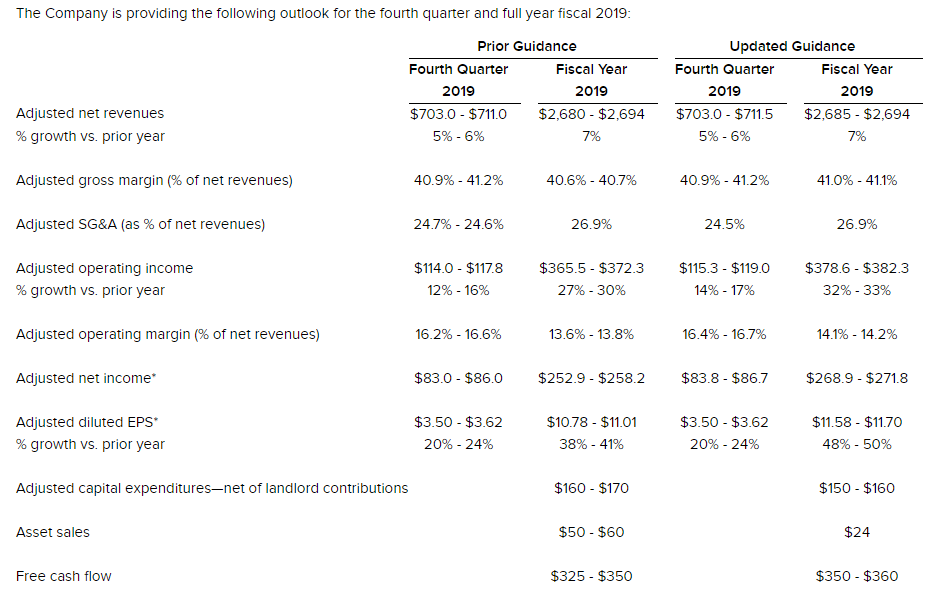

The image below shows the 4th quarter and full 2019 fiscao year guidance as provided by Restoration Warehouse

Regarding trade with China, we do not expect the current tariffs to impair our ability to achieve stated financial goals and the impact from the increased tariffs is embedded in our guidance for the year. We continue to receive pricing accommodations from vendors and have implemented price increases where necessary with little to no impact to our business.

The image below shows the 4th quarter and full 2019 fiscao year guidance as provided by Restoration Warehouse

Fiscal guidance provided by Restoration Warehouse

Increasing our long-term outlook

Looking forward, we see a clear path to over $5 billion in North America revenues, with high teens to low twenties operating margins and ROIC in excess of 50%. Additionally, we now believe there is an opportunity to build a $20 billion global brand as we expand internationally and further develop the RH ecosystem that will move the brand beyond creating and selling products to conceptualizing and selling spaces.

We are increasing our long-term targets to:

Looking forward, we see a clear path to over $5 billion in North America revenues, with high teens to low twenties operating margins and ROIC in excess of 50%. Additionally, we now believe there is an opportunity to build a $20 billion global brand as we expand internationally and further develop the RH ecosystem that will move the brand beyond creating and selling products to conceptualizing and selling spaces.

We are increasing our long-term targets to:

- Net revenue growth of 8% to 12%

- Adjusted operating margins in the high teens to low twenties

- Adjusted net income growth of 15% to 20%

- Return on invested capital (ROIC) in excess of 50%

A home's interior that was decorated by products from Restoration Warehouse

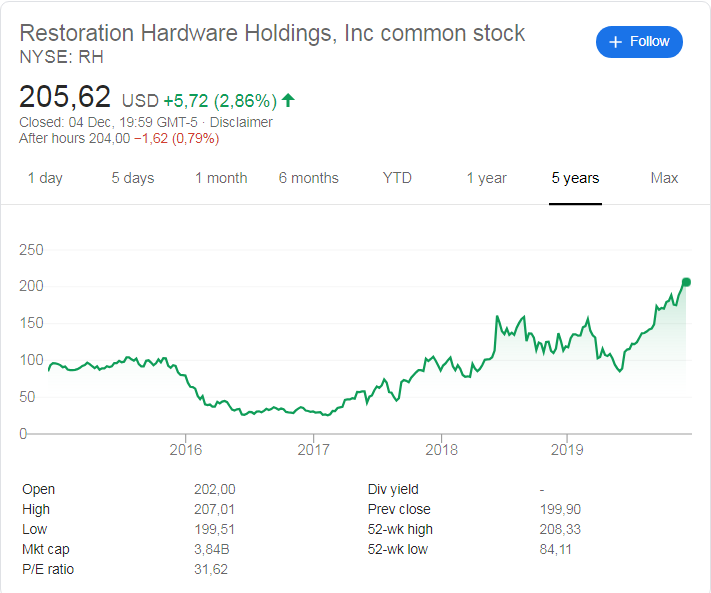

Restoration Hardware (NYSE: RH) stock price history

The image below, obtained from Google shows the stock price history of Restoration Hardware over the last 5 years. And its been a very volatile but overall a good time for stockholders of Restoration Hardware with the stock trading around $85.20 five years ago, and its currently trading at $205.62.

That's a very healthy return of 141.40% over the last 5 years being provided by Restoration Hardware to stockowners. The stock is trading at very close to its 52 week high of $208.33 and is far away from its 52 week low of $84.11, which is a clear indication that short term sentiment and momentum of Restoration Hardware is overwhelmingly positive.

That's a very healthy return of 141.40% over the last 5 years being provided by Restoration Hardware to stockowners. The stock is trading at very close to its 52 week high of $208.33 and is far away from its 52 week low of $84.11, which is a clear indication that short term sentiment and momentum of Restoration Hardware is overwhelmingly positive.

Restoration Hardware (NYSE:RH) stock price history over the last 5 years

Recent coverage of Restoration Hardware

The extract below touches on the latest results from Restoration Hardware, as obtained from Zacks.

RH (RH) - Get Report shares were ripping higher on Friday, up more than 6% on news that Warren Buffett's Berkshire Hathaway (BRK.A) - Get Report(BRK.B) - Get Report has taken a stake in the retailer. RH, perhaps better known as Restoration Hardware, is not necessarily the typical Berkshire investment. Then again, neither is Amazon.com (AMZN) - Get Report .

But that only makes it look more attractive to many bulls, who have witnessed the stock's 2019 ascent. Shares of RH have jumped 50% over the past year and have more than doubled from their lows in May. Berkshire gobbled up 1.21 million shares and while that may seem insignificant for a massive company like Buffett's, consider that RH has just about 18.6 million shares outstanding. After a series of beat-and-raise earnings reports, momentum has been on Restoration's side. With Berkshire's stake, bulls are feeling even more confident. Now just a few dollars from new 52-week highs, can RH stock continue to rally?

Read the full article here.

RH (RH) - Get Report shares were ripping higher on Friday, up more than 6% on news that Warren Buffett's Berkshire Hathaway (BRK.A) - Get Report(BRK.B) - Get Report has taken a stake in the retailer. RH, perhaps better known as Restoration Hardware, is not necessarily the typical Berkshire investment. Then again, neither is Amazon.com (AMZN) - Get Report .

But that only makes it look more attractive to many bulls, who have witnessed the stock's 2019 ascent. Shares of RH have jumped 50% over the past year and have more than doubled from their lows in May. Berkshire gobbled up 1.21 million shares and while that may seem insignificant for a massive company like Buffett's, consider that RH has just about 18.6 million shares outstanding. After a series of beat-and-raise earnings reports, momentum has been on Restoration's side. With Berkshire's stake, bulls are feeling even more confident. Now just a few dollars from new 52-week highs, can RH stock continue to rally?

Read the full article here.

Restoration Hardware (NYSE: RH) latest stock valuation

So based on Restoration Warehouse's latest earnings report what are their stock currently worth? Based on Restoration Hardware's current earnings report and the updated fiscal guidance provided we have a target (full value) price in the stock at $185.30 (up slightly from our 2nd quarter 2019 earnings report valuation of Restoration). So we believe at its current price Restoration Hardware is overvalued.

However for fundamental long term or value investors we would recommend looking to enter Restoration Hardware stock at, at least 10% below our target (full value) price of $185.30. We would therefore suggest looking to enter into the stock of Restoration Hardware at around $166.80 or below. We expect the stock of Restoration Hardware to pull back from current levels to levels closer to our target price/ full value price.

However for fundamental long term or value investors we would recommend looking to enter Restoration Hardware stock at, at least 10% below our target (full value) price of $185.30. We would therefore suggest looking to enter into the stock of Restoration Hardware at around $166.80 or below. We expect the stock of Restoration Hardware to pull back from current levels to levels closer to our target price/ full value price.

Next earnings release of Restoration Hardware (NYSE: RH)

It is expected that Restoration Hardware will release their 4th quarter and full fiscal 2019 earnings report in late February 2020